7

Follow

359

Followers

Compartilhando a lógica da estratégia de arbitragem de diferença de preço à vista em várias bolsas

Created 2022-06-27 21:26:27 Updated 2024-12-02 21:35:44

4

10034

Princípio da estratégia

Devido a razões de liquidez, quando há uma grande quantidade de venda ou retirada no mercado, inevitavelmente haverá grandes flutuações de preço, e haverá uma diferença momentânea de preço entre as bolsas. A estratégia é capturar esses momentos e executar transações rápidas para conclua o processo de comprar barato e vender caro. .

Alguns clientes me perguntaram por que tenho tantas exchanges. Isso é inevitável. O que ganhamos dinheiro é a diferença instantânea de preço entre as exchanges. Quanto mais exchanges houver, mais oportunidades de diferença de preço haverá após o crossover.

Lógica central da estratégia

- Obtenha simultaneamente as informações de mercado de várias bolsas. É necessário obtê-las simultaneamente para reduzir o atraso na obtenção das informações de mercado. Para aquisição simultânea, você pode consultar o plug-in de ferramenta que compartilhei.Plugin simultâneo de múltiplas trocas

- Combine o preço de venda e o preço de compra de todas as bolsas para obter informações de cotação combinadas, onde RealPrice é o preço após a dedução da taxa de manuseio.

function createOrders(depths, askOrders, bidOrders) {

let asksIndex = 0;

let bidIndex = 0;

for (let i = 0; i < depths.length; i++) {

let exchangeTariff = getExchangeTariff(i);

let asks = depths[i].Asks;

let bids = depths[i].Bids;

for (let j = 0; j < Math.min(asks.length, bids.length, 20); j++) {

if (asks[j].Amount >= minTakerAmount) {

askOrders[asksIndex] = {

"Price": asks[j].Price,

"Amount": asks[j].Amount,

"Fee": asks[j].Price * exchangeTariff,

"RealPrice": asks[j].Price * (1 + exchangeTariff),

"Index": i,

};

asksIndex++;

}

if (bids[j].Amount >= minTakerAmount) {

bidOrders[bidIndex] = {

"Price": bids[j].Price,

"Amount": bids[j].Amount,

"Fee": bids[j].Price * exchangeTariff,

"RealPrice": bids[j].Price * (1 - exchangeTariff),

"Index": i,

};

bidIndex++;

}

}

}

askOrders.sort(function (a, b) {

return a.RealPrice - b.RealPrice;

});

bidOrders.sort(function (a, b) {

return b.RealPrice - a.RealPrice;

});

}

- Calcule o spread de arbitragem mais lucrativo a partir das informações de mercado combinadas. Como estamos recebendo ordens, ou seja, comprando pelo menor preço de venda e vendendo pelo maior preço de oferta, desde que bid.RealPrice > ask.RealPrice, há espaço para lucro

function getArbitrageOrders(askOrders, bidOrders) {

let ret = [];

for (let i = 0; i < askOrders.length; i++) {

for (let j = 0; j < bidOrders.length; j++) {

let bidOrder = bidOrders[j];

let askOrder = askOrders[i];

if (bidOrder.Index === askOrder.Index) {

continue

}

let minMigrateDiffPrice = ((askOrder.Price + bidOrder.Price) / 2 * minMigrateDiffPricePercent / 100);

if (bidOrder.RealPrice - askOrder.RealPrice > minMigrateDiffPrice) {

ret.push({

"Ask": askOrder,

"Bid": bidOrder,

})

}

}

}

if (ret.length === 0) {

ret.push({

"Ask": askOrders[0],

"Bid": bidOrders[0],

});

}

//按最优价差排序

ret.sort((a, b) => {

return (b.Bid.RealPrice - b.Ask.RealPrice) - (a.Bid.RealPrice - a.Ask.RealPrice);

});

return ret;

}

- Agora que obtivemos as informações de spread de arbitragem no mercado, como decidimos se executamos a transação e quanto negociar? Aqui estão alguns pontos-chave a serem considerados:

- Ativos remanescentes atuais

- O tamanho do spread (se o spread for muito pequeno, ele apenas equilibrará a quantidade de moeda e, se o spread for grande o suficiente, ele maximizará o número de transações)

- Número de pedidos pendentes

var askOrder = arbitrageOrder.Ask;

var bidOrder = arbitrageOrder.Bid;

var perAmountFee = arbitrageOrder.Ask.Fee + arbitrageOrder.Bid.Fee;

var minRealDiffPrice = (askOrder.Price + bidOrder.Price) / 2 * minDiffPricePercent / 100;

var minMigrateDiffPrice = ((askOrder.Price + bidOrder.Price) / 2 * minMigrateDiffPricePercent / 100);

var curRealDiffPrice = arbitrageOrder.Bid.RealPrice - arbitrageOrder.Ask.RealPrice;

var buyExchange = exchanges[arbitrageOrder.Ask.Index];

var sellExchange = exchanges[arbitrageOrder.Bid.Index];

var buySellAmount = 0;

if (curRealDiffPrice > minRealDiffPrice) {

buySellAmount = math.min(

bidOrder.Amount,

askOrder.Amount,

maxTakerAmount,

runningInfo.Accounts[bidOrder.Index].CurStocks,

runningInfo.Accounts[askOrder.Index].CurBalance / askOrder.Price

);

} else if (bidOrder.Index !== askOrder.Index) {

if (migrateCoinEx == -1) {

if (curRealDiffPrice > minMigrateDiffPrice && runningInfo.Accounts[bidOrder.Index].CurStocks - runningInfo.Accounts[askOrder.Index].CurStocks > maxAmountDeviation) {

buySellAmount = math.min(

bidOrder.Amount,

askOrder.Amount,

maxTakerAmount,

runningInfo.Accounts[bidOrder.Index].CurStocks,

runningInfo.Accounts[askOrder.Index].CurBalance / askOrder.Price,

runningInfo.Accounts[bidOrder.Index].CurStocks - ((runningInfo.Accounts[bidOrder.Index].CurStocks + runningInfo.Accounts[askOrder.Index].CurStocks) / 2)

