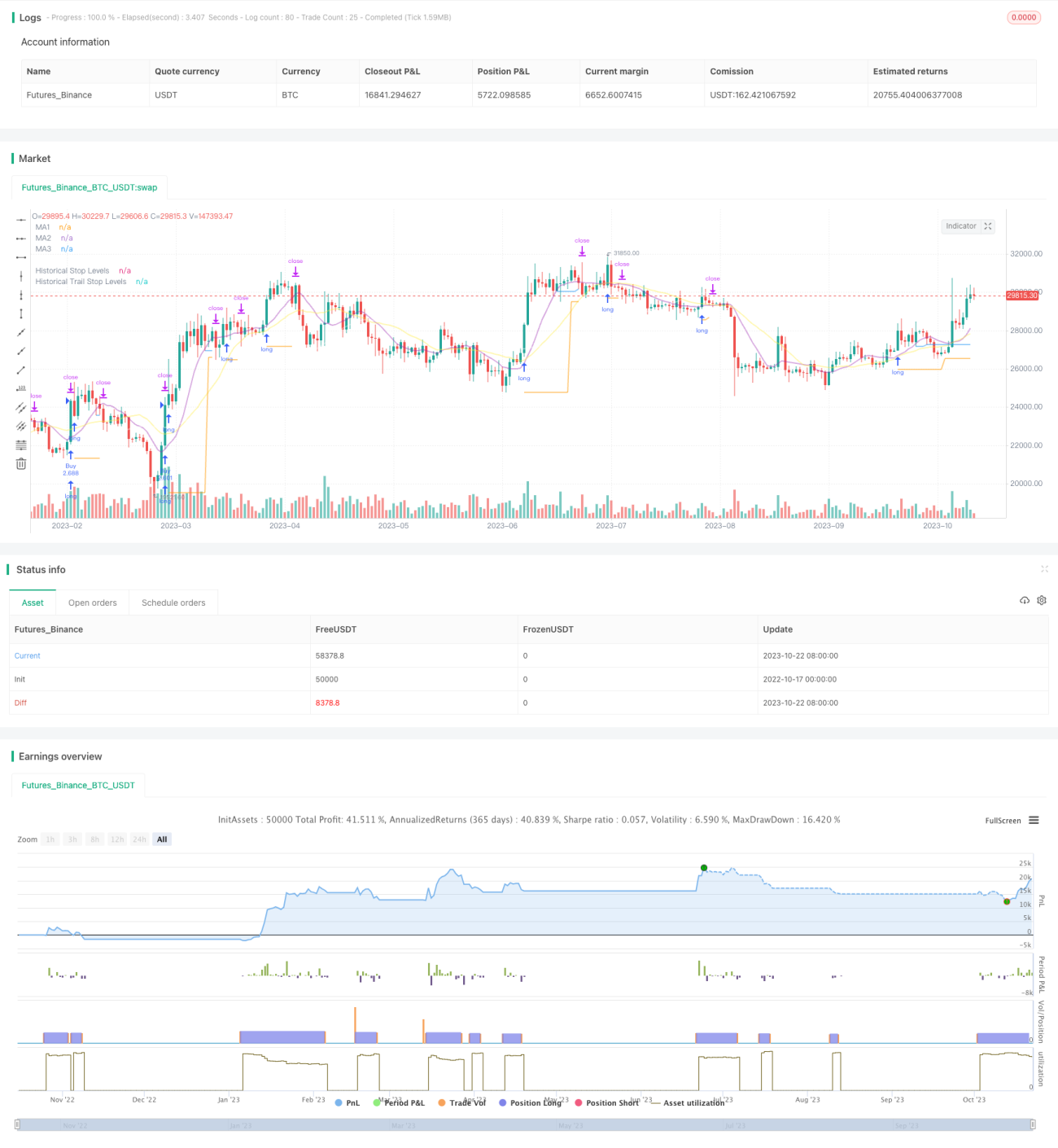

Estratégia de Trailing Stop com Breakout V2

Visão Geral

Esta estratégia combina as vantagens de uma estratégia de rompimento (breakout) e de uma estratégia de trailing stop baseada em tendência, com o objetivo de capturar sinais de rompimento de suporte e resistência em gráficos de longo prazo, ao mesmo tempo que utiliza médias móveis para realizar um trailing stop, permitindo lucrar na direção da tendência de longo prazo enquanto controla o risco.

