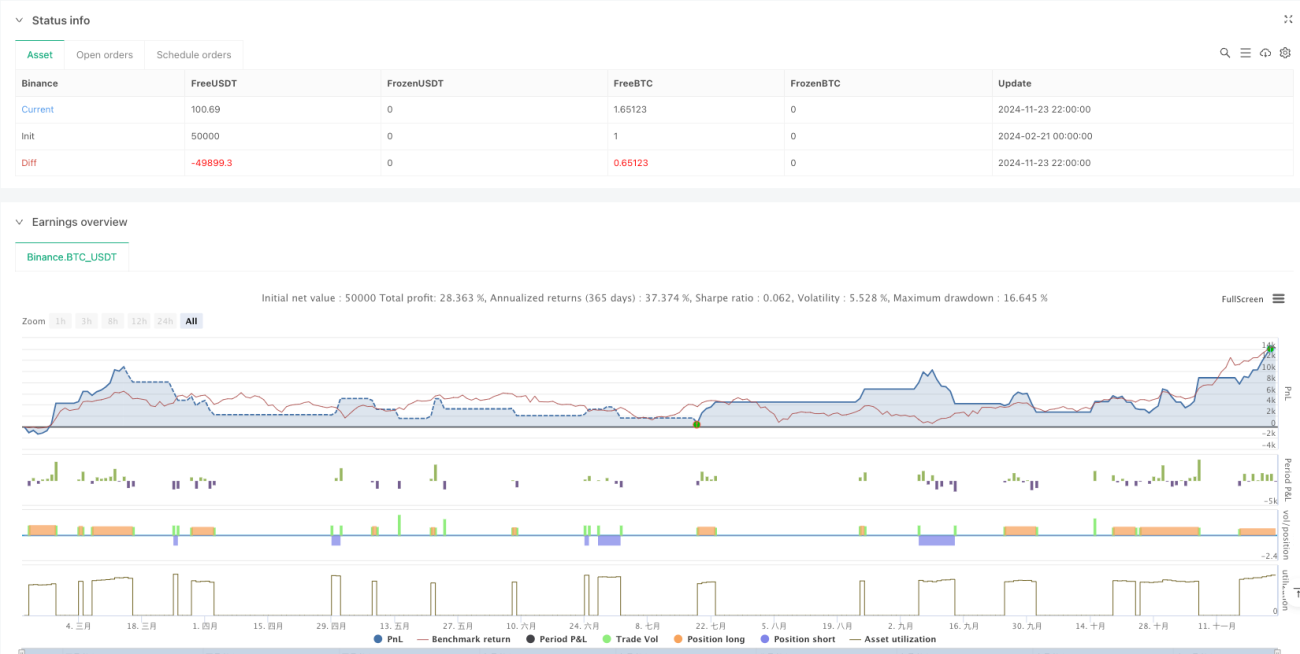

Gambaran Keseluruhan

Strategi ini menggabungkan Harga Purata Berwajaran Volume (VWAP) dan Purata Bergerak Eksponen (EMA) berbilang tempoh. Strategi ini digunakan terutamanya untuk dagangan intrahari, sesuai khususnya untuk tempoh masa 15 minit. Strategi menentukan arah aliran pasaran dan peluang dagangan dengan menganalisis hubungan antara harga dengan VWAP dan EMA pada tempoh yang berbeza, serta menggabungkan maklumat volume.

Prinsip Strategi

Strategi ini menggunakan EMA 10 tempoh, 20 tempoh, dan 200 tempoh, serta VWAP sebagai penunjuk teras. Isyarat dagangan dijana berdasarkan syarat berikut:

- Syarat masuk beli: Harga mestilah lebih tinggi daripada VWAP, 200EMA, 10EMA dan 20EMA secara serentak; harga tutup lilin semasa lebih tinggi daripada harga buka; VWAP berada di atas 200EMA; 10EMA berada di atas 20EMA, dan 20EMA berada di atas VWAP.

- Syarat masuk jual: Gabungan syarat yang bertentangan dengan beli.

- Hentian rugi: Menggunakan titik terendah 10 lilin sebelumnya (untuk beli) atau titik tertinggi (untuk jual) ditambah/dikurangkan dengan nilai ATR.

- Sasaran untung: Menetapkan dua sasaran menggunakan nisbah risiko-keuntungan 1:2 dan 1:3.

Kelebihan Strategi

- Mekanisme pengesahan berganda: Penggunaan beberapa penunjuk teknikal secara bersama meningkatkan kebolehpercayaan isyarat dagangan.

- Pengurusan risiko dinamik: Hentian rugi dinamik berdasarkan ATR dapat menyesuaikan diri dengan perubahan volatiliti pasaran.

- Sasaran untung yang jelas: Nisbah risiko-keuntungan tetap memudahkan pengawalan risiko oleh pedagang.

- Gabungan pengesanan arah aliran dan momentum: Dengan purata bergerak berbilang tempoh, ia dapat menangkap arah aliran dan tidak melepaskan peluang jangka pendek.

Risiko Strategi

- Risiko ketinggalan: EMA dan VWAP adalah penunjuk ketinggalan, mungkin tidak bertindak balas tepat pada masanya apabila pasaran berubah arah dengan cepat.

- Risiko pasaran bergetar: Semasa fasa pengukuhan mendatar, mungkin menghasilkan terlalu banyak isyarat pecah palsu.

- Risiko pengurusan modal: Nisbah risiko-keuntungan tetap mungkin tidak sesuai untuk semua keadaan pasaran.

- Kesan kos dagangan: Dagangan yang kerap boleh menyebabkan kos dagangan yang tinggi.

Arah Pengoptimuman Strategi

- Menambah penapis volatiliti: Boleh menambah ambang peratusan ATR untuk mengelakkan dagangan dalam persekitaran volatiliti rendah.

- Mengoptimumkan penapis masa: Menetapkan tempoh dagangan terbaik berdasarkan ciri pasaran yang berbeza.

- Melaraskan nisbah risiko-keuntungan secara dinamik: Menyesuaikan sasaran untung berdasarkan volatiliti pasaran.

- Menambah pengesahan volume: Menetapkan ambang volume minimum untuk meningkatkan kebolehpercayaan pecahan.

Kesimpulan

Strategi ini membina sistem dagangan lengkap dengan menggabungkan beberapa penunjuk teknikal. Kelebihan utama strategi ini adalah mekanisme pengesahan berganda dan sistem pengurusan risiko yang komprehensif. Walaupun terdapat risiko ketinggalan, melalui arah pengoptimuman yang dicadangkan, kestabilan dan keuntungan strategi dapat ditingkatkan lagi. Strategi ini sesuai terutamanya untuk pedagang intrahari, tetapi memerlukan pengoptimuman parameter berdasarkan ciri pasaran tertentu.

- 1