Sistem Perdagangan Mengikuti Trend dengan Penghentian Rugi Menjejak Dinamik ATR

Gambaran Keseluruhan

Strategi ini adalah sistem penjejakan arah aliran (trend following) berdasarkan henti rugi dinamik ATR (Purata Julat Sebenar/ Average True Range). Ia menggabungkan purata bergerak EMA sebagai penapis arah aliran, dan mengawal penjanaan isyarat dengan melaraskan parameter sensitiviti dan kitaran ATR. Sistem ini menyokong dagangan panjang (long) dan pendek (short), serta mempunyai mekanisme pengurusan keuntungan yang lengkap.

Prinsip Strategi

- Menggunakan penunjuk ATR untuk mengira amplitud pergerakan harga, dan menentukan jarak henti rugi dinamik berdasarkan pekali sensitiviti (Nilai Utama/ Key Value).

- Menentukan arah aliran pasaran melalui purata bergerak EMA; hanya membuka dagangan panjang apabila harga berada di atas purata bergerak, dan membuka dagangan pendek apabila harga berada di bawah purata bergerak.

- Apabila harga menembusi garisan henti rugi dinamik dan mematuhi arah aliran, isyarat dagangan akan tercetus.

- Sistem menguruskan kedudukan dengan kaedah pemberhentian keuntungan berperingkat:

- Apabila keuntungan 20%-50%, henti rugi dinaikkan ke harga kos untuk pulang modal.

- Apabila keuntungan 50%-80%, sebahagian keuntungan direalisasikan dan henti rugi diketatkan.

- Apabila keuntungan 80%-100%, henti rugi diketatkan lagi untuk melindungi keuntungan.

- Apabila keuntungan melebihi 100%, semua kedudukan ditutup sepenuhnya.

Kelebihan Strategi

- Henti rugi dinamik dapat menjejak arah aliran dengan berkesan, melindungi keuntungan tanpa meninggalkan pasaran terlalu awal.

- Penapis arah aliran EMA berkesan mengurangkan risiko penembusan palsu.

- Mekanisme pemberhentian keuntungan berperingkat memastikan keuntungan direalisasikan sambil memberi ruang yang mencukupi untuk perkembangan arah aliran.

- Menyokong dagangan dua arah (panjang dan pendek), membolehkan peluang pasaran dimanfaatkan sepenuhnya.

- Parameter boleh laras yang tinggi, sesuai untuk pelbagai keadaan pasaran.

Risiko Strategi

- Dalam pasaran yang bergelora (sideways), mungkin berlaku dagangan yang kerap dan menyebabkan kerugian.

- Pada peringkat awal pembalikan arah aliran, mungkin berlakunya penarikan balik (drawdown) yang besar.

- Tetapan parameter yang tidak sesuai boleh menjejaskan prestasi strategi.

Cadangan pengurusan risiko:

- Digunakan dalam pasaran yang mempunyai arah aliran yang jelas.

- Pilih parameter dengan berhati-hati; boleh dioptimumkan melalui ujian balik (backtesting).

- Tetapkan had penarikan balik maksimum.

- Pertimbangkan untuk menambah syarat penapis keadaan pasaran.

Hala Tuju Pengoptimuman Strategi

- Menambah mekanisme pengiktirafan keadaan pasaran, menggunakan parameter yang berbeza dalam keadaan pasaran yang berbeza.

- Memperkenalkan penunjuk bantu seperti volum dagangan untuk meningkatkan kebolehpercayaan isyarat.

- Mengoptimumkan mekanisme pengurusan keuntungan, melaraskan sasaran keuntungan secara dinamik berdasarkan turun naik (volatiliti).

- Menambah penapis masa untuk mengelakkan dagangan pada waktu yang tidak menguntungkan.

- Mempertimbangkan penapis turun naik untuk mengurangkan kekerapan dagangan semasa turun naik yang berlebihan.

Kesimpulan

Ini adalah sistem penjejakan arah aliran yang mempunyai struktur lengkap dan logik yang jelas. Melalui gabungan penjejakan dinamik ATR dan penapis arah aliran EMA, ia dapat mengawal risiko dengan baik sambil menangkap arah aliran. Reka bentuk mekanisme pemberhentian keuntungan berperingkat juga mencerminkan pemikiran dagangan yang matang. Strategi ini mempunyai kepraktisan dan kebolehlanjutan yang tinggi; melalui pengoptimuman dan penambahbaikan berterusan, ia dijangka dapat mencapai hasil dagangan yang lebih baik.

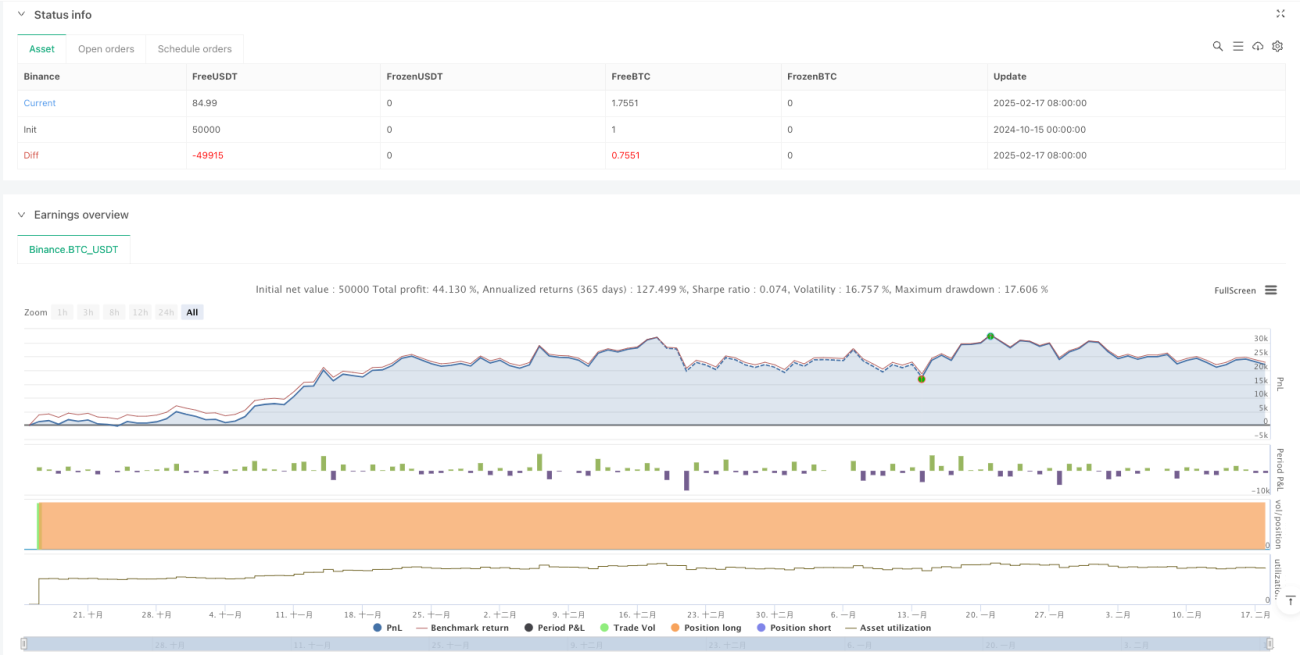

/*backtest

start: 2024-10-15 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Enhanced UT Bot with Long & Short Trades", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input Parameters- 1