Estratégia de Rompimento do RSI Acumulado

Visão Geral

Esta estratégia utiliza o indicador RSI acumulado para identificar tendências, realizando operações de compra e venda quando o valor acumulado do RSI ultrapassa limiares críticos. A estratégia consegue filtrar eficazmente o ruído do mercado, capturando oportunidades de negociação de tendências de médio a longo prazo.

Princípio da Estratégia

A estratégia baseia-se principalmente no indicador RSI acumulado para tomar decisões de negociação. O RSI acumulado é a soma acumulada dos valores do RSI durante um período definido pelo parâmetro cumlen. Este indicador pode filtrar o ruído de curto prazo do mercado.

Quando o RSI acumulado cruza acima da banda superior de Bollinger, é executada uma ordem de compra (abertura de posição); quando cruza abaixo da banda inferior, é executada uma ordem de venda (fechamento de posição). As bandas superior e inferior de Bollinger são calculadas com base em dados históricos de vários anos, constituindo níveis de referência dinâmicos.

Além disso, a estratégia inclui um filtro de tendência opcional. Uma posição de compra só é aberta se o preço estiver acima da média móvel de 100 dias, ou seja, quando se encontra num canal de tendência de alta. Este filtro evita negociações incorretas durante períodos de oscilação de preços.

Vantagens da Estratégia

- Utiliza o RSI acumulado para filtrar ruídos eficazmente, capturando tendências de médio a longo prazo.

- Inclui um filtro de tendência para evitar negociações inadequadas.

- Utiliza níveis de referência dinâmicos (bandas de Bollinger) em vez de valores fixos para as decisões.

- Vários parâmetros configuráveis para adaptação a diferentes mercados.

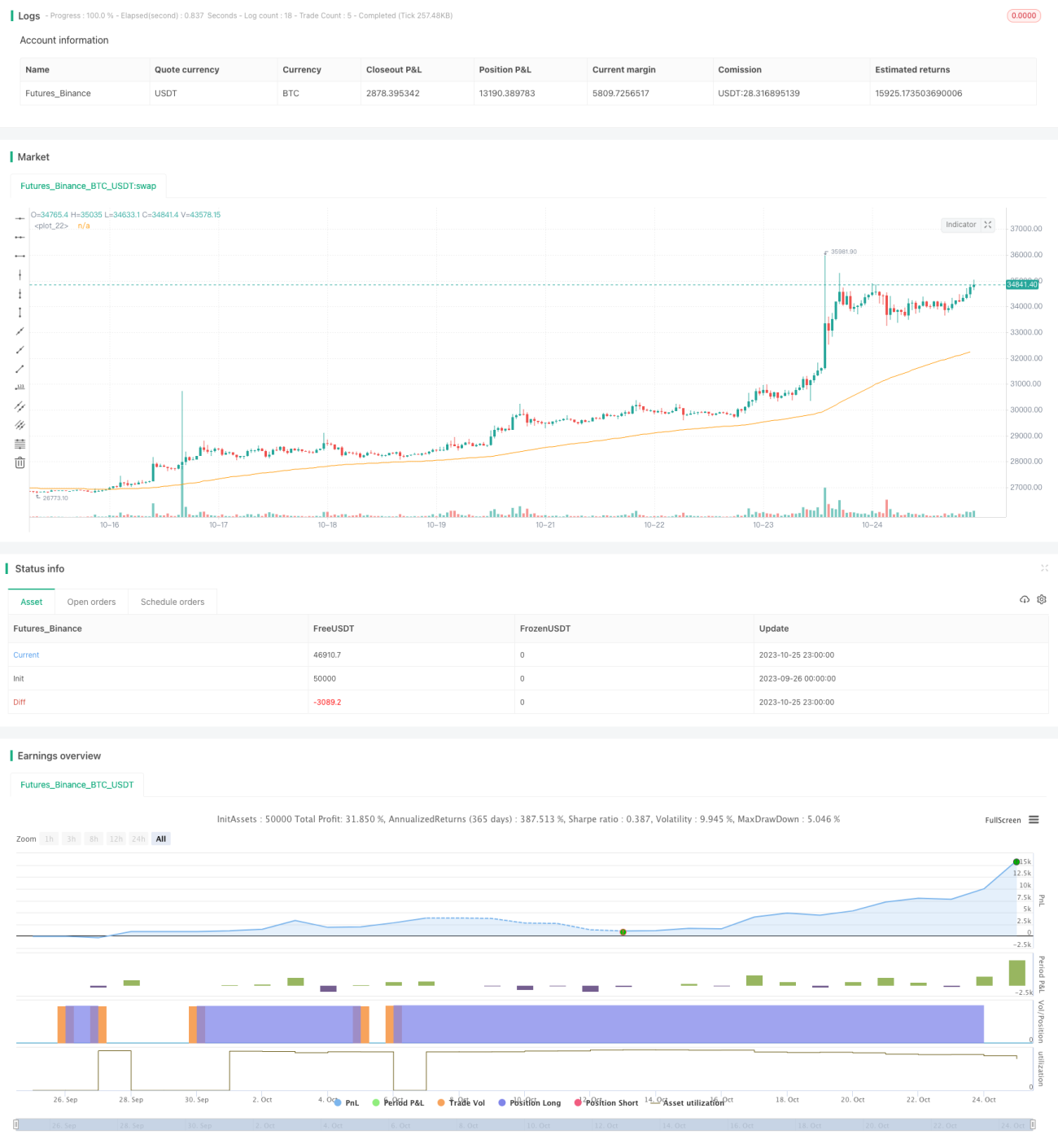

- Resultados excelentes em backtests de 10 anos, com retornos muito superiores à estratégia de buy-and-hold.

Riscos e Melhorias da Estratégia

- A estratégia baseia-se apenas num único indicador (RSI acumulado) para tomar decisões. Poderiam ser adicionados outros indicadores ou filtros para uma análise mais abrangente.

- A alavancagem fixa é elevada; poderia ser ajustada com base no drawdown.

- Opera apenas em posições longas; poderia considerar oportunidades de venda a descoberto.

- Os parâmetros podem ser otimizados, uma vez que configurações diferentes podem ser mais adequadas em diferentes condições de mercado.

- As condições de fecho poderiam ser enriquecidas com stop loss, trailing stop, entre outras.

- A estratégia poderia ser combinada com outras para obter efeitos sinérgicos.

Resumo

A Estratégia de Rompimento do RSI Acumulado é fluida e logicamente clara. Através do RSI acumulado para filtrar ruídos e da adição de um filtro de tendência, capta com precisão as tendências de médio a longo prazo, apresentando um desempenho histórico excelente. No entanto, ainda há espaço para otimização, nomeadamente no ajuste de parâmetros, na adição de indicadores adicionais e no enriquecimento das condições de fecho, de modo a construir uma estratégia de tendência mais robusta e abrangente. A abordagem é inovadora e merece ser explorada e aplicada mais a fundo.

/*backtest

start: 2023-09-26 00:00:00

end: 2023-10-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @version=5

// Author = TradeAutomation

- 1