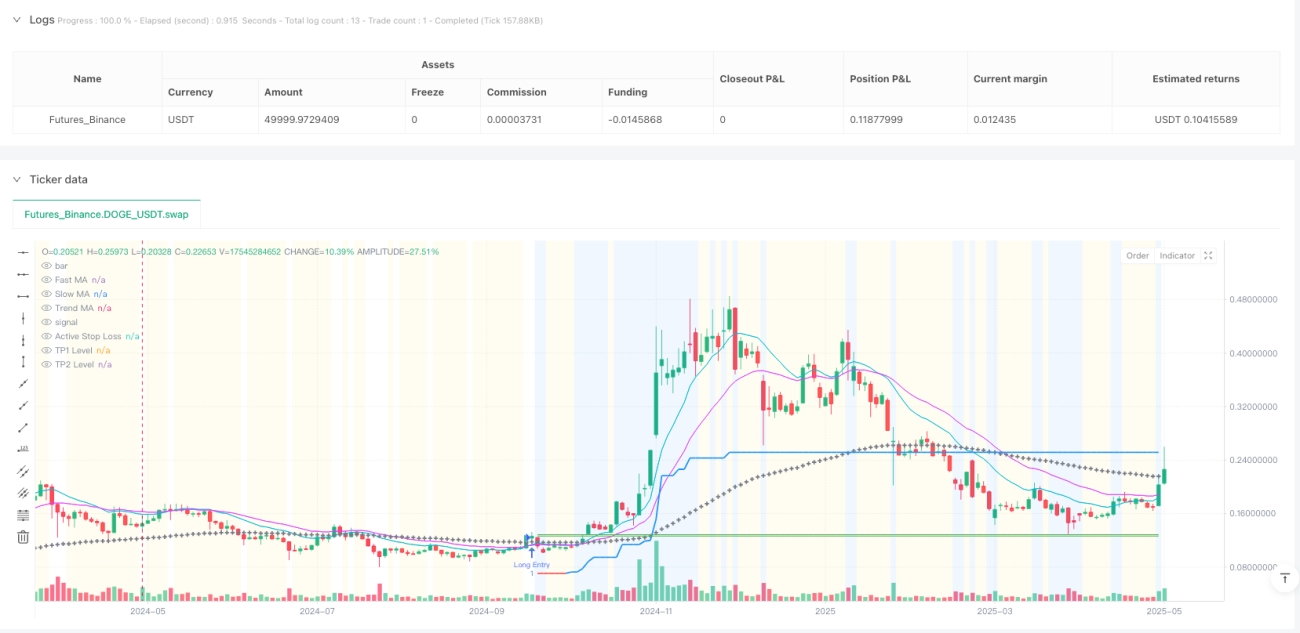

Gambaran Keseluruhan Strategi

Strategi perdagangan kuantitatif penjejakan volatiliti lintasan purata bergerak adaptif ialah strategi sistematik yang direka khusus untuk perdagangan frekuensi tinggi dan operasi jangka pendek. Teras strategi ini menggunakan lintasan antara purata bergerak pantas (MA) dan purata bergerak perlahan sebagai pencetus isyarat utama, sambil menggabungkan pelbagai penapis kritikal dan alat pengurusan risiko yang tepat untuk menangkap pergerakan harga yang kecil tetapi pantas. Strategi ini sangat boleh dikonfigurasikan, membolehkan pengguna memilih jenis purata bergerak (EMA, SMA, WMA, HMA, VWMA) dan parameter tempohnya secara fleksibel untuk menyesuaikan dengan keperluan perdagangan pelbagai rentak pasaran. Selain itu, strategi ini bersedia untuk API, membolehkan integrasi tanpa celah ke dalam sistem perdagangan automatik untuk pelaksanaan isyarat yang pantas, amat sesuai untuk pedagang jangka pendek yang mengejar keuntungan kecil frekuensi tinggi.

Prinsip Strategi

Logik teras strategi ini terbahagi kepada beberapa bahagian utama:

-

Isyarat Kemasukan: Terutamanya menggunakan lintasan/persilangan antara purata bergerak pantas dan purata bergerak perlahan sebagai keadaan pencetus kemasukan. Pengguna boleh mengkonfigurasi jenis purata bergerak (EMA, SMA, WMA, HMA, VWMA) dan panjang tempoh secara fleksibel untuk melaraskan sensitiviti isyarat, menyesuaikan dengan keadaan pasaran yang berbeza.

-

Penapis Trend: Strategi secara pilihan boleh menggunakan purata bergerak jangka panjang sebagai penapis arah aliran utama, memastikan perdagangan hanya dilakukan mengikut arah aliran utama, mengelakkan perdagangan jangka pendek menentang arah dalam pasaran berarah yang kuat.

