Estratégia de Tendência de Curto Prazo Baseada em Decisão de Indicadores Multidimensionais

Visão Geral

Esta estratégia combina três indicadores técnicos de diferentes dimensões: níveis de suporte e resistência, sistema de médias móveis e indicadores de sobrecompra/sobrevenda. Com base nos sinais combinados desses indicadores, ela determina a direção da tendência de curto prazo, visando obter uma alta taxa de acerto.

Princípio da Estratégia

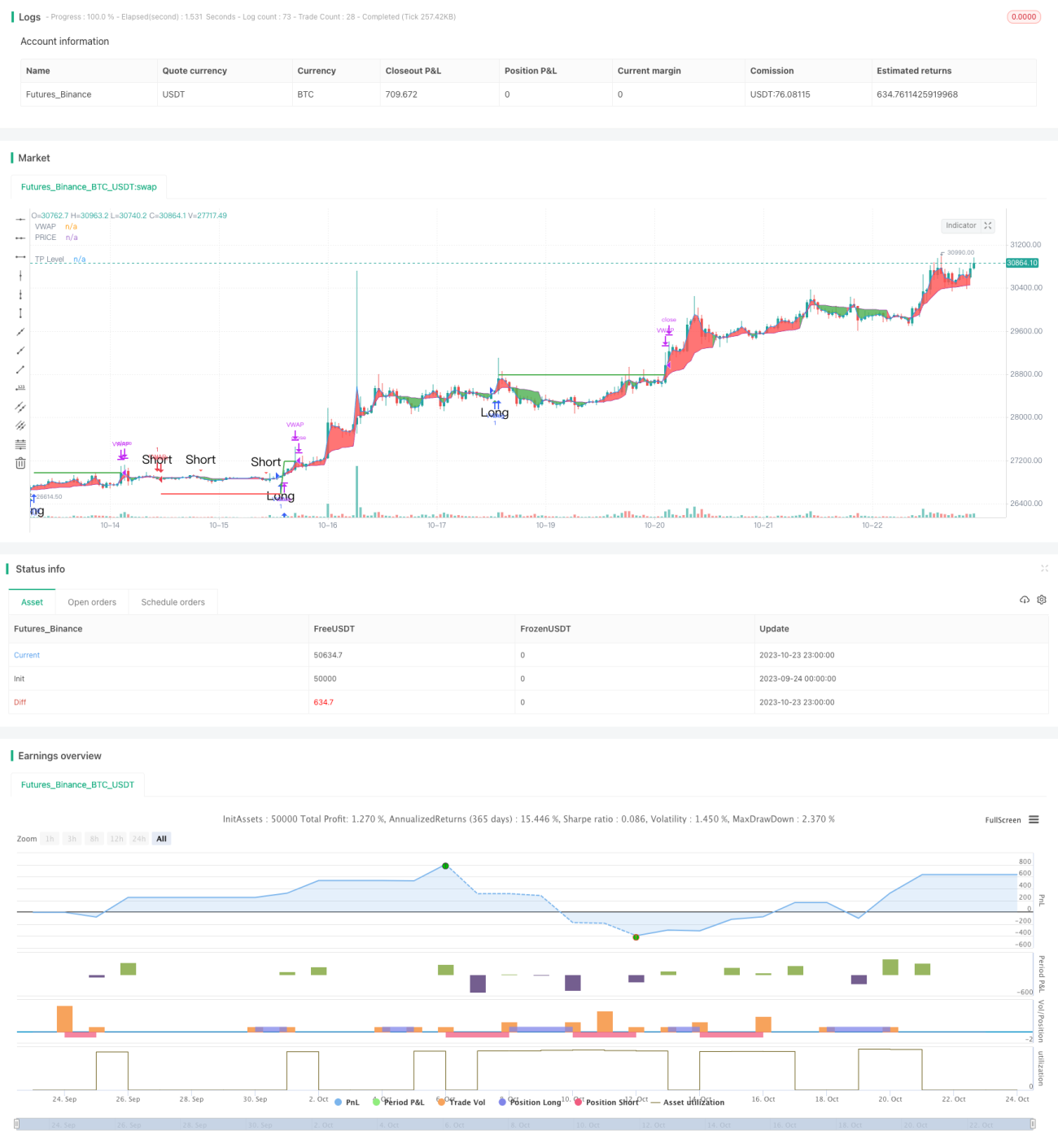

No código, primeiro são calculados os níveis de suporte e resistência do preço, incluindo o eixo oscilatório padrão e os níveis de suporte e resistência de Fibonacci, que são plotados no gráfico. Quando o preço rompe esses níveis-chave, isso é considerado um sinal importante de tendência.

Em seguida, calcula-se a Média Móvel Ponderada por Volume (VWAP) e a média de preço, analisando os sinais de cruzamento de ouro e cruzamento da morte. Isso pertence à avaliação de tendência de médio a longo prazo.

Por fim, calcula-se o indicador Stochastic RSI, avaliando seus sinais de cruzamento de ouro e cruzamento da morte, que é um indicador de sobrecompra/sobrevenda.

Combinando esses três indicadores de diferentes dimensões, se os níveis de suporte/resistência, a média VWAP e o Stochastic RSI emitirem simultaneamente um sinal de compra, uma posição longa é aberta; se os três emitirem simultaneamente um sinal de venda, uma posição curta é aberta.

Análise de Vantagens

A maior vantagem desta estratégia é a combinação de três indicadores de diferentes dimensões, tornando o julgamento mais abrangente e preciso, com alta taxa de acerto. Primeiro, os níveis de suporte/resistência avaliam a grande tendência; em segundo lugar, o VWAP avalia a tendência de médio a longo prazo; por último, o Stochastic RSI avalia as condições de sobrecompra/sobrevenda. A emissão simultânea de sinais pelos três indicadores filtra grande parte dos sinais falsos, aumentando a taxa de sucesso na entrada.

