Estratégia de compra em correção de queda

Visão Geral

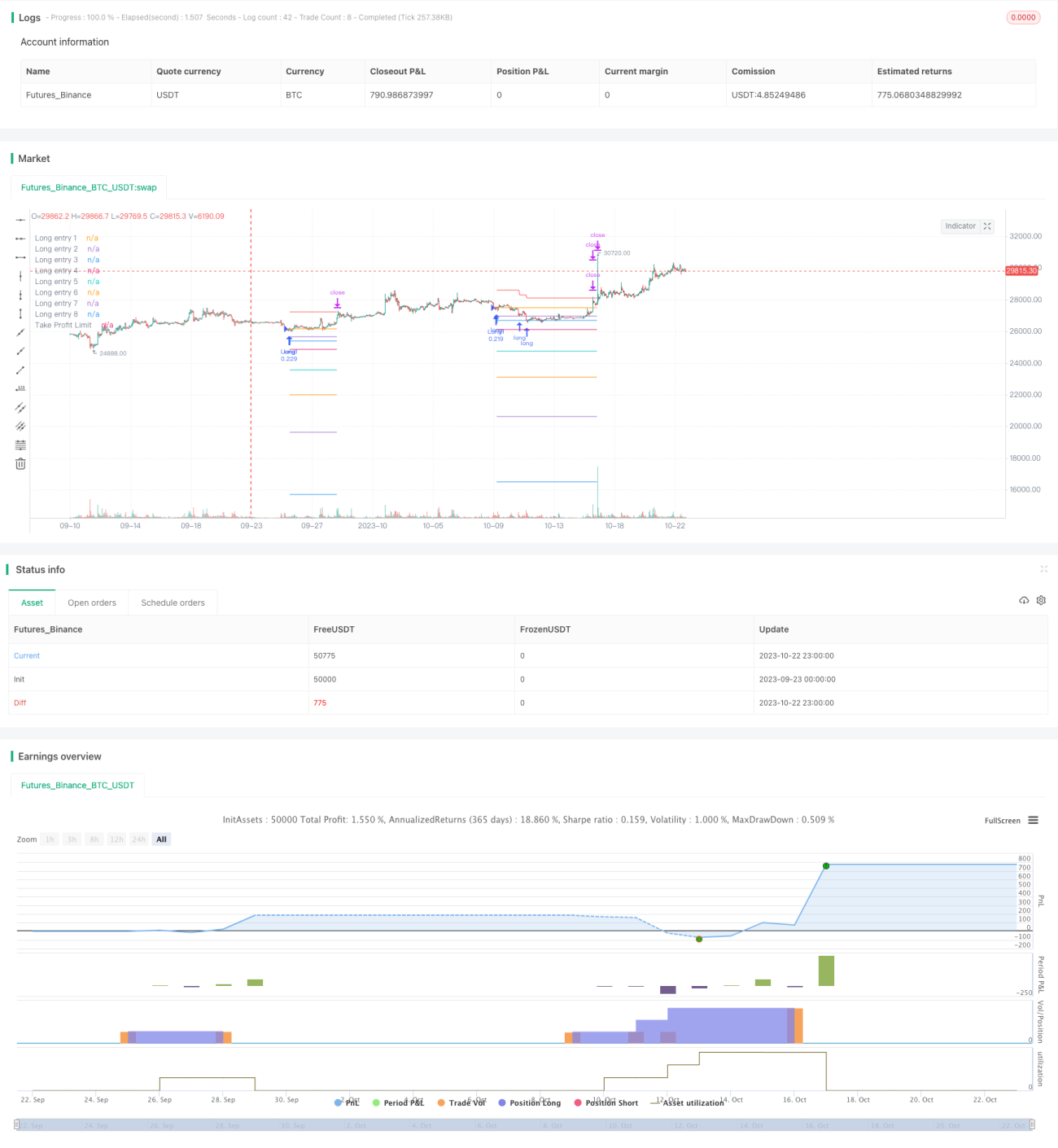

Esta estratégia combina o indicador RSI com uma média móvel de preços, procurando oportunidades de sobrevenda quando o preço da ação cai abaixo da média móvel para abrir posições compradas. À medida que o preço cai ainda mais, a estratégia adiciona camadas sucessivas conforme uma porcentagem predefinida, com o objetivo de obter um custo médio de posição. Quando o lucro da posição atinge a porcentagem de take profit configurada, a estratégia opta por fechar a posição. Simultaneamente, a estratégia introduz um mecanismo de take profit progressivo, ajustando dinamicamente o preço de take profit da posição total com base nos lucros já realizados de cada lote individual. Isso reduz efetivamente o risco de perda, permitindo uma saída gradual.

