Estratégia de negociação baseada em médias móveis EMA

Visão Geral

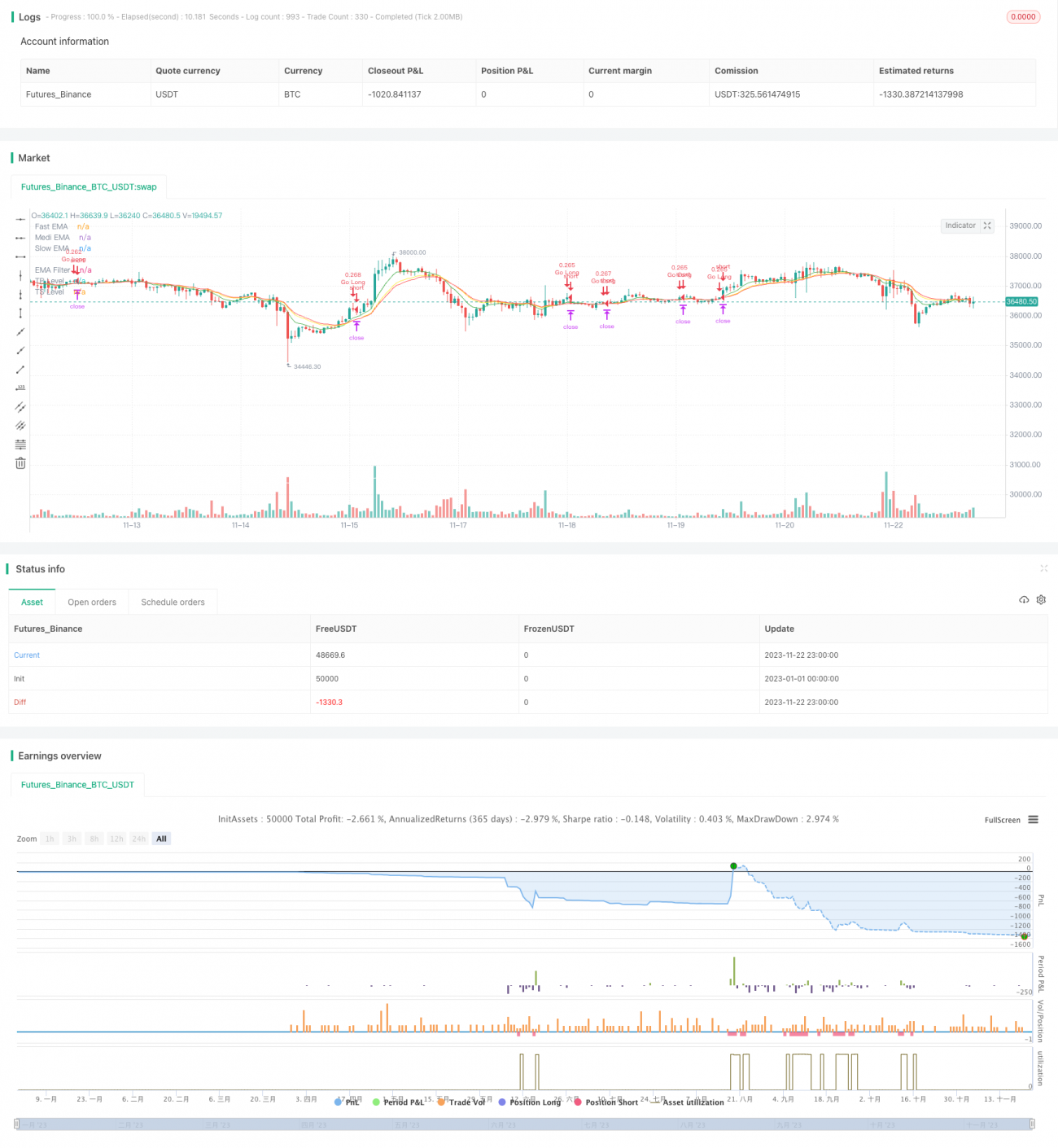

Esta estratégia utiliza 4 médias móveis exponenciais (EMA) de diferentes períodos e gera sinais de negociação com base na sua ordenação, assemelhando-se às luzes de um semáforo (vermelho, amarelo e verde). Por isso, é denominada "Estratégia de Negociação Semáforo". Ela analisa o mercado sob as perspetivas de tendência e reversão, visando aumentar a precisão das decisões de negociação.

