Gambaran Keseluruhan

Strategi ini adalah sistem perdagangan pintar berdasarkan penjejakan arah aliran dan perdagangan momentum, direka khas untuk senario dagangan jangka pendek dan pantas. Teras strategi menggunakan gabungan sistem penilaian persilangan Purata Bergerak Eksponen (EMA), Indeks Kekuatan Relatif (RSI) dan Purata Julat Sebenar (ATR), serta dilengkapi dengan mekanisme henti rugi pintar berasaskan peratusan. Strategi ini amat sesuai untuk perdagangan pada carta jangka masa pendek seperti 1 minit dan 5 minit, dengan melaraskan parameter secara dinamik untuk menyesuaikan dengan persekitaran pasaran yang berbeza.

Prinsip Strategi

Strategi ini menggunakan tiga petunjuk teknikal teras untuk membina sistem isyarat perdagangan:

- Sistem persilangan Purata Bergerak Eksponen (EMA) cepat dan perlahan - menggunakan gabungan EMA 9 kitaran dan 21 kitaran, menentukan arah aliran melalui persilangan emas (golden cross) dan persilangan maut (death cross)

- Penapis RSI terlebih beli/terlebih jual - menggunakan RSI 14 kitaran, dengan nilai 70 dan 30 sebagai ambang terlebih beli dan terlebih jual, bagi mengelakkan masuk semasa keadaan melampau

- Mekanisme pengesahan turun naik ATR - menggunakan ATR untuk mengukur turun naik pasaran, memastikan pelaksanaan dagangan hanya apabila terdapat kekuatan penembusan yang mencukupi

