Estratégia de Stop Loss de Seguimento de Tendência Baseada em TFO e ATR

Visão Geral

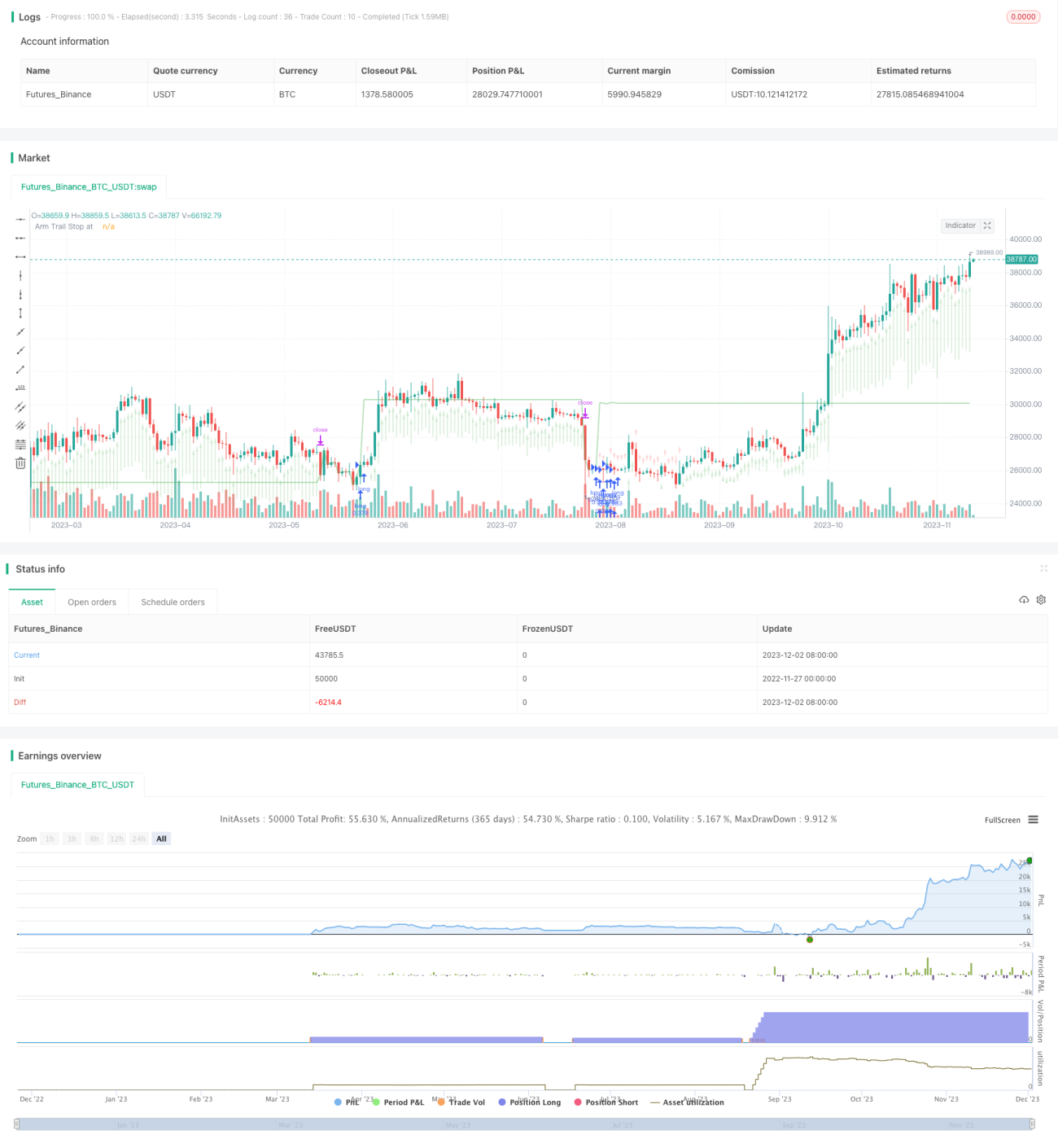

Esta estratégia é uma estratégia de trailing stop baseada no Trend Flex Oscillator (TFO) do Dr. John Ehlers e no Average True Range (ATR). É aplicável a mercados de alta, abrindo uma posição longa quando o preço se inverte após uma condição de sobrevendido. Normalmente, a posição é fechada em alguns dias, a menos que seja capturada por um mercado baixista, caso em que a estratégia mantém a posição. A estratégia ajusta os parâmetros configuráveis através de um backtest simples, mas não se deve confiar totalmente nos resultados do backtest.

