Strategi Pecahan Trend Gabungan Pelbagai Indikator Teknikal

Ringkasan

Strategi ini merupakan sistem perdagangan pecah arah (trend breakout) yang menggabungkan pelbagai penunjuk teknikal dan corak grafik. Ia menangkap titik perubahan arah pasaran dengan mengenal pasti corak grafik utama (seperti dua puncak/dua lembah, kepala dan bahu atas/bawah) dan penembusan harga, sambil menggabungkan penunjuk teknikal seperti EMA, ATR dan volum untuk penapisan isyarat dan pengurusan risiko, mencapai penjejakan arah dan kawalan risiko yang cekap.

Prinsip Strategi

Logik teras strategi terdiri daripada tiga bahagian utama:

- Pengenalpastian corak grafik: Menggunakan kaedah tetingkap gelongsor untuk mengenal pasti corak teknikal klasik seperti dua puncak/dua lembah, kepala dan bahu, melalui perbandingan titik tinggi/rendah dan pengesahan silang EMA untuk isyarat pembalikan arah.

- Sistem pengesahan arah: Menggunakan EMA tempoh 50 sebagai penapis arah, digabungkan dengan pengesahan penembusan harga untuk menentukan arah trend, dan melalui penapis volum (memerlukan volum melebihi 120% purata 20 hari) untuk mengesahkan kesahihan isyarat.

- Sistem pengurusan risiko: Menetapkan ambang untung/rugi secara dinamik berdasarkan ATR tempoh 14, dengan menggunakan pengganda ATR 1.5 kali ganda untuk kawalan nisbah risiko-untung yang tepat.

Kelebihan Strategi

- Gabungan isyarat pelbagai dimensi: Menggabungkan maklumat pasaran daripada pelbagai dimensi seperti corak grafik, purata bergerak, volatiliti dan volum, meningkatkan kebolehpercayaan isyarat.

- Pengurusan risiko dinamik: Menggunakan ATR untuk melaraskan kedudukan ambil untung/henti rugi secara dinamik, menyesuaikan dengan persekitaran pasaran yang berbeza.

- Automasi tinggi: Sistem mengenal pasti corak, menjana isyarat dagangan dan melaksanakan pesanan secara automatik, mengurangkan campur tangan manusia.

- Visualisasi jelas: Menunjukkan isyarat dagangan secara intuitif melalui penanda grafik dan sistem amaran.

Risiko Strategi

- Risiko penembusan palsu: Dalam pasaran yang bergelora, isyarat penembusan palsu mungkin berlaku, memerlukan pengesahan volum yang ketat.

- Risiko ketinggalan: Penunjuk seperti purata bergerak dan ATR mempunyai sedikit ketinggalan, mungkin terlepas masa masuk yang optimum.

- Kepekaan parameter: Keberkesanan strategi sangat dipengaruhi oleh tetapan parameter, memerlukan pengoptimuman melalui ujian balik untuk menentukan parameter optimum.

- Kebergantungan pada persekitaran pasaran: Dalam pasaran mendatar tanpa arah yang jelas, prestasi strategi mungkin kurang memuaskan.

Arah Pengoptimuman Strategi

- Memperkenalkan pengenalan persekitaran pasaran: Menambah penunjuk kekuatan arah (seperti ADX) untuk membezakan antara pasaran bertrend dan pasaran mendatar, melaraskan parameter strategi secara dinamik.

- Mengoptimumkan penapisan isyarat: Boleh mempertimbangkan menambah penunjuk ayunan seperti RSI untuk menapis lagi isyarat penembusan palsu.

- Menambah baik kawalan risiko: Memperkenalkan sistem pengurusan saiz posisi, melaraskan saiz pegangan secara dinamik berdasarkan volatiliti pasaran.

- Meningkatkan kebolehsuaian: Membangunkan sistem parameter adaptif yang mengoptimumkan parameter strategi secara automatik berdasarkan keadaan pasaran.

Kesimpulan

Strategi ini berjaya menangkap titik perubahan arah pasaran dengan menggabungkan pelbagai penunjuk teknikal. Reka bentuk sistemnya merangkumi secara menyeluruh elemen utama seperti penjanaan isyarat, pengesahan arah dan kawalan risiko, menjadikannya sangat praktikal. Dengan arah pengoptimuman yang dicadangkan, kestabilan dan kebolehsuaian strategi dijangka dapat dipertingkatkan. Dalam aplikasi dagangan sebenar, adalah disyorkan agar pedagang menyesuaikan parameter strategi mengikut ciri pasaran tertentu dan toleransi risiko peribadi.

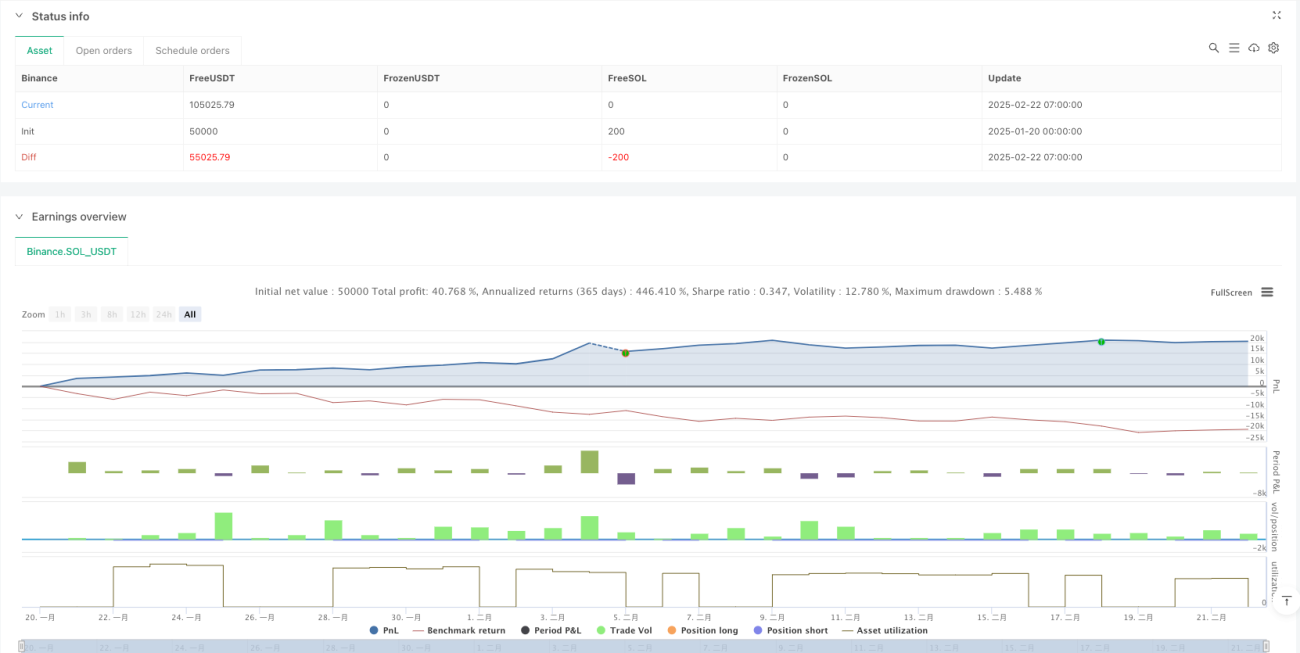

/*backtest

start: 2025-01-20 00:00:00

end: 2025-02-22 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Ultimate Pattern Finder", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// 🎯 CONFIGURABLE PARAMETERS- 1