Princípio da Estratégia

-

Quando o indicador RSI está abaixo da linha de sobrevenda de 29 e o preço de fechamento está abaixo da média móvel, abre-se a primeira ordem de compra.

-

Quando o preço cai 2% em relação à primeira ordem, adiciona-se uma nova posição comprada; quando a queda atinge 3%, adiciona-se pela terceira vez, e assim sucessivamente até um máximo de 8 adições. Isso permite o efeito de acumulação gradual de posições.

-

Após cada abertura de posição, registra-se o preço de abertura naquele momento. Esses pontos de preço servem como referência de entrada. As linhas desses preços são desenhadas no gráfico.

-

Após abrir as posições, calcula-se o preço médio da posição total. Utiliza-se 3% do preço médio como take profit de cada lote e 4% como take profit da posição total.

-

Quando o preço sobe acima do take profit de um determinado lote, opta-se por fechar aquele lote.

-

Cálculo do take profit progressivo: a cada lote fechado, subtrai-se o lucro realizado desse lote do preço de take profit total. Isso faz com que a linha de take profit desça lentamente, e só quando o lucro de todos os lotes for suficiente para cobrir a perda máxima, toda a posição é fechada com lucro.

-

Quando o preço atinge a linha de take profit progressivo, opta-se por fechar toda a posição.

Análise de Vantagens

-

O indicador RSI pode identificar com precisão as zonas de sobrevenda, favorecendo a captura de oportunidades de reversão.

-

Adicionar posições em várias etapas permite obter um custo médio mais baixo nos pontos de queda.

-

O take profit progressivo reduz o risco de perda, permitindo uma saída gradual. Mesmo em caso de perda, esta pode ser controlada dentro de certos limites.

-

As porcentagens de take profit e adição de posições são configuráveis, permitindo ajustar o risco da estratégia conforme o mercado.

-

A representação gráfica das linhas de referência de abertura e take profit permite visualizar a distribuição das posições.

Análise de Riscos

-

Em mercados laterais, a estratégia pode acionar aberturas e take profits repetidamente, gerando frequentes negociações e custos de spread. Pode-se ajustar os parâmetros do RSI para reduzir o número de negociações.

-

Uma definição inadequada do número e da porcentagem de adições pode levar a excesso de negociações. Deve-se configurar com cuidado, considerando o capital disponível.

-

Se o mercado continuar caindo após as adições, pode haver risco de perda ilimitada. Deve-se definir um limite máximo de adições e manter uma porcentagem conservadora na última camada.

-

Se a porcentagem de take profit for muito pequena, pode resultar em saída precoce. Deve-se determinar a porcentagem adequada com base em dados históricos de backtest.

Direções de Otimização

-

Pode-se introduzir indicadores como MACD para filtrar os sinais do RSI, reduzindo negociações ineficazes.

-

Pode-se definir stop loss baseado no ATR para evitar grandes perdas em condições extremas de mercado.

-

Pode-se otimizar parâmetros como número de adições, porcentagens e take profit para adaptar a estratégia a diferentes ativos.

-

Pode-se ajustar dinamicamente a porcentagem de take profit com base na volatilidade, afrouxando-a em momentos de alta volatilidade.

Resumo

Esta estratégia aproveita o indicador RSI para identificar zonas de sobrevenda e, combinado com a média móvel de preços, realiza operações de reversão. Utiliza mecanismos inteligentes de adição de posições e take profit progressivo, permitindo uma estratégia de compra eficiente com controle de risco. Otimizando os parâmetros dos indicadores e o mecanismo de take profit, a estratégia pode se tornar mais estável e eficiente. Pode ser amplamente aplicada a ativos financeiros com características de reversão de tendência, como futuros de índices, criptomoedas, etc., possuindo valor prático de investimento.

- 1