-

Penapis Pengesahan:

- Penapis Volatiliti ATR: Direka untuk menjeda kemasukan dalam pasaran yang sangat mendatar atau "mati", di mana volatiliti berada di bawah ambang dinamik (berdasarkan purata ATR), membantu mengelakkan ayunan dalam keadaan tanpa trend dan tenaga rendah.

- Penapis Volume: Mengesahkan isyarat kemasukan dengan memerlukan penyertaan pasaran minimum (perbandingan volume dengan purata bergeraknya), mengelakkan kemasukan berdasarkan lonjakan kecairan rendah atau tingkah laku harga yang tidak signifikan.

-

Peranti Pengurusan Risiko:

- Henti Rugi Volatiliti Awal: Henti rugi awal berasaskan ATR menyediakan titik permulaan objektif untuk menentukan risiko setiap perdagangan, menyesuaikan dengan volatiliti terkini.

- Henti Rugi Jejak ATR: Penting untuk pasaran dinamik, garisan henti rugi jejak akan menyesuaikan mengikut pergerakan harga yang menguntungkan, bertujuan melindungi keuntungan dalam dagangan jangka pendek yang berjaya, sambil mengurangkan kerugian dengan agak cepat apabila arah berbalik.

- Henti Rugi Pulang Modal (Pilihan): Selepas mencapai TP1 atau harga bergerak sejauh ATR tertentu, henti rugi boleh dipindahkan secara automatik ke harga kemasukan (dengan penimbal), digunakan untuk meneutralkan risiko dagangan yang telah menunjukkan kejayaan awal dengan cepat.

- Dua Tahap Ambil Untung: Menetapkan dua sasaran ambil untung TP1 dan TP2, TP1 direka untuk mengambil untung separa dengan cepat (contohnya 50%), manakala TP2 menyasarkan ruang keuntungan yang lebih besar untuk baki kedudukan.

-

Pengurusan Kedudukan: Menggunakan saiz kedudukan kuantiti tetap, membolehkan kawalan tepat saiz kedudukan setiap dagangan, amat penting untuk penggunaan risiko yang konsisten dan penjanaan arahan API dalam persekitaran frekuensi tinggi.

Kelebihan Strategi

Melalui analisis mendalam kod, strategi ini mempunyai kelebihan jelas berikut:

-

Kebolehan Konfigurasi Tinggi: Pengguna boleh melaraskan pelbagai parameter secara fleksibel, termasuk jenis purata bergerak dan tempoh, tetapan penapis serta parameter pengurusan risiko, membolehkan strategi menyesuaikan dengan pelbagai persekitaran pasaran dan gaya perdagangan.

-

Mekanisme Penapis Pelbagai Lapisan: Menggabungkan penapis trend, volatiliti dan volume, secara berkesan mengurangkan isyarat palsu dan bunyi pasaran, meningkatkan kualiti perdagangan.

-

Pengurusan Risiko yang Menyeluruh: Strategi ini dilengkapi dengan pelbagai mekanisme henti rugi (awal, jejak, pulang modal) dan dua sasaran ambil untung, membolehkan kawalan risiko dan perlindungan keuntungan yang terperinci.

-

Reka Bentuk Mesra API: Logik kemasukan dan pengeluaran yang jelas menjana isyarat tanpa kekaburan, memudahkan integrasi dengan sistem perdagangan luaran untuk pelaksanaan pesanan yang hampir segera.

-

Kawalan Kedudukan Tepat: Saiz kedudukan kuantiti tetap memudahkan muatan titik akhir API, menjadikan pelaksanaan automatik lebih boleh dipercayai.

-

Kebolehsuaian Tinggi: Melalui pelarasan parameter, strategi boleh bertukar daripada mod perdagangan frekuensi tinggi jangka pendek kepada mod penjejakan trend jangka panjang, menyesuaikan dengan keadaan pasaran berbeza dan keutamaan peribadi.

Risiko Strategi

Walaupun strategi ini direka dengan baik, masih terdapat beberapa potensi risiko dan cabaran:

-

Risiko Pengoptimuman Parameter: Oleh kerana strategi mengandungi banyak parameter boleh dikonfigurasi, pengoptimuman berlebihan boleh menyebabkan keputusan ujian balik yang baik tetapi prestasi sebenar yang buruk (overfitting). Pelabur harus mengesahkan pada data luar sampel atau melalui ujian hadapan untuk mengelakkan risiko ini.

-

Kesan Kos Dagangan: Perdagangan frekuensi tinggi bermaksud jumlah dagangan yang banyak, komisen dan gelinciran terkumpul boleh menjejaskan keuntungan bersih dengan ketara. Pastikan kos ini dikira dengan tepat dalam tetapan dan ujian balik sebelum digunakan.

