Estratégia de Rompimento com Trailing

Visão Geral

Esta estratégia implementa principalmente uma estratégia de negociação de breakout baseada no indicador "Canal de Donchian". Ela combina duas abordagens de negociação: tendência e breakout. Com base na identificação de tendências de longo prazo, busca pontos de breakout de curto prazo para realizar entradas, aproveitando o movimento favorável da tendência. Além disso, a estratégia define níveis de stop loss e take profit para controlar a relação risco-retorno de cada operação. No geral, a estratégia possui a vantagem de acompanhar a tendência, permitindo atuar a favor dela e capturar oportunidades de tendências de longo prazo.

Princípio da Estratégia

-

Definir os parâmetros do indicador "Canal de Donchian", padrão de 20 períodos.

-

Definir a Média Móvel Exponencial (EMA), padrão de 200 períodos.

-

Definir a relação risco-retorno, padrão de 1,5.

-

Definir os parâmetros de pullback do breakout, separadamente para posições compradas e vendidas.

-

Registrar se o último breakout foi de máxima ou mínima.

-

Sinal de compra: se o último breakout foi de mínima, e o preço está acima da banda superior do Donchian e acima da EMA, gera sinal de compra.

-

Sinal de venda: se o último breakout foi de máxima, e o preço está abaixo da banda inferior do Donchian e abaixo da EMA, gera sinal de venda.

-

Ao entrar em posição comprada, definir stop loss como a banda inferior do Donchian menos 5 ticks, e take profit como a relação risco-retorno multiplicada pela distância do stop loss.

-

Ao entrar em posição vendida, definir stop loss como a banda superior do Donchian mais 5 ticks, e take profit como a relação risco-retorno multiplicada pela distância do stop loss.

Dessa forma, a estratégia combina a identificação de tendências com operações de breakout, permitindo atuar a favor da tendência e capturar oportunidades de curto prazo dentro de uma tendência de longo prazo. Ao mesmo tempo, a definição de stop loss e take profit controla o risco-retorno de cada operação.

Análise de Vantagens

-

Acompanha tendências de longo prazo, atuando a favor delas, evitando operações contrárias.

-

O Canal de Donchian como indicador de longo prazo, combinado com o filtro da EMA, permite uma boa identificação da direção da tendência.

-

O mecanismo de stop loss e take profit controla o risco de cada operação, limitando possíveis perdas.

-

A otimização da relação risco-retorno pode ampliar a relação lucro-prejuízo, buscando retornos excessivos.

-

Os parâmetros de backtest são flexíveis, permitindo ajustar a melhor combinação de parâmetros para diferentes mercados.

Análise de Riscos

-

O Canal de Donchian e a EMA como indicadores de filtro podem gerar sinais falsos.

-

As operações de breakout são propensas a serem enganadas, exigindo a identificação clara do contexto da tendência.

-

As distâncias de stop loss e take profit são fixas, não podendo ser ajustadas de acordo com a volatilidade do mercado.

-

O espaço de otimização de parâmetros é limitado, e o desempenho em mercado real é difícil de garantir.

-

O sistema de negociação não resiste bem a muitos eventos aleatórios; eventos de cisne negro podem causar grandes perdas.

Direções de Otimização

-

Pode-se considerar adicionar mais indicadores para filtro, como osciladores, melhorando a qualidade dos sinais.

-

Pode-se implementar stop loss e take profit inteligentes, ajustando dinamicamente as posições de lucro e perda com base na volatilidade do mercado e no indicador ATR.

-

Podem-se utilizar métodos como aprendizado de máquina para testar e otimizar os parâmetros, tornando-os mais próximos do mercado real.

-

Pode-se otimizar a lógica de entrada, incluindo indicadores de volume ou volatilidade como condições auxiliares para evitar armadilhas.

-

Pode-se considerar combinar com estratégias de acompanhamento de tendência ou aprendizado de máquina, formando uma estratégia híbrida para aumentar a estabilidade.

