Estratégia de Índice de Seleção de Commodities com Momentum

Visão Geral

A estratégia do Índice de Seleção de Commodities (Commodity Selection Index, CSI) é uma estratégia de negociação de curto prazo que acompanha o momentum do mercado. Ela identifica commodities com forte momentum para negociação, calculando sua tendência e volatilidade. Essa estratégia foi proposta por Welles Wilder em seu livro "New Concepts in Technical Trading Systems".

Princípio da Estratégia

O indicador central da estratégia é o índice CSI, que considera tanto a tendência quanto a volatilidade da commodity. O cálculo específico é:

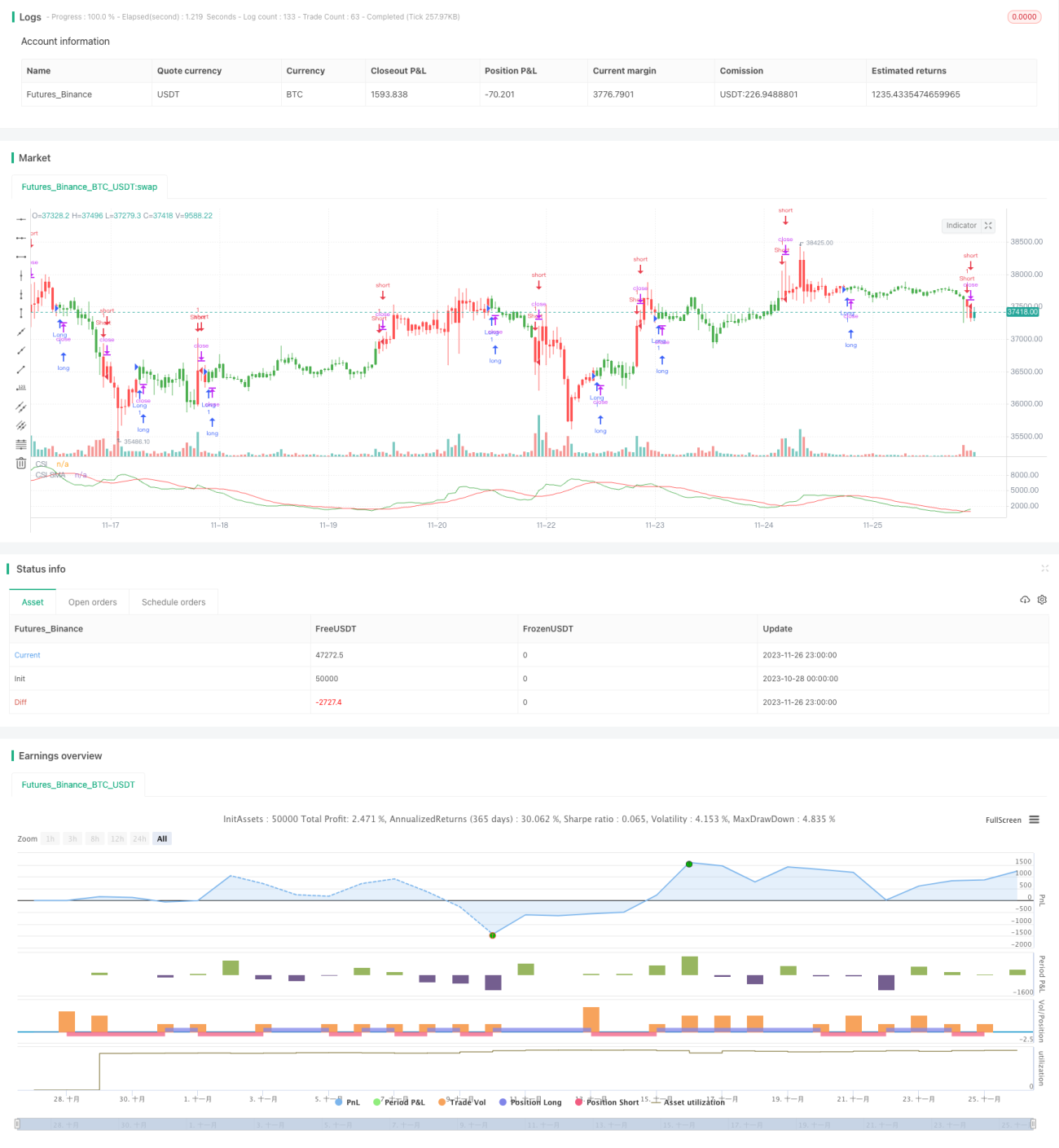

CSI = K × ATR × ((ADX + média móvel de n dias do ADX) / 2)

Onde K é um fator de escala, ATR representa a Amplitude Verdadeira Média (Average True Range), que mede a volatilidade do mercado, e ADX representa o Índice de Movimento Direcional Médio (Average Directional Index), que reflete a tendência do mercado.

Ao calcular o valor do índice CSI para cada commodity e compará-lo com sua média móvel simples de n dias, um sinal de compra é gerado quando o CSI está acima de sua média móvel, e um sinal de venda quando está abaixo.

A estratégia seleciona commodities com alto índice CSI para negociação, pois essas commodities possuem forte tendência e volatilidade, oferecendo maior potencial de lucro no curto prazo.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Captura o momentum do mercado, aproveitando plenamente as características de tendência e volatilidade das commodities.

- Utiliza indicadores duplos, tornando os sinais de negociação mais confiáveis.

- Regras de negociação simples e claras, adequadas para negociação automatizada.

- Projetada especificamente para negociação de curto prazo, permitindo aproveitar rapidamente oportunidades de curto prazo.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- Dependência excessiva de indicadores técnicos, podendo gerar sinais falsos.

- A característica de acompanhar o momentum a torna adequada apenas para operações de curto prazo.

- Volatilidade excessiva pode acionar stop loss, causando perdas na negociação.

- Exige suportar certo nível de alavancagem, resultando em maior risco de capital.

Para controlar os riscos, deve-se definir razoavelmente os níveis de stop loss, controlar o tamanho de cada posição e ajustar adequadamente os parâmetros para se adequar a diferentes condições de mercado.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Testar mais combinações de parâmetros para encontrar os parâmetros ideais.

- Adicionar outros indicadores auxiliares para filtrar sinais.

- Combinar com outras estratégias, como reversão de volatilidade, para formar um portfólio.

- Utilizar aprendizado de máquina para treinar modelos que gerem sinais de negociação mais confiáveis.

Resumo

A estratégia do Índice de Seleção de Commodities, ao capturar commodities com forte tendência e alta volatilidade no mercado, proporciona negociações de curto prazo simples e rápidas. Essa abordagem focada no acompanhamento do momentum gera sinais claros, facilitando a automação. Naturalmente, é necessário controlar os riscos e aprimorar continuamente a estratégia para se adaptar às mudanças nas condições do mercado.

/*backtest

start: 2023-10-28 00:00:00

end: 2023-11-27 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 20/03/2019

// The Commodity Selection Index ("CSI") is a momentum indicator. It was - 1