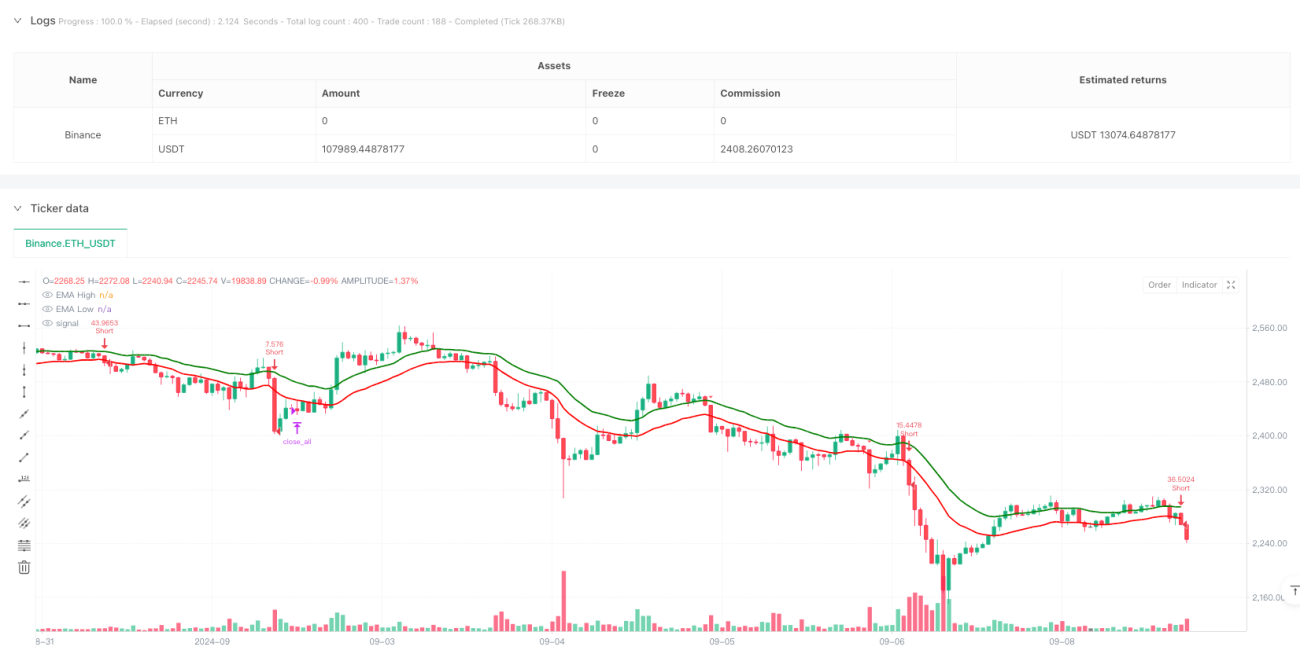

Gambaran Keseluruhan

Ini adalah strategi dagangan intrahari berdasarkan pelbagai penunjuk teknikal, menggunakan saluran EMA, RSI terlebih beli/terlebih jual, dan pengesahan arah aliran MACD untuk menjana isyarat. Strategi ini beroperasi pada kitaran 3 minit, menangkap arah aliran pasaran melalui saluran EMA tinggi/rendah yang digabungkan dengan pengesahan persilangan RSI dan MACD. Ia dilengkapi dengan henti rugi dan ambil untung dinamik berdasarkan ATR, serta masa tutup dagangan tetap.

Prinsip Strategi

Strategi menggunakan EMA 20 kitaran yang dikira pada harga tertinggi dan terendah untuk membentuk saluran. Apabila harga menembusi saluran dan memenuhi syarat berikut, posisi dibuka:

- Masuk beli: harga tutup menembusi atas saluran EMA tinggi, RSI antara 50-70, garisan MACD menembusi ke atas garisan isyarat.

- Masuk jual: harga tutup menembusi bawah saluran EMA rendah, RSI antara 30-50, garisan MACD menembusi ke bawah garisan isyarat.

- Gunakan ATR untuk mengira kedudukan henti rugi secara dinamik, tetapkan ambil untung berdasarkan nisbah risiko-ke-untung 2.5 kali ganda.

- Risiko setiap dagangan adalah 1% daripada akaun, saiz posisi dikira secara dinamik berdasarkan jarak henti rugi.

- Paksa tutup semua posisi pada pukul 15:00 waktu piawai India.

Kelebihan Strategi

- Pengesahan silang pelbagai penunjuk teknikal meningkatkan kebolehpercayaan isyarat dagangan.

- Henti rugi dinamik berdasarkan ATR menyesuaikan dengan turun naik pasaran dengan lebih baik.

- Nisbah risiko tetap dan nisbah risiko-ke-untung mengawal risiko dengan berkesan.

- Mengambil kira kos dagangan, termasuk pengiraan komisen.

- Melarang penambahan posisi dalam arah yang sama, mengelakkan risiko pegangan berlebihan.

- Waktu tutup tetap mengelakkan risiko semalaman.

Risiko Strategi

- Pelbagai penunjuk boleh menyebabkan kelewatan isyarat, menjejaskan masa masuk.

- Saluran EMA mungkin menghasilkan penembusan palsu yang kerap dalam pasaran mendatar.

- Nisbah risiko-ke-untung tetap mungkin tidak fleksibel merentasi persekitaran pasaran yang berbeza.

- Had julat RSI mungkin menyebabkan terlepas arah aliran besar.

- Paksa tutup pada waktu tetap mungkin menyebabkan keluar pada tahap kritikal.

Arah Pengoptimuman Strategi

- Pertimbangkan untuk menambah penunjuk volum sebagai pengesahan tambahan.

- Laraskan nisbah risiko-ke-untung secara dinamik berdasarkan ciri turun naik dalam tempoh berbeza.

- Perkenalkan penunjuk turun naik pasaran untuk melaraskan ambang RSI secara dinamik.

- Pertimbangkan untuk menambah penapis kekuatan arah aliran untuk mengurangkan penembusan palsu.

- Boleh menyesuaikan parameter berdasarkan ciri tempoh berbeza dalam hari yang sama.

- Tambah analisis turun naik sejarah untuk mengoptimumkan pengurusan kedudukan.

Kesimpulan

Strategi ini membina sistem dagangan yang agak lengkap melalui penggunaan gabungan pelbagai penunjuk teknikal. Kelebihan strategi terletak pada kawalan risiko yang agak sempurna, termasuk henti rugi dinamik, risiko tetap dan mekanisme tutup pada waktu tetap. Walaupun terdapat risiko kelewatan, prestasi strategi boleh dipertingkatkan lagi melalui pengoptimuman parameter dan penambahan penunjuk tambahan. Strategi ini sangat sesuai untuk pasaran dagangan intrahari yang agak tidak menentu, menjana keuntungan stabil melalui kawalan risiko ketat dan pengesahan isyarat berganda.

- 1