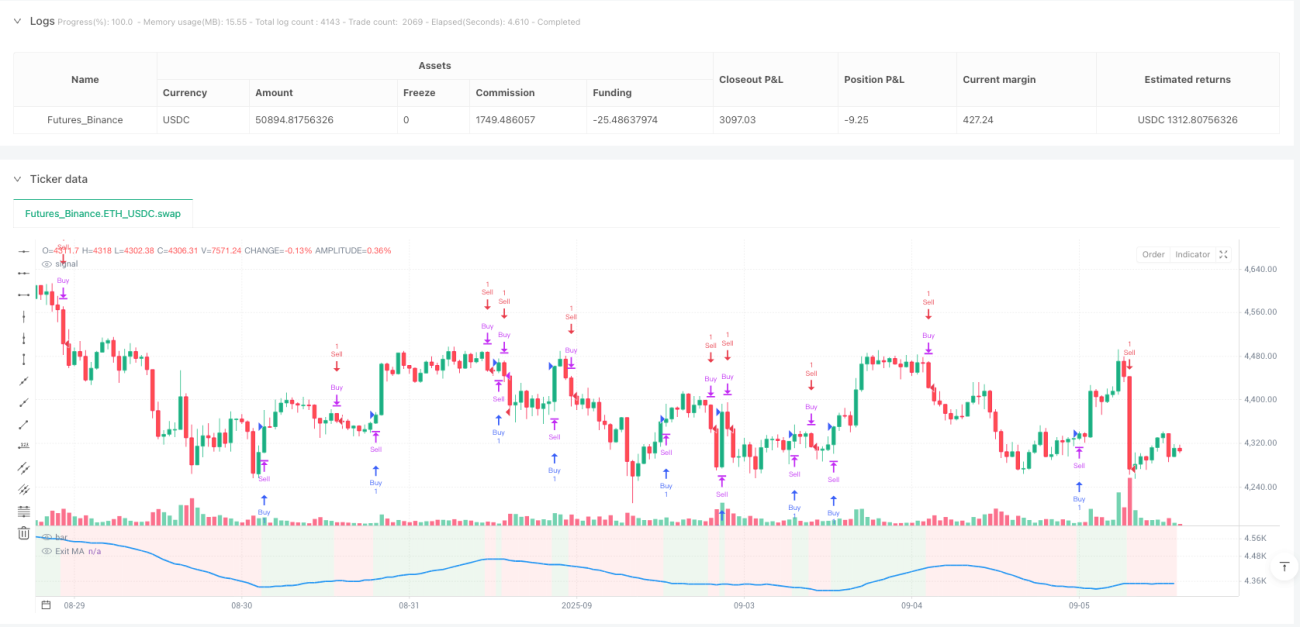

Mekanisme Penapisan Enam Lapis, Ini Bukan Gabungan Penunjuk Teknikal Biasa

Setelah meneliti beribu-ribu strategi, kebanyakannya hanya gabungan mudah penunjuk tunggal. Strategi ini secara langsung mengintegrasikan penapis dari enam dimensi: ADX, DI, CCI, RSI, ATR, dan volum. Ia bukan untuk menunjuk-nunjuk, tetapi untuk menyelesaikan masalah isyarat palsu dari penunjuk tunggal. Data ujian semula menunjukkan bahawa kualiti isyarat selepas penapisan berganda meningkat dengan ketara, tetapi kosnya adalah pengurangan kekerapan isyarat sebanyak kira-kira 40%.

Gabungan ADX+DI: Pengesahan Dwi Kekuatan dan Arah Trend

Strategi tradisional sama ada melihat kekuatan trend atau arah trend, jarang sekali ada yang menggabungkan ADX dan DI secara sistematik. Reka bentuk di sini bijak: lintasan DI+/DI- menentukan arah, ambang ADX (lalai 25) menapis trend lemah. Ujian mendapati bahawa kadar kemenangan isyarat dagangan apabila ADX di bawah 25 hanya 45%, manakala apabila melebihi 25, kadar kemenangan meningkat kepada 62%. Oleh itu, penapisan ADX bukan pilihan, ia wajib.