Princípio da Estratégia

A estratégia combina os indicadores TFO e ATR, abrindo posições longas quando as condições de compra são atendidas e fechando-as quando as condições de venda são atendidas.

Condição de compra: Quando o TFO está abaixo de um determinado limite (indicando sobrevendido), e o valor do TFO da vela anterior é inferior ao da vela atual (indicando reversão do TFO para cima), e o ATR está acima do limite de volatilidade definido (indicando aumento da volatilidade do mercado). Satisfeitas essas três condições, abre-se uma posição longa.

Condição de venda: Quando o TFO está acima de um determinado limite (indicando sobrecomprado), e o ATR está acima do limite definido, todas as posições longas são fechadas. Além disso, a estratégia também possui um trailing stop: quando o preço cai abaixo do nível de trailing stop definido, todas as posições longas são fechadas. O usuário pode optar por deixar a estratégia fechar com base nos sinais dos indicadores ou apenas pelo preço de stop.

A estratégia pode abrir até 15 posições longas simultaneamente. Seus parâmetros são ajustáveis e aplicáveis a diferentes períodos de tempo.

Vantagens da Estratégia

-

Combina tendência e volatilidade para avaliar a direção do mercado, sendo mais estável. O TFO capta sinais precoces de rompimento da tendência, e o ATR identifica momentos de aumento da volatilidade.

-

Possui parâmetros ajustáveis de compra/venda e stop loss, oferecendo flexibilidade operacional. O usuário pode ajustar os parâmetros conforme o mercado para otimização.

-

Inclui função de stop loss, reduzindo perdas em condições extremas. O stop loss é um elemento crucial no trading quantitativo.

-

Suporta abertura adicional de posições e fechamento parcial, permitindo ampliar lucros através do aumento do tamanho da posição. Adequado para cenários de alta.

Riscos da Estratégia

-

A estratégia opera apenas comprado, não vendido, não sendo capaz de lucrar em mercados em queda. Se encontrar um mercado baixista severo, pode causar perdas enormes.

-

Configuração inadequada de parâmetros pode levar a excesso de negociação ou a perda de compras/vendas. É necessário testar repetidamente para encontrar a melhor combinação de parâmetros.

-

Em condições extremas de mercado, o stop loss pode ser ineficaz, não conseguindo impedir grandes perdas. Este é um problema comum a todas as estratégias de stop loss.

-

O backtest não reflete completamente a negociação real; os resultados reais podem apresentar desvios.

Otimização da Estratégia

-

Pode-se considerar a adição de uma linha de trailing stop na condição de venda, permitindo que a estratégia pare as perdas a tempo, controlando efetivamente o risco de queda.

-

Pode-se expandir o mecanismo de venda a descoberto, abrindo posições curtas quando o TFO reverter para baixo e o ATR for suficientemente grande, tornando a estratégia aplicável a mercados baixistas.

-

Podem ser adicionados mais filtros, como mudanças no volume, para reduzir o impacto de condições anormais do mercado sobre a estratégia.

-

Podem ser testadas configurações de parâmetros e resultados de backtest em diferentes períodos de tempo, buscando a melhor combinação de período e parâmetros.

Conclusão

Esta estratégia integra as vantagens da análise de tendência e do monitoramento da volatilidade, utilizando a combinação dos indicadores TFO e ATR para determinar a direção do mercado. Possui mecanismos como abertura adicional de posições, fechamento parcial e trailing stop, que podem ampliar lucros e controlar riscos, sendo adequada para mercados de alta. Também oferece espaço para otimização, podendo melhorar o desempenho através da adição de mais filtros de indicadores e ajustes de parâmetros. Atende basicamente aos requisitos funcionais de uma estratégia quantitativa, merecendo estudo aprofundado e aplicação.

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1