Estratégia de reversão RSI multifatorial

Visão Geral

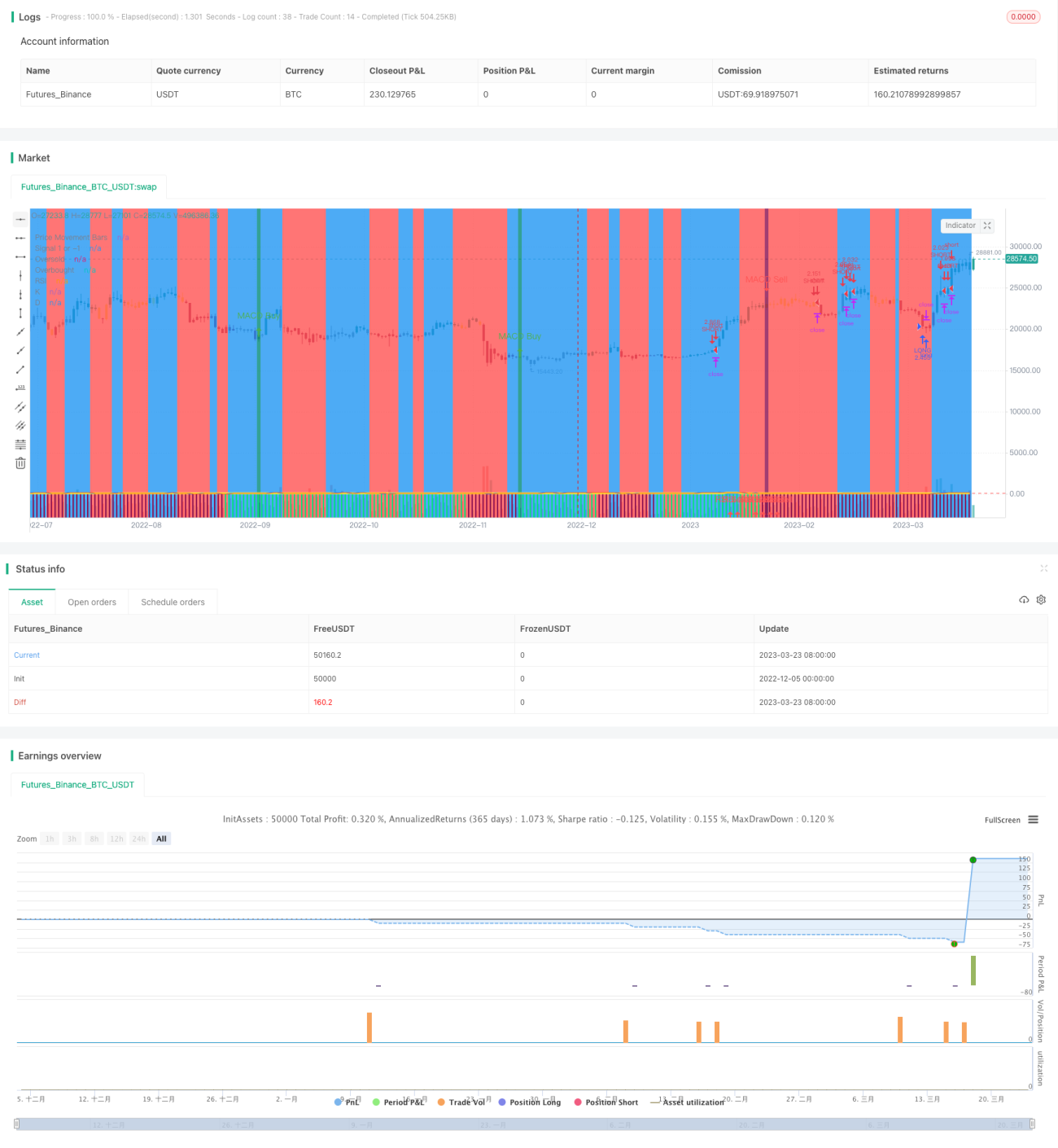

Esta estratégia utiliza o indicador RSI para identificar condições de sobrecompra e sobrevenda, combinando múltiplos fatores auxiliares como MACD, indicador Estocástico, etc., para entrar no mercado. O objetivo é capturar oportunidades de reversão de curto prazo, sendo uma estratégia de reversão.

Princípio da Estratégia

Esta estratégia utiliza principalmente o indicador RSI para determinar se o mercado está em condição de sobrecompra ou sobrevenda. Quando o RSI ultrapassa a linha de sobrecompra definida, indica que o mercado pode estar sobrecomprado, e a estratégia opta por vender (short). Quando o RSI cai abaixo da linha de sobrevenda definida, indica que o mercado pode estar sobrevendido, e a estratégia opta por comprar (long). Dessa forma, lucra capturando oportunidades de curto prazo geradas durante a reversão de um estado extremo para outro.

Além disso, a estratégia introduz múltiplos fatores auxiliares como MACD e Estocástico. Esses fatores auxiliares servem para filtrar possíveis sinais falsos positivos. Somente quando o RSI emite um sinal e os fatores auxiliares também o apoiam é que a estratégia realiza uma ação de negociação real. Essa combinação de múltiplos fatores aumenta a confiabilidade dos sinais, melhorando assim a estabilidade da estratégia.

Análise de Vantagens

A maior vantagem desta estratégia é a alta eficiência de captura, implementando validação multifatorial para melhorar a qualidade do sinal. Especificamente, reflete-se nos seguintes aspectos:

- O próprio indicador RSI tem forte capacidade de identificar regimes de mercado, podendo efetivamente detectar condições de sobrecompra e sobrevenda.

- Com a ajuda de múltiplas ferramentas auxiliares para validação multifatorial, a qualidade do sinal é melhorada, filtrando muitos falsos positivos.

- A estratégia é insensível aos parâmetros, facilitando a otimização.

Riscos e Soluções

A estratégia também enfrenta certos riscos, concentrando-se principalmente em dois aspectos:

- Risco de falha de reversão. O sinal de reversão em si depende de oportunidades de arbitragem estatística, não excluindo a probabilidade de falha de reversão individual. O risco pode ser controlado reduzindo a posição ou definindo stop-loss.

- Risco de perda em tendência de alta. A estratégia como um todo ainda opera contra a tendência principal, e em um mercado de alta é inevitável sofrer algumas perdas. Isso exige que julguemos corretamente a tendência geral e, quando necessário, interrompamos manualmente ambientes desfavoráveis.

Direções de Otimização

A estratégia precisa ser otimizada nos seguintes aspectos:

- Testar diferentes instrumentos financeiros para