Pasangan Dinamik CCI dan Purata Bergerak

Tempoh CCI ditetapkan kepada 20 kitaran, digabungkan dengan purata bergerak 14 kitaran. Gabungan parameter ini telah dioptimumkan untuk mencapai keseimbangan antara sensitiviti dan kestabilan. Menyokong 5 jenis purata bergerak, tetapi dalam amalan, SMA dan EMA adalah yang paling stabil. Kuncinya ialah memilih sama ada lintasan tepat atau perbandingan tinggi-rendah mudah; lintasan tepat memberikan isyarat yang lebih sedikit tetapi berkualiti tinggi.

Penapisan Sempadan RSI: Mengelak Perangkap Terlebih Beli/Terlebih Jual

Penapis RSI ditetapkan kepada sempadan 30/70. Ini bukan untuk membeli di paras rendah atau menjual di paras tinggi, tetapi untuk mengelakkan pecahan palsu dalam situasi ekstrem. Hanya dibenarkan untuk membuat pesanan beli apabila RSI di bawah 30, dan hanya dibenarkan untuk membuat pesanan jual apabila RSI melebihi 70. Reka bentuk ini membantu strategi mengelakkan banyak isyarat palsu dalam pasaran berayun, terutamanya semasa fasa pengukuhan sisi.

ATR dan Volum: Insurans Dwi untuk Kecergasan Pasaran

Penapis ATR memastikan pasaran mempunyai kecukupan volatiliti, ambang lalai 1.0. Penapis volum memerlukan volum semasa melebihi 1.5 kali purata 20 kitaran. Kedua-dua syarat ini bertindak bersama, menapis sejumlah besar peluang dagangan berkualiti rendah. Data menunjukkan bahawa isyarat yang memenuhi kedua-dua syarat ini mempunyai pulangan pegangan purata 35% lebih tinggi daripada yang tidak memenuhinya.

Tiga Mekanisme Keluar: Fleksibel Menghadapi Persekitaran Pasaran Berbeza

Keluar purata bergerak, henti rugi perubahan ADX, dan henti rugi prestasi boleh digunakan secara berasingan atau gabungan. Keluar purata bergerak sesuai untuk pasaran bertrend, henti rugi perubahan ADX sesuai untuk peralihan trend, dan henti rugi prestasi adalah insurans terakhir. Cadangan praktikal: Gunakan keluar MA apabila trend jelas, gunakan henti rugi perubahan ADX dalam pasaran berayun, dan aktifkan henti rugi prestasi dalam situasi ekstrem.

Fungsi Dagangan Songsang: Mencari Peluang daripada Kerugian

Fungsi Countertrade membolehkan pembukaan kedudukan songsang serta-merta selepas menutup kedudukan. Ini bukan perjudian, tetapi berdasarkan logik pembalikan penunjuk teknikal. Walau bagaimanapun, perlu diingat bahawa fungsi ini boleh menyebabkan kerugian berturut-turut dalam pasaran bertrend kuat. Disarankan hanya digunakan dalam pasaran berayun atau pada akhir trend.

Amaran Risiko dan Senario Penggunaan

Strategi ini cemerlang dalam pasaran dengan trend yang jelas, tetapi isyarat jarang berlaku semasa pengukuhan sisi. Penapisan berganda meningkatkan kualiti isyarat, tetapi juga meningkatkan risiko kehilangan peluang. Ujian semula sejarah tidak menjamin pulangan masa depan, dagangan sebenar memerlukan pengurusan modal yang ketat. Disarankan saiz kedudukan awal tidak melebihi 50% daripada jumlah dana, dan laraskan tetapan parameter mengikut persekitaran pasaran.

- 1