Estratégia de Trading de Oscilação com Padrão Triplo

Visão Geral

A estratégia de negociação de oscilação de padrão triplo é uma estratégia de curto prazo baseada na combinação de múltiplos indicadores técnicos. Ela combina o indicador Super Trend, a Média Móvel Mista SSL e o indicador QQE Modificado para gerar sinais de negociação estáveis. É adequada para ativos de alta volatilidade, como criptomoedas e ações, especialmente após períodos de rompimento.

Princípio

Sinal de Entrada

Entrada em posição longa:

- Super Trend muda de baixa para alta

- Preço de fechamento cruza acima da banda superior da Média Móvel Mista SSL

- QQE Modificado está azul (alta)

Entrada em posição curta:

- Super Trend muda de alta para baixa

- Preço de fechamento cruza abaixo da banda inferior da Média Móvel Mista SSL

- QQE Modificado está vermelho (baixa)

Sinal de Saída

Saída de posição longa: Super Trend muda de alta para baixa

Saída de posição curta: Super Trend muda de baixa para alta

Stop Loss

Pode escolher stop loss percentual, stop loss ATR ou stop loss baseado na máxima/mínima recente.

Take Profit

Pode definir uma proporção de retorno para take profit, calculando automaticamente o preço de take profit.

Gestão de Capital

Opção de usar lógica de gestão de capital para controlar o tamanho da posição.

Plotagem

- Desenha a linha Super Trend e o canal da Média Móvel Mista SSL

- Opção de desenhar ou não a Média Móvel EMA

- Desenha as linhas de abertura, stop loss e take profit para posições longas e curtas

- Desenha rótulos de abertura para posições longas e curtas

Vantagens

-

Combinação de múltiplos indicadores gera sinais estáveis

A combinação de Super Trend, Média Móvel Mista SSL e QQE Modificado permite que diferentes indicadores se validem mutuamente, filtrando falsos rompimentos e gerando sinais de alta qualidade. -

Adequado para negociação de oscilação em ativos voláteis

A estratégia adota negociação de curto prazo, focando em capturar flutuações de preço de médio-curto prazo. O Super Trend acompanha eficazmente a tendência de preço, enquanto a Média Móvel Mista SSL identifica claramente níveis de suporte e resistência; a combinação dos dois pode gerar ganhos em mercados laterais. -

Múltiplas opções de stop loss e take profit

O stop loss pode ser percentual, ATR ou extremo recente. O take profit pode definir uma proporção de retorno. A gestão de capital permite controlar o tamanho da posição. O usuário pode combinar livremente de acordo com as características do ativo e sua tolerância ao risco. -

Plotagem clara

A plotagem da estratégia é clara, mostrando visualmente os níveis de stop loss e take profit. As marcações de abertura de posição facilitam a identificação dos sinais.

Riscos e Otimização

-

Possibilidade de pequenas perdas

Devido à negociação de curto prazo, pequenas perdas comuns em oscilações normais não podem ser totalmente evitadas. É possível ajustar a amplitude do stop loss ou otimizar a lógica de gestão de capital. -

Risco de falso rompimento

Quando o preço apresenta um falso rompimento, pode gerar sinais incorretos. Pode-se testar EMAs de diferentes períodos para filtrar falsos rompimentos ou otimizar os parâmetros dos indicadores de identificação de tendência. -

Risco de falha dos indicadores subjacentes

Se os indicadores básicos falharem, podem surgir múltiplos sinais incorretos. É necessário verificar periodicamente a eficácia dos indicadores e ajustá-los rapidamente ao detectar problemas. -

Otimização do período de backtest

O período de backtest atual é fixo, não correspondendo aos diferentes ciclos de mercado do ativo. Recomenda-se otimizar para corresponder ao período principal de negociação do contrato. -

Adequação ao ativo

Os parâmetros da estratégia podem ser ajustados finamente de acordo com as características dos dados de cada ativo para melhorar a taxa de acerto de posições longas e curtas. Recomenda-se usar otimização por passos para comparar o impacto de diferentes parâmetros na estratégia.

