Estratégia de gestão de capital dinâmica multifatorial

Visão Geral

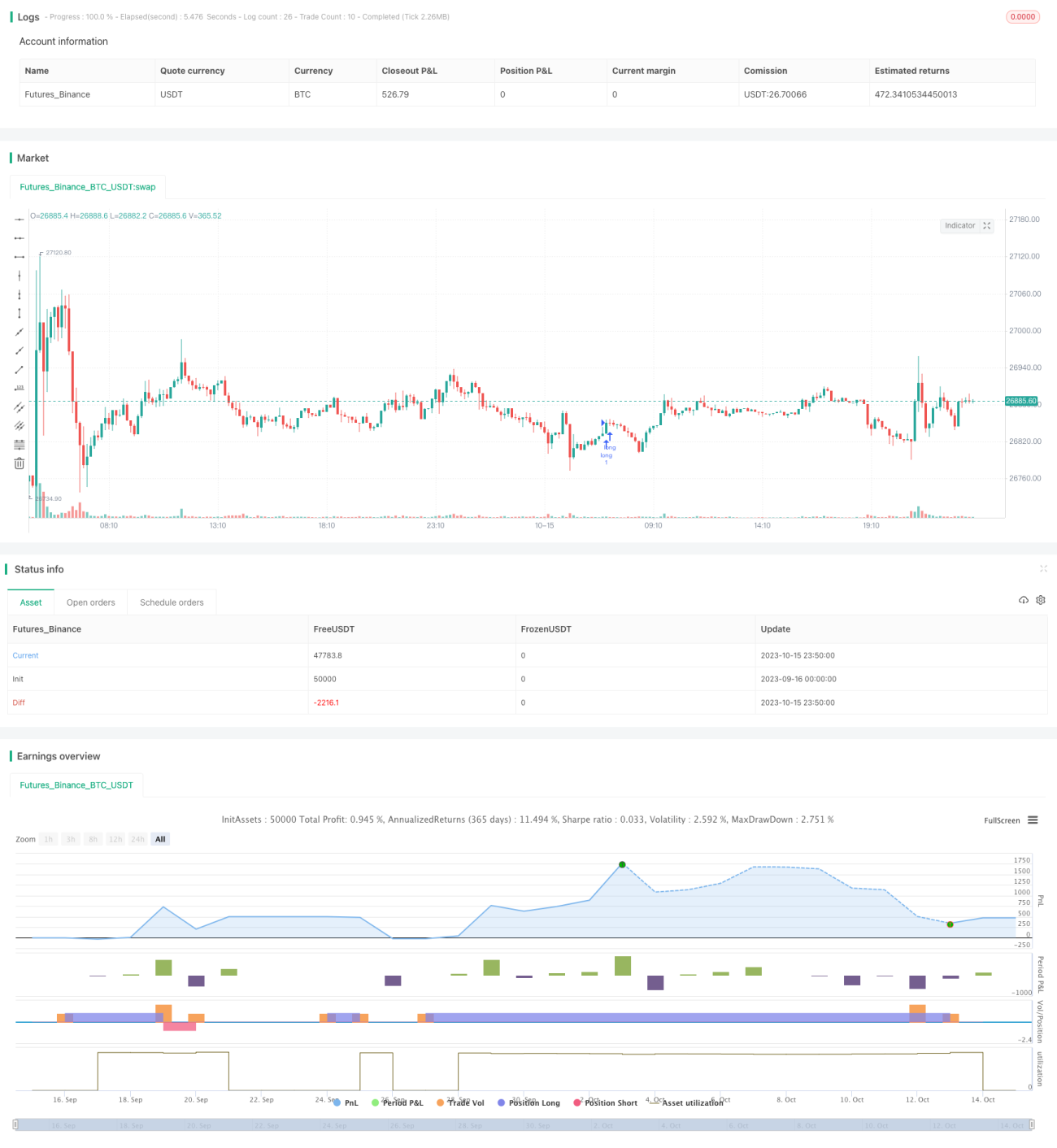

Esta estratégia combina o uso de múltiplos indicadores técnicos como MACD, RSI, PSAR e princípios de gestão dinâmica de capital para realizar rastreamento de tendências e negociações de reversão em múltiplos prazos. A estratégia pode ser aplicada a negociações de curto, médio e longo prazo.

Princípio

A estratégia utiliza o indicador PSAR para determinar a direção da tendência. O cruzamento das médias móveis EMA rápida e lenta com a linha média das Bandas de Bollinger serve como primeiro ponto de confirmação. A direção das barras do histograma MACD é o segundo ponto de confirmação. A região de sobrecompra/sobrevenda do RSI é o terceiro ponto de confirmação. Quando todas as condições acima são atendidas, um sinal de negociação é gerado.

Após a entrada, são definidos pontos de stop loss e take profit. O stop loss é definido com base em um múltiplo do valor ATR. O take profit segue o mesmo princípio. Simultaneamente, é definido um stop loss percentual de perda flutuante, que interrompe a posição quando a perda atinge uma proporção específica do patrimônio total da conta.

Também existe uma configuração percentual para lucro flutuante, que encerra a posição quando o lucro atinge uma proporção específica do patrimônio total da conta.

A gestão dinâmica de capital calcula o tamanho da posição com base no patrimônio total da conta, no ATR e no múltiplo de stop loss definido. Além disso, é estabelecido um volume mínimo de negociação.

Vantagens

- Confirmação multifatorial, evitando falsos rompimentos e aumentando a precisão das entradas.

- Gestão dinâmica de capital controla o risco por operação, protegendo efetivamente a conta.

- Stop loss e take profit baseados no ATR, ajustáveis de acordo com a volatilidade do mercado.

- Configurações percentuais de perda/lucro flutuante garantem os lucros e evitam reversões.

Riscos

- A combinação multifatorial pode perder algumas oportunidades de negociação.

- Configurações percentuais muito altas podem ampliar as perdas.

- Valores inadequados de ATR podem resultar em stop loss/take profit excessivamente amplos ou agressivos.

- Parâmetros de gestão de capital inadequados podem levar a posições excessivamente grandes.

Direções de Otimização

- Ajustar os pesos dos fatores de entrada para otimizar a precisão dos sinais.

- Testar diferentes configurações de parâmetros percentuais para encontrar a melhor combinação.

- Escolher múltiplos de ATR razoáveis de acordo com as características de cada ativo.

- Ajustar dinamicamente os parâmetros de gestão de capital com base nos resultados do backtest.

- Otimizar a configuração de períodos, testando diferentes horários de negociação.

Resumo

Esta estratégia combina múltiplos indicadores técnicos para determinar tendências, incorpora gestão dinâmica de capital para controle de risco e busca obter lucros estáveis em múltiplos prazos. É possível continuar otimizando os pesos dos fatores, parâmetros de risco e configurações de gestão de capital com base nos resultados do backtest para obter melhores resultados.

- 1