-

Turun Naik Kualiti Isyarat: Dalam keadaan pasaran berbeza, kebolehpercayaan isyarat lintasan purata bergerak mungkin berubah, terutamanya dalam pasaran mendatar atau sangat tidak menentu.

-

Kebergantungan Teknikal: Sebagai strategi bersedia API, keberkesanannya sebahagiannya bergantung pada kelajuan pelaksanaan dan kestabilan teknikal. Kependaman sistem atau kegagalan boleh menyebabkan kehilangan peluang atau penyelewengan pelaksanaan.

-

Had Saiz Dana: Saiz kedudukan kuantiti tetap mungkin tidak sesuai untuk semua saiz akaun. Akaun kecil mungkin menghadapi risiko berlebihan, manakala akaun besar mungkin tidak dapat menggunakan dana sepenuhnya.

Arah Pengoptimuman Strategi

Berdasarkan reka bentuk strategi dan potensi risiko, berikut adalah beberapa arah pengoptimuman yang mungkin:

-

Parameter Adaptif: Reka bentuk parameter utama (seperti pengganda ATR dan tempoh purata bergerak) untuk menyesuaikan secara automatik berdasarkan keadaan pasaran, meningkatkan kebolehsuaian strategi dalam fasa pasaran yang berbeza.

-

Peningkatan Penapis Pintar: Mengintegrasikan penunjuk keadaan pasaran tambahan (seperti struktur pasaran, pengiktirafan corak volatiliti atau korelasi aset berkaitan) untuk meningkatkan lagi ketepatan penapis.

-

Pengurusan Kedudukan Dinamik: Gantikan saiz kedudukan tetap dengan pengiraan kedudukan dinamik berdasarkan saiz akaun, volatiliti semasa dan prestasi strategi terkini, untuk pengurusan modal yang lebih pintar.

-

Pengesahan Pelbagai Jangka Masa: Mengesahkan isyarat pada jangka masa yang berbeza, memastikan arah perdagangan selaras dengan struktur pasaran yang lebih besar, mengurangkan dagangan yang tidak perlu.

-

Integrasi Pembelajaran Mesin: Gunakan algoritma pembelajaran mesin untuk menganalisis prestasi isyarat sejarah, meramalkan kebarangkalian kejayaan isyarat masa depan, dan mengutamakan pelaksanaan dagangan berkemungkinan tinggi.

-

Pengurusan Sesi Dagangan: Tambah penapis waktu dagangan untuk mengelakkan tempoh kecairan rendah atau volatiliti tinggi, fokus pada tetingkap dagangan yang paling cekap.

-

Penapis Korelasi: Untuk dagangan berbilang aset, tambah analisis korelasi dengan pasaran berkaitan untuk mengelakkan pendedahan berlebihan kepada faktor risiko tertentu.

Ringkasan

Strategi perdagangan kuantitatif penjejakan volatiliti lintasan purata bergerak adaptif ialah sistem perdagangan frekuensi tinggi yang berfungsi sepenuhnya, menggunakan lintasan purata bergerak sebagai pencetus isyarat, digabungkan dengan pelbagai penapis kritikal dan alat pengurusan risiko yang tepat, direka khusus untuk menangkap pergerakan harga yang kecil tetapi pantas. Kekuatan strategi ini terletak pada kebolehan konfigurasi yang tinggi dan rangka kerja pengurusan risiko yang menyeluruh, membolehkan pedagang melaraskan parameter perdagangan dengan tepat mengikut toleransi risiko dan keadaan pasaran masing-masing.

Bagi pedagang frekuensi tinggi, strategi ini menyediakan logik kemasukan dan pengeluaran yang jelas, serta keupayaan integrasi tanpa celah dengan platform pelaksanaan luaran, yang amat penting untuk pelaksanaan keputusan yang pantas dalam pasaran yang berubah dengan cepat. Walau bagaimanapun, apabila menggunakan strategi ini, perhatian khusus harus diberikan kepada kos dagangan terkumpul dan risiko pengoptimuman berlebihan, memastikan keteguhan dan keuntungan strategi dalam dagangan sebenar.

Akhirnya, strategi ini mewakili pendekatan yang seimbang – memanfaatkan kuasa penunjuk teknikal dan alat pengurusan risiko, sambil mengekalkan kelenturan yang mencukupi untuk menyesuaikan dengan keadaan pasaran yang sentiasa berubah. Melalui pelarasan parameter yang teliti dan penambahbaikan pemantauan berterusan, strategi ini boleh menjadi komponen berharga dalam portfolio perdagangan kuantitatif.

- 1