);

if (buySellAmount >= minTakerAmount) {

Log("启动交易所平衡!");

}

}

} else if (migrateCoinEx == askOrder.Index) {

if (curRealDiffPrice > minMigrateDiffPrice && runningInfo.Accounts[bidOrder.Index].CurStocks > 0) {

buySellAmount = math.min(

bidOrder.Amount,

askOrder.Amount,

maxTakerAmount,

runningInfo.Accounts[bidOrder.Index].CurStocks,

runningInfo.Accounts[askOrder.Index].CurBalance / askOrder.Price

);

if (buySellAmount >= minTakerAmount) {

Log("启动货币迁移:", exchanges[bidOrder.Index].GetName(), "-->", exchanges[askOrder.Index].GetName());

}

}

}

}

- Uma vez que a quantidade do pedido é calculada, a transação pode ser executada. A estratégia usa o método de adicionar slippage diretamente para receber pedidos e fazer pedidos ao mesmo tempo

var buyWait = buyExchange.Go("Buy", _N(askOrder.Price * (1.01), pricePrecision), buySellAmount);

var sellWait = sellExchange.Go("Sell", _N(bidOrder.Price * (0.99), pricePrecision), buySellAmount);

var startWaitTime = new Date().getTime()

Sleep(3000);

var buyOrder = buyWait.wait()

var sellOrder = sellWait.wait()

- O que resta é a lógica de calcular lucros, lidar com stop losses para ordens falhadas, etc.

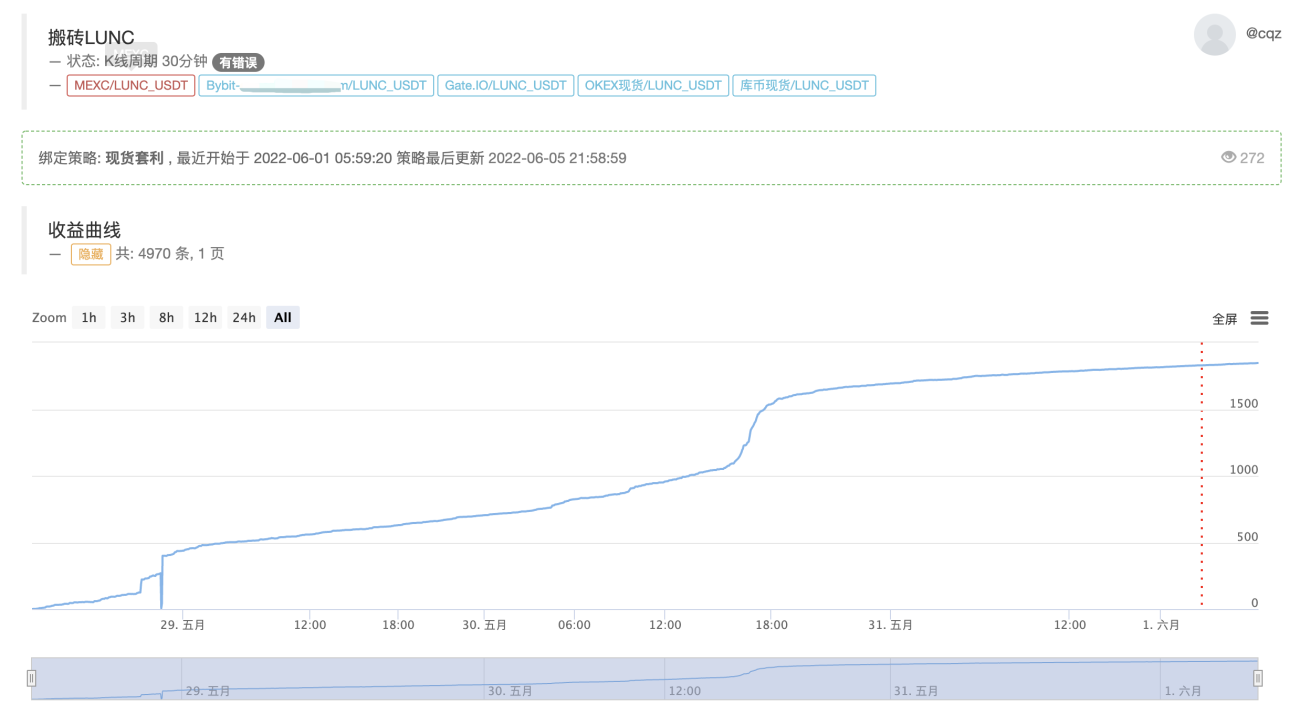

Os benefícios reais desta estratégia

Exibição atual em tempo real, lógica central permanece inalterada, otimizada para suportar múltiplas moedas

https://www.fmz.com/robot/464965

Por fim, bem-vindo para se juntar à Laoqiu Quantitative Exchange: https://t.me/laoqiu_arbitrage

Related Recommendations

Cryptocurrency spot hedging strategy design(2)An example of general protocol contract access on FMZMulti-Exchange Spot Spread Arbitrage Strategy Logic SharingVisualization module to build trading strategies - in-depthUse the KLineChart function to make strategy drawing design easierJavaScript strategy backtesting is debugged in DevTools of Chrome browserDetailed Explanation of Equilibrium & Grid StrategiesDesign a Multiple-Chart Plotting LibraryRSI2 Mean Reversion Strategy using in futuresThe futures and cryptocurrency API explanation

Comment

All comments (4)

- 1