Princípio da Estratégia

-

São definidas 3 EMAs: rápida (período 8), média (período 14) e lenta (período 16), acrescentando-se uma EMA de longo prazo (período 100) como filtro.

-

A ordenação das 3 EMAs (rápida, média, lenta) e os seus cruzamentos com o filtro determinam os momentos de compra e venda:

-

Quando a EMA rápida cruza acima da EMA média, ou a EMA média cruza acima da EMA lenta, é gerado um sinal de compra (long).

-

Quando a EMA média cruza abaixo da EMA rápida, é gerado um sinal de fecho da posição comprada.

-

Quando a EMA rápida cruza abaixo da EMA média, ou a EMA média cruza abaixo da EMA lenta, é gerado um sinal de venda (short).

-

Quando a EMA média cruza acima da EMA rápida, é gerado um sinal de fecho da posição vendida.

-

-

A ordenação das 3 EMAs determina a direção e a força da tendência. Combinada com os cruzamentos das EMAs com o filtro, identifica pontos de reversão, integrando o seguimento de tendência com a captura de reversões.

Análise de Vantagens

Esta estratégia combina as vantagens do seguimento de tendência e da negociação de reversão, permitindo uma melhor captura de oportunidades de mercado. As principais vantagens são:

- Utiliza múltiplas EMAs, proporcionando maior poder de decisão e reduzindo sinais falsos.

- Define condições flexíveis para compra e venda, evitando a perda de oportunidades de negociação.

- Utiliza EMAs de curto e longo prazo de forma integrada, oferecendo uma análise abrangente.

- Permite personalizar condições de take profit e stop loss, garantindo um controlo de risco adequado.

Através da otimização de parâmetros, esta estratégia pode adaptar-se a mais ativos, demonstrando uma forte capacidade de rentabilidade e estabilidade nos backtests.

Análise de Risco

Os principais riscos da estratégia são:

- Quando a ordenação das múltiplas EMAs se torna confusa, a dificuldade de análise aumenta, podendo causar hesitação nas negociações.

- Incapacidade de filtrar eficazmente sinais falsos decorrentes de flutuações anómalas do mercado, podendo gerar perdas em mercados muito voláteis.

- Parâmetros mal configurados podem tornar as condições de take profit e stop loss demasiado amplas ou restritivas, levando à perda de lucros ou a perdas excessivas.

Recomenda-se aumentar a estabilidade da estratégia e controlar o risco através da otimização de parâmetros, definição de níveis de stop loss e negociação cautelosa.

Direções de Otimização

As principais direções de otimização da estratégia são:

- Ajustar os períodos das EMAs para se adaptarem a mais ativos.

- Adicionar outros indicadores de filtro, como MACD, Bandas de Bollinger, etc., para melhorar a precisão das decisões.

- Otimizar os rácios de take profit e stop loss para obter o melhor equilíbrio entre risco e retorno.

- Adicionar mecanismos de stop loss adaptativos, como o stop loss baseado em ATR, para controlar ainda mais o risco de queda.

Através de ajustes multifacetados nos parâmetros e da introdução de mecanismos de controlo de risco, é possível melhorar continuamente a estabilidade e a rentabilidade da estratégia.

Resumo

Esta Estratégia de Negociação Semáforo integra o seguimento de tendência e a análise de reversão, utilizando 4 EMAs para gerar sinais de negociação. Através da otimização de parâmetros, adapta-se a mais ativos e demonstra uma forte rentabilidade nos backtests. Com a introdução adicional de controlo de risco e de indicadores diversificados, tem potencial para se tornar uma estratégia de negociação quantitativa estável e eficiente.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1