Além disso, a estratégia inclui uma função de realização de lucros (take profit), que pode travar uma porcentagem de ganhos, favorecendo a gestão de capital.

Análise de Riscos

O principal risco desta estratégia reside na dependência de sinais sincronizados dos indicadores para decisões de compra/venda. Se algum indicador emitir um sinal errado, pode levar a uma decisão equivocada. Por exemplo, se o Stochastic RSI emitir um sinal de sobrecompra, mas o VWAP e os níveis de suporte/resistência ainda indicarem alta, pode-se perder um ponto de entrada.

Além disso, parâmetros inadequados dos indicadores também podem levar a julgamentos errôneos, exigindo repetidos backtests para encontrar os parâmetros ideais.

Adicionalmente, eventos de cisne negro no mercado de ações, de curto prazo, podem invalidar os indicadores. Para mitigar esse risco, pode-se adicionar uma estratégia de stop loss, evitando perdas excessivas em uma única operação.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

-

Adicionar mais sinais de indicadores, como volume de negociação, para avaliar a força da tendência e melhorar a precisão das decisões.

-

Incorporar modelos de aprendizado de máquina para treinar com múltiplas dimensões de indicadores, buscando automaticamente a estratégia de negociação ideal.

-

Otimizar parâmetros de acordo com diferentes ativos, configurando parâmetros adaptativos.

-

Adicionar estratégias de stop loss e controlar o tamanho da posição com base no drawdown, para melhor gerenciamento de risco.

-

Realizar otimização de portfólio, selecionando ativos com baixa correlação para compor uma carteira, reduzindo o drawdown geral.

Resumo

No geral, esta estratégia é muito adequada para negociação de tendências de curto prazo. Ela utiliza indicadores multidimensionais para tomada de decisão, filtrando grande parte do ruído e proporcionando alta taxa de acerto. No entanto, deve-se atentar ao risco de sinais falsos dos indicadores; com otimizações contínuas, esta estratégia tem potencial para se tornar uma estratégia de curto prazo eficiente e estável.

- 1