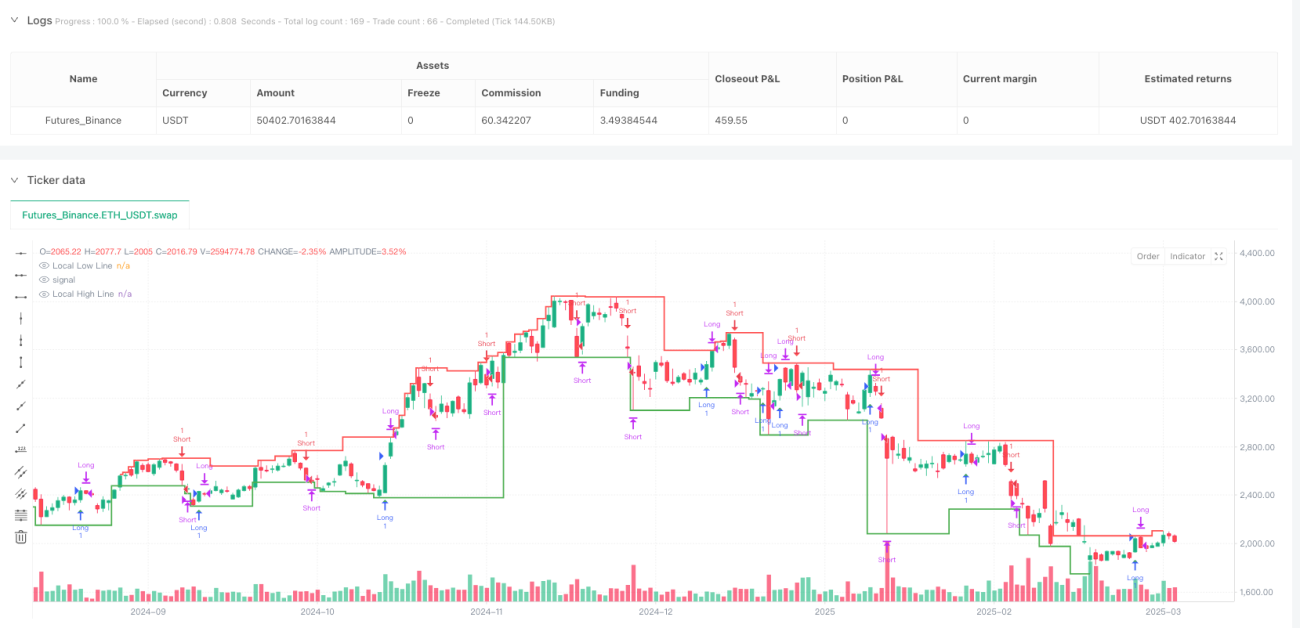

Gambaran Keseluruhan

Ini adalah strategi perdagangan inovatif yang menggabungkan analisis kawasan kecairan dan dinamik struktur pasaran dalaman, bertujuan untuk mengenal pasti titik masuk berkebarangkalian tinggi. Strategi ini mengesan interaksi harga dengan tahap pasaran utama dan menggunakan pertukaran pasaran dalaman untuk mencetuskan dagangan, menyediakan pedagang dengan kaedah masuk pasaran yang fleksibel dan tepat.

Prinsip Strategi

Logik teras strategi adalah berdasarkan dua komponen utama: pengenalpastian kawasan kecairan dan pertukaran pasaran dalaman. Kawasan kecairan ditentukan secara dinamik melalui analisis titik tinggi dan rendah tempatan, manakala pertukaran pasaran dalaman menilai perubahan arah pasaran berdasarkan penembusan harga melebihi tahap bullish atau bearish sebelumnya.

Strategi ini mempunyai ciri-ciri teras berikut:

- Logik pertukaran pasaran dalaman: Tidak bergantung pada corak lilin tradisional, tetapi berdasarkan penembusan harga pada tahap utama.

- Penjejakan kawasan kecairan: Mengenal pasti kawasan kecairan utama secara dinamik untuk mengelakkan dagangan dalam keadaan pasaran lemah.

- Fleksibiliti corak: Menyediakan tiga mod dagangan: "Kedua-duanya", "Hanya Bullish" dan "Hanya Bearish".

- Pengurusan risiko: Tahap henti rugi dan ambil untung boleh disesuaikan.

- Kawalan jangka masa: Boleh mengawal tempoh dagangan dengan tepat.

Kelebihan Strategi

- Adaptasi dinamik: Strategi dapat bertindak balas dengan cepat terhadap perubahan struktur pasaran.

- Kemasukan tepat: Menggabungkan kawasan kecairan dan pertukaran pasaran dalaman untuk meningkatkan ketepatan kemasukan.

- Risiko terkawal: Mekanisme henti rugi dan ambil untung terbina dalam.

- Fleksibiliti tinggi: Boleh memilih mod dagangan berdasarkan keadaan pasaran yang berbeza.

- Analisis pelbagai dimensi: Mempertimbangkan tingkah laku harga, kecairan dan struktur pasaran secara serentak.

Risiko Strategi

- Turun naik pasaran yang melampau boleh menyebabkan henti rugi tercetus.

- Dalam pasaran yang bergerak dalam julat, isyarat yang kerap boleh meningkatkan kos dagangan.

- Tetapan parameter yang tidak sesuai boleh menjejaskan prestasi strategi.

- Keputusan ujian semula mungkin berbeza daripada dagangan sebenar.

Hala Tuju Pengoptimuman Strategi

- Memperkenalkan algoritma pembelajaran mesin untuk pengoptimuman parameter adaptif.

- Menambah lebih banyak syarat penapisan seperti volum dagangan dan penunjuk turun naik.

- Membangunkan mekanisme pengesahan pelbagai jangka masa.

- Mengoptimumkan algoritma henti rugi dan ambil untung dengan mengambil kira pelarasan dinamik turun naik pasaran.

Ringkasan

Ini adalah strategi dagangan inovatif yang menggabungkan analisis kecairan dan dinamik struktur pasaran. Dengan logik pertukaran pasaran dalaman yang fleksibel dan penjejakan kawasan kecairan yang tepat, strategi ini menyediakan alat dagangan yang berkuasa untuk pedagang. Kuncinya terletak pada kebolehsuaian dan keupayaan analisis pelbagai dimensi, membolehkan kecekapan pelaksanaan yang tinggi dalam pelbagai keadaan pasaran.

- 1