Conclusão

Esta estratégia combina vários indicadores para gerar sinais de negociação, filtrando eficazmente falsos rompimentos, sendo adequada para criptomoedas e ações individuais de alta volatilidade. Além disso, oferece diversas opções de stop loss e take profit, proporcionando flexibilidade de uso. No geral, a estratégia gera sinais de negociação estáveis e pode obter bons retornos em mercados laterais de curto prazo. Com otimizações adicionais, é possível ajustar os parâmetros para diferentes ativos, aumentando o fator de lucro da estratégia. Esta é uma estratégia eficiente que merece estudo aprofundado.

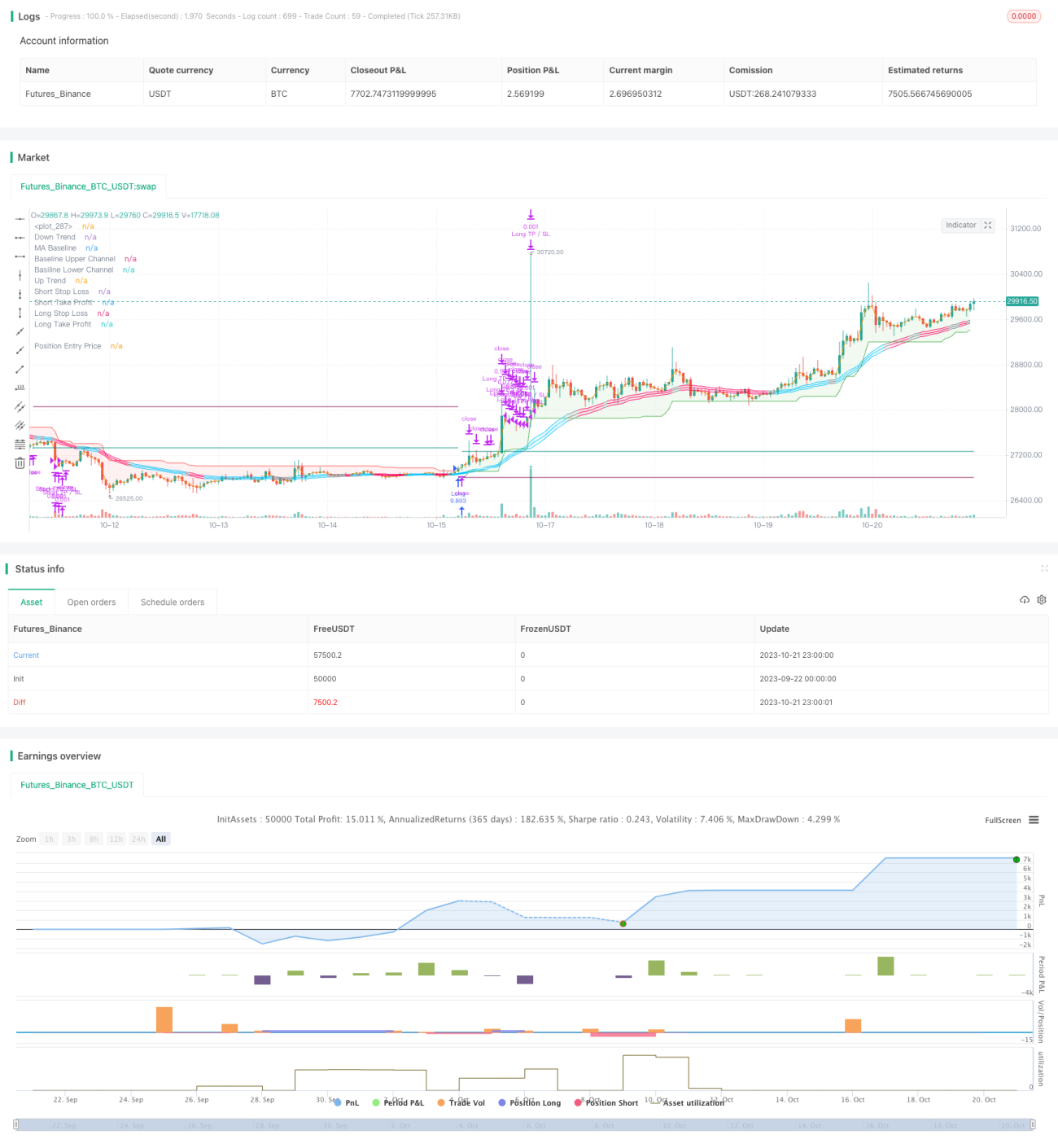

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1