Resumo

Esta estratégia, como uma estratégia de breakout baseada em acompanhamento de tendência, tem como núcleo a premissa de identificar uma tendência de longo prazo, utilizando breakouts como sinal para operar a favor da tendência, e definindo stop loss e take profit para controlar o risco de cada operação. A estratégia possui certas vantagens, mas também apresenta espaço para otimização. No geral, se a definição de parâmetros e a escolha do momento de entrada forem bem tratadas, e com a adição de outras técnicas para aprimoramento, esta estratégia pode se tornar uma ferramenta prática de acompanhamento de tendência. No entanto, os investidores devem lembrar que nenhum sistema de negociação pode evitar completamente os riscos de mercado, sendo necessário um bom gerenciamento de risco.

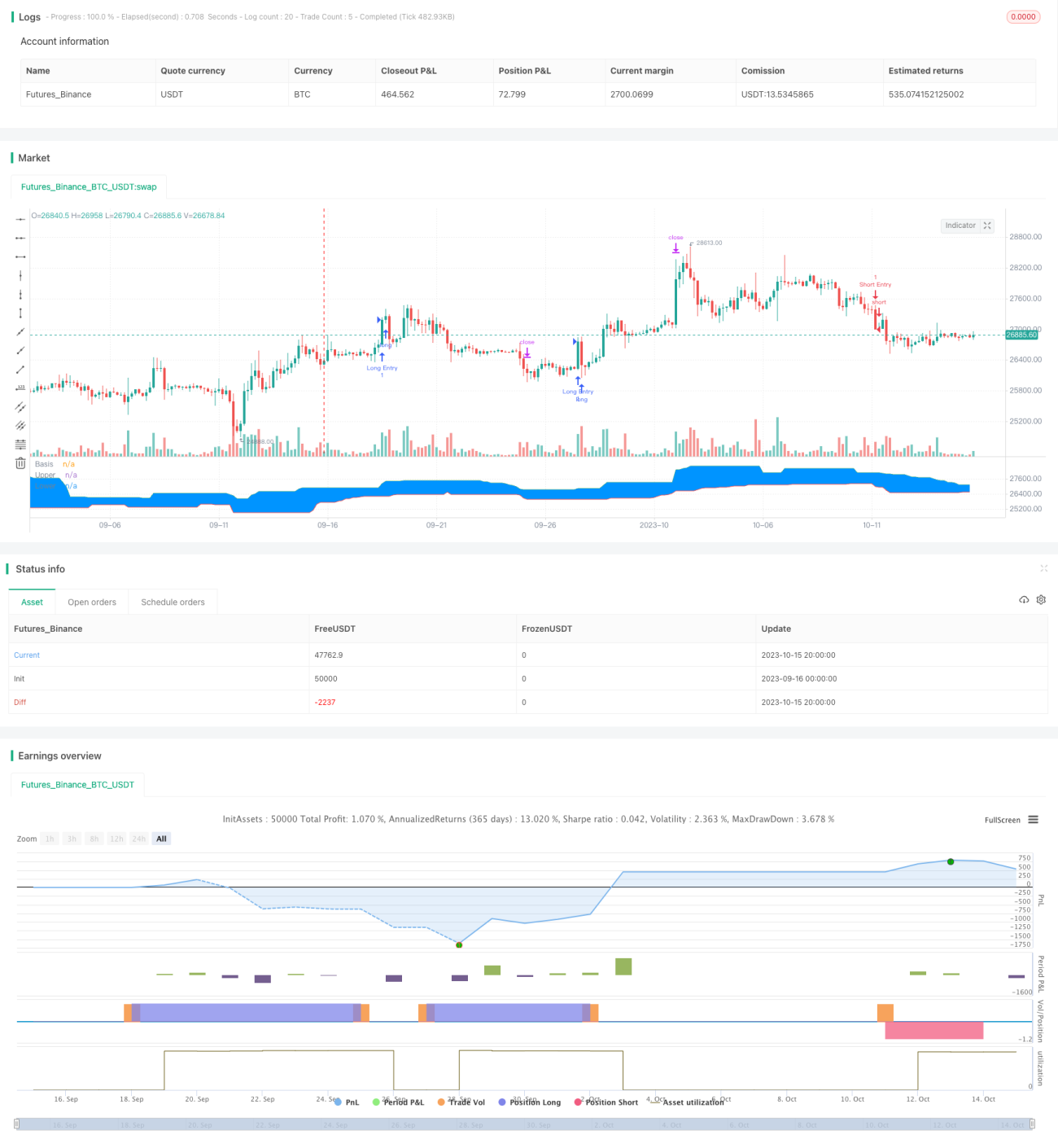

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1