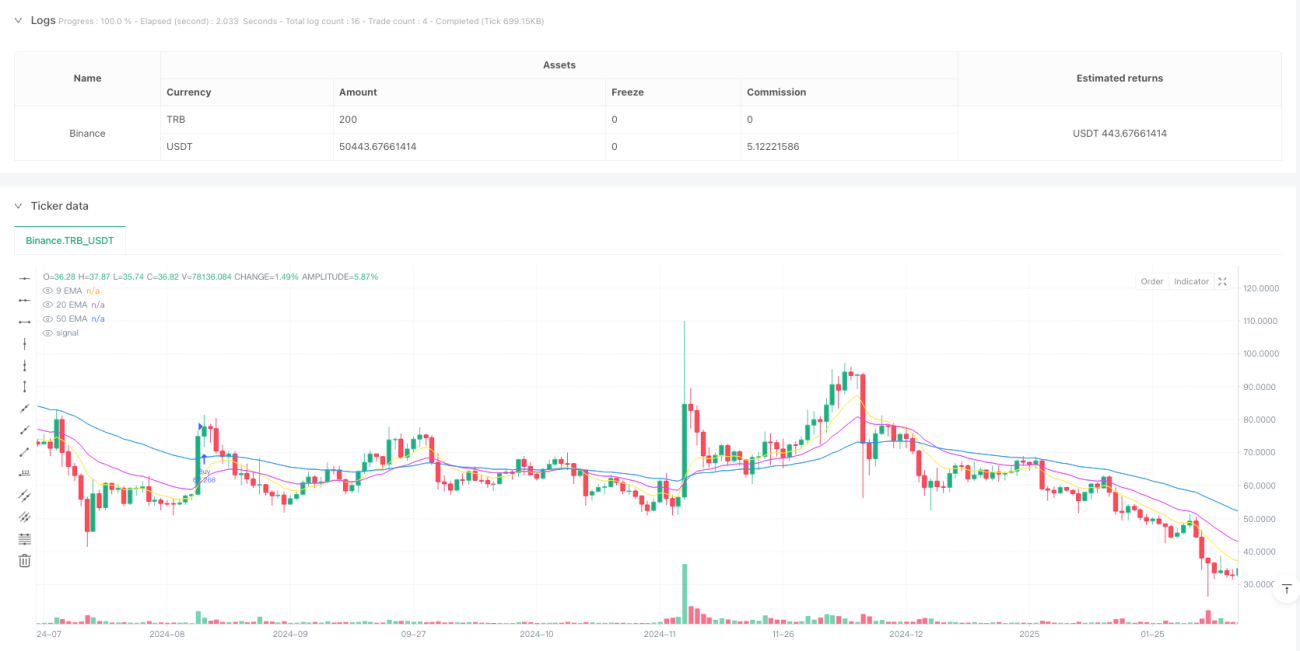

Gambaran Keseluruhan

Ini adalah strategi perdagangan mata wang kripto berdasarkan sistem penjejakan arah aliran purata bergerak berbilang, yang menggabungkan penunjuk RSI dan ATR untuk penapisan perdagangan dan pengurusan risiko. Strategi ini terutamanya menyasarkan mata wang kripto utama, mengawal risiko dengan menetapkan had kekerapan dagangan harian dan henti rugi/ambil untung dinamik. Strategi ini menggunakan tiga purata bergerak eksponen (EMA) iaitu 9-kitaran, 20-kitaran, dan 50-kitaran untuk menentukan arah aliran, serta menggunakan Indeks Kekuatan Relatif (RSI) dan Purata Julat Sebenar (ATR) sebagai penunjuk tambahan untuk penapisan perdagangan.

Prinsip Strategi

Logik perdagangan teras strategi ini merangkumi beberapa bahagian utama:

- Penentuan arah aliran: Menggunakan tiga EMA (9/20/50) untuk menentukan arah aliran. Apabila EMA jangka pendek melintasi EMA jangka sederhana dan harga berada di atas EMA jangka panjang, ia dianggap sebagai arah aliran menaik; sebaliknya, ia dianggap sebagai arah aliran menurun.

- Penapisan perdagangan: Menggunakan RSI (14) untuk penapisan terlebih beli/terlebih jual. Isyarat beli memerlukan RSI antara 45-70, manakala isyarat jual memerlukan RSI antara 30-55.