Princípio da Estratégia

-

A estratégia primeiro calcula vários grupos de médias móveis com diferentes parâmetros, que são usados respectivamente para julgamento de tendência, suporte/resistência e trailing stop.

-

Em seguida, identifica os pontos mais altos e mais baixos dentro de um período especificado como zonas de suporte e resistência para entrada. Quando o preço rompe esses níveis, um sinal é gerado.

-

A estratégia utiliza o rompimento do ponto mais alto como sinal de compra (long) e o rompimento do ponto mais baixo como sinal de venda (short).

-

Após a entrada, a posição é mantida usando o ponto mais baixo rompido como stop loss.

-

Quando a posição entra em lucro, o stop loss é alterado para um trailing stop baseado em média móvel. Quando o preço cai abaixo da média móvel, o stop é ajustado para o ponto mais baixo daquele candle.

-

Dessa forma, é possível travar lucros enquanto dá espaço suficiente para a posição acompanhar a tendência.

-

A estratégia também incorpora o Average True Range (ATR) para garantir que o rompimento só ocorra em faixas adequadas, evitando rompimentos excessivamente amplos.

Análise das Vantagens da Estratégia

-

Combina as vantagens duais da estratégia de rompimento e da estratégia de trailing stop baseada em tendência.

-

Pode comprar rompimentos com base na tendência de longo prazo, aumentando a probabilidade de lucro.

-

A estratégia de stop loss protege a posição ao mesmo tempo que dá espaço suficiente para a posição se movimentar.

-

Inclui filtro de volatilidade para evitar rompimentos desfavoráveis excessivos.

-

Negociação automatizada, adequada para acompanhamento parcial.

-

Permite personalizar médias móveis de diferentes períodos para operar.

-

Ajuste flexível do método de trailing stop.

Análise de Riscos da Estratégia

-

Estratégias de rompimento são propensas a falsos rompimentos. Pode-se relaxar a confirmação do rompimento adequadamente.

-

É necessária volatilidade suficiente para gerar sinais de rompimento; em mercados instáveis pode ser ineficaz.

-

Alguns rompimentos podem ser muito curtos para serem capturados. Pode-se reduzir o timeframe para encontrar mais oportunidades.

-

O trailing stop pode ser acionado com muita frequência em mercados laterais. Pode-se aumentar a distância do stop adequadamente.

-

O filtro de volatilidade pode perder algumas oportunidades. Pode-se reduzir o parâmetro do filtro.

Direções de Otimização da Estratégia

-

Testar diferentes combinações de parâmetros de médias móveis para encontrar os melhores parâmetros.

-

Testar diferentes mecanismos de confirmação de rompimento, como canais, formações de candles, etc.

-

Experimentar diferentes métodos de trailing stop para encontrar o melhor stop.

-

Otimizar a estratégia de gerenciamento de capital, como position sizing.

-

Adicionar filtros de indicadores técnicos estatísticos para melhorar a precisão do filtro.

-

Testar a eficácia da estratégia em diferentes ativos.

-

Incorporar algoritmos de aprendizado de máquina para melhorar o desempenho da estratégia.

Resumo

Esta estratégia integra o conceito de rompimento com o pensamento de trailing stop baseado em tendência. Se o julgamento de longo prazo estiver correto, pode otimizar o espaço de lucro. A chave é encontrar a melhor combinação de parâmetros e combiná-la com uma boa estratégia de gerenciamento de capital para capturar oportunidades de longo prazo enquanto controla o risco. Esta estratégia tem potencial para se tornar uma estratégia de tendência de longo prazo confiável após otimizações adicionais.

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1