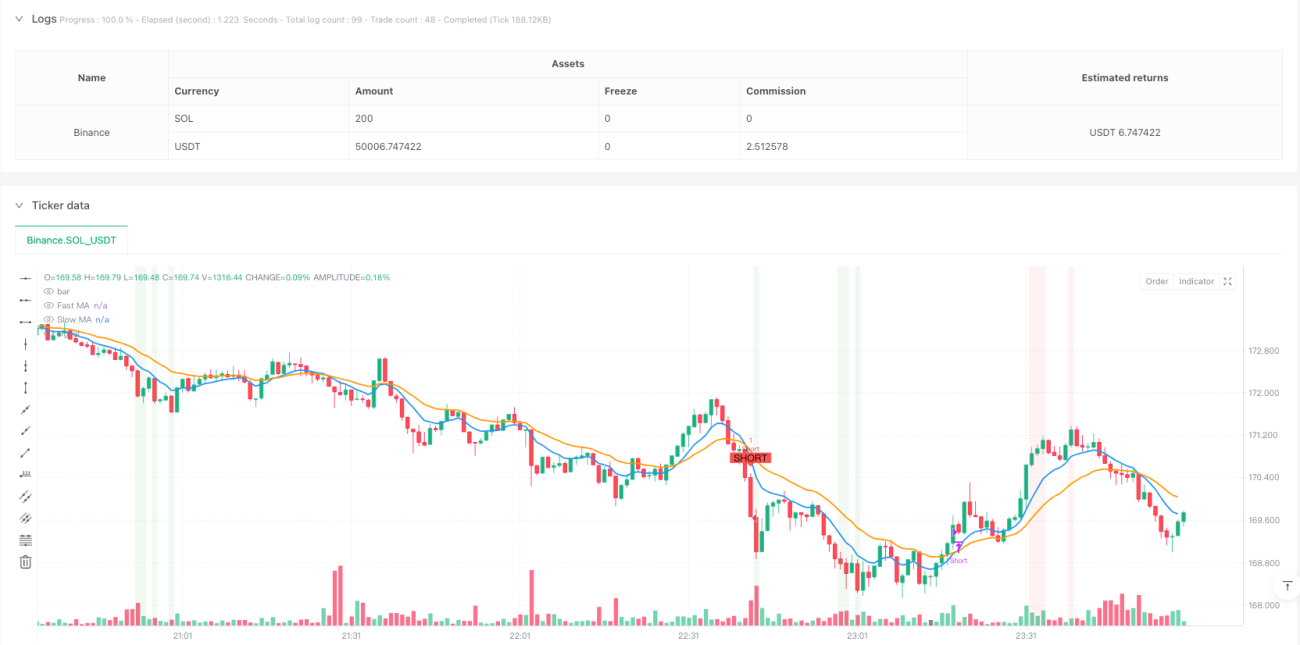

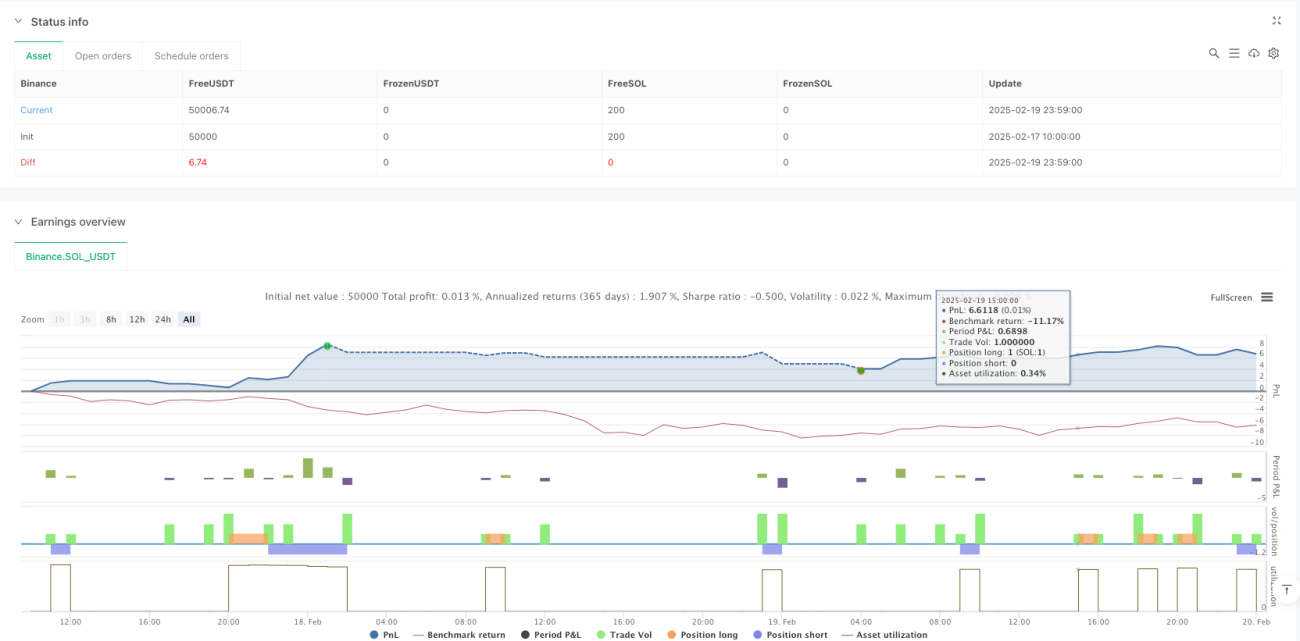

Logik dagangan direka dengan jelas: Kemasukan beli memerlukan garisan cepat melintasi garisan perlahan ke atas, RSI di bawah 70 dan harga melepasi gandaan ATR; Kemasukan jual memerlukan garisan cepat melintasi garisan perlahan ke bawah, RSI di atas 30 dan harga jatuh di bawah gandaan ATR. Sistem ini dilengkapi dengan henti rugi dinamik 1% untuk mengawal risiko dengan berkesan.

Kelebihan Strategi

- Pengesahan silang pelbagai petunjuk teknikal meningkatkan kebolehpercayaan isyarat

- Sistem penyesuaian parameter dinamik sesuai untuk jangka masa yang berbeza

- Mekanisme penapisan turun naik berasaskan ATR mengurangkan isyarat palsu

- Sistem henti rugi pintar mengawal risiko setiap dagangan dengan ketat

- Sistem visualisasi lengkap termasuk tanda grafik yang jelas dan petunjuk latar belakang

Risiko Strategi

- Pasaran yang tidak menentu mungkin menghasilkan isyarat dagangan yang kerap, meningkatkan kos perdagangan

- Henti rugi peratusan tetap mungkin tidak sesuai untuk semua persekitaran pasaran

- Risiko gelinciran (slippage) mungkin berlaku semasa tempoh turun naik tinggi

- Pengoptimuman parameter memerlukan pemantauan dan pelarasan berterusan

Untuk mengurangkan risiko, adalah disyorkan:

- Melaraskan peratusan henti rugi mengikut ciri-ciri instrumen yang berbeza

- Menambah mekanisme pengesahan kekuatan arah aliran

- Memantau keadaan turun naik pasaran secara masa nyata

- Mewujudkan sistem pengurusan modal yang lengkap

Hala Tuju Pengoptimuman Strategi

- Memperkenalkan mekanisme henti rugi adaptif, melaraskan nisbah henti rugi secara dinamik berdasarkan turun naik pasaran

- Menambah penapis kekuatan arah aliran untuk meningkatkan kualiti isyarat perdagangan

- Membangunkan sistem penapisan masa pintar untuk mengelakkan tempoh kecairan rendah

- Mengintegrasikan petunjuk volum untuk meningkatkan kebolehpercayaan isyarat

- Membangunkan sistem pengoptimuman parameter dinamik untuk membolehkan pelarasan diri strategi

Kesimpulan

Strategi ini membina sistem perdagangan yang lengkap melalui sinergi pelbagai petunjuk teknikal. Sistem ini mengekalkan fleksibiliti sambil memastikan keselamatan perdagangan melalui kawalan risiko yang ketat. Walaupun terdapat batasan tertentu, dengan pengoptimuman dan penambahbaikan berterusan, strategi ini mempunyai nilai aplikasi dan potensi pembangunan yang baik.

- 1