- Pengesahan kekuatan arah aliran: Memerlukan jarak harga dari EMA 50-kitaran lebih besar daripada 1.1 kali ganda ATR untuk memastikan arah aliran cukup kukuh.

- Pengurusan risiko: Berdasarkan ciri turun naik mata wang kripto yang berbeza, tetapkan henti rugi pada 2.5-3.2 kali ganda ATR dan ambil untung pada 3.5-5.0 kali ganda ATR.

- Kawalan kekerapan dagangan: Maksimum satu dagangan dibenarkan setiap hari dagangan untuk mengelakkan dagangan berlebihan.

Kelebihan Strategi

- Pengurusan risiko dinamik: Melaraskan kedudukan henti rugi/ambil untung secara dinamik melalui ATR, menyesuaikan dengan ciri turun naik tinggi pasaran mata wang kripto.

- Pemprosesan berbeza: Menetapkan parameter risiko yang berbeza berdasarkan ciri turun naik mata wang kripto yang berbeza.

- Mekanisme penapisan berbilang: Menggabungkan penunjuk arah aliran, momentum, dan turun naik untuk meningkatkan kualiti perdagangan.

- Had kekerapan dagangan: Mengurangkan risiko dagangan berlebihan melalui had dagangan harian, sesuai terutamanya untuk ciri turun naik tinggi pasaran mata wang kripto.

- Pengurusan modal yang munasabah: Mengira saiz dagangan secara dinamik berdasarkan saiz akaun dan tahap risiko, melindungi keselamatan modal.

Risiko Strategi

- Risiko pembalikan arah aliran: Mungkin mengalami kerugian besar semasa turun naik teruk pasaran mata wang kripto.

- Risiko gelinciran: Mungkin menghadapi gelinciran besar apabila kecairan tidak mencukupi.

- Had peluang dagangan: Had bilangan dagangan harian mungkin terlepas peluang dalam pasaran yang bergerak pantas.

- Kepekaan parameter: Tetapan pelbagai parameter penunjuk akan mempengaruhi prestasi strategi, memerlukan pengoptimuman berkala.

- Pergantungan persekitaran pasaran: Strategi berprestasi lebih baik dalam pasaran arah aliran, tetapi mungkin menghasilkan isyarat palsu dalam pasaran berayun.

Arah Pengoptimuman Strategi

- Memperkenalkan analisis kitaran turun naik pasaran: Boleh melaraskan parameter secara dinamik berdasarkan kitaran turun naik pasaran mata wang kripto yang berbeza.

- Mengoptimumkan penapisan masa dagangan: Menambah syarat penapisan berdasarkan sesi dagangan utama global.

- Menambah baik mekanisme keluar: Boleh menambah henti rugi bergerak atau mekanisme keluar dinamik berdasarkan sentimen pasaran.

- Menambah pengurusan saiz dagangan: Boleh melaraskan saiz dagangan secara dinamik berdasarkan turun naik pasaran.

- Menambah penunjuk sentimen pasaran: Memperkenalkan data rantaian atau penunjuk sentimen media sosial untuk meningkatkan penapisan perdagangan.

Kesimpulan

Strategi ini mencapai sistem perdagangan mata wang kripto yang agak kukuh melalui penggunaan menyeluruh pelbagai penunjuk teknikal. Dengan tetapan parameter risiko yang berbeza dan kawalan kekerapan dagangan yang ketat, ia mengimbangi pulangan dan risiko dengan baik. Kelebihan teras strategi ini terletak pada mekanisme pengurusan risiko dinamik dan sistem penapisan yang lengkap, tetapi juga perlu memberi perhatian kepada risiko turun naik tinggi dan kecairan yang unik dalam pasaran mata wang kripto. Melalui pengoptimuman dan penambahbaikan berterusan, strategi ini dijangka dapat mengekalkan prestasi yang stabil dalam pelbagai persekitaran pasaran.

/*backtest

start: 2015-02-22 00:00:00

end: 2025-02-18 17:23:25

period: 1h

basePeriod: 1h

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © buffalobillcody

//@version=6

strategy("Backtest Last 2880 Baars Filers and Exits", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=2, backtest_fill_limits_assumption=0)- 1