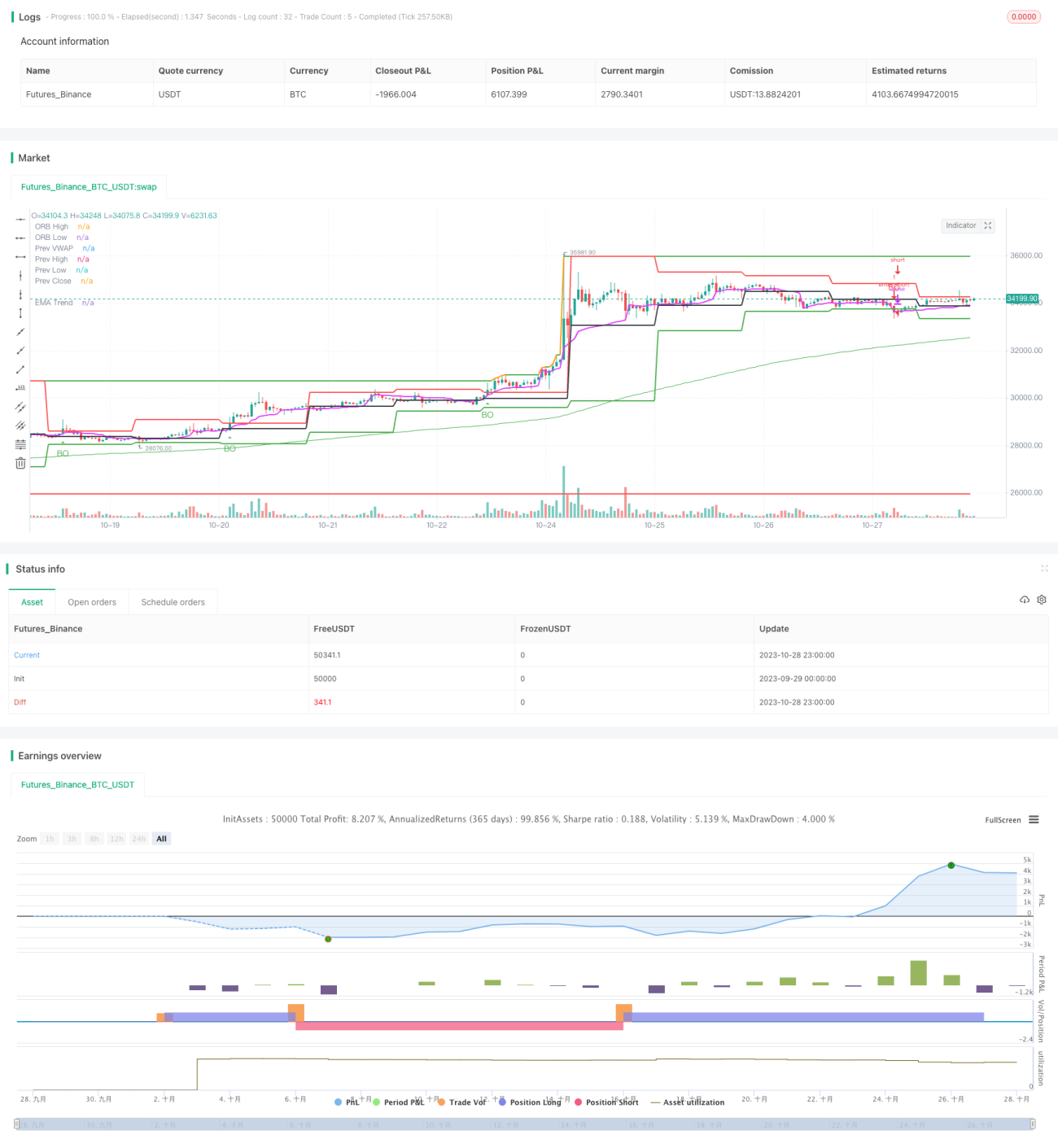

Estratégia de rompimento de média móvel de alto nível

Visão Geral

A ideia principal desta estratégia é utilizar rompimentos de médias móveis de alto período para realizar negociações de tendência. Em um timeframe superior, quando o preço rompe acima ou abaixo da média móvel, pode-se identificar o início de uma tendência, momento em que se pode escolher a direção adequada para seguir.

Princípio da Estratégia

Esta estratégia é desenvolvida em linguagem Pine Script e é dividida principalmente nas seguintes partes:

-

Parâmetros de entrada

- Define o parâmetro de período da média móvel

period, com valor padrão de 200. - Define o parâmetro de timeframe

timeframe, com valor padrão de diário"D".

- Define o parâmetro de período da média móvel

-

Cálculo da média móvel

- Utiliza a função

ta.emapara calcular a Média Móvel Exponencial (Exponential Moving Average).

- Utiliza a função

-

Identificação de rompimento

- Utiliza as funções

ta.crossovereta.crossunderpara verificar se o preço rompeu acima ou abaixo da média móvel.

- Utiliza as funções

-

Plotagem de sinais

- Quando ocorre um rompimento, plota setas para cima ou para baixo nas barras do gráfico.

-

Abertura e fechamento de posições

- Ao ocorrer um rompimento, abre posição na direção correspondente e fecha a posição quando a distância de stop loss duplo é atingida.

Esta estratégia depende principalmente da capacidade de identificação de tendência de uma média móvel de alto período, realizando um simples acompanhamento de tendência por meio de rompimentos. Trata-se de uma estratégia de rompimento relativamente tradicional.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Conceito simples, fácil de entender e dominar.

- Utiliza apenas um indicador de média móvel, com ajuste de parâmetros simplificado.

- As operações de rompimento tendem a formar tendências, evitando negociações frequentes.

- O período superior mostra claramente a tendência principal, sendo menos afetado por oscilações de curto prazo.

- Permite configurar diferentes combinações de timeframes, adaptando-se a diversos ativos.

- Facilita o acompanhamento de múltiplos ativos, dificultando ser pego em várias posições ao mesmo tempo.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- O sinal de rompimento pode ser falso, incapaz de filtrar oscilações de mercado de forma eficaz.

- Não consegue aproveitar oportunidades de curto prazo para lucrar.

- Quando a direção principal estiver errada, as perdas podem ser significativas.

- Se o período da média móvel não coincidir com o período de negociação, pode haver excesso de negociações ou vazamento de sinais.

- Não há stop loss em tempo real, aumentando a possibilidade de perdas maiores.

As soluções para esses riscos incluem: combinar indicadores de tendência, adicionar filtros, encurtar adequadamente o período de retenção da posição, ajustar dinamicamente o nível de stop loss, entre outros.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Adicionar combinações de indicadores de tendência, como MACD, KD, etc., para aumentar a confiabilidade dos rompimentos.

- Incluir filtros como volume de negociação ou Bandas de Bollinger para evitar falsos rompimentos.

- Otimizar a correspondência dos parâmetros de período, de modo que o período de retenção da posição fique mais alinhado com o período da tendência.

- Adicionar uma estratégia de stop loss em tempo real, utilizando stop loss móvel para controlar a perda por operação.

- Considerar a incorporação de técnicas de aprendizado de máquina para otimizar dinamicamente os parâmetros.

- Experimentar combinações de múltiplos ativos para aumentar a estabilidade geral.

Resumo

No geral, esta estratégia é relativamente simples e prática. Ao utilizar rompimentos de média móvel para acompanhar tendências, é fácil de dominar e pode servir como uma das estratégias introdutórias para trading quantitativo. No entanto, apresenta alguns problemas que precisam ser melhorados por meio da combinação de indicadores, otimização de parâmetros, stop loss dinâmico, etc., tornando a estratégia mais estável e eficiente. Possui grande espaço para otimização e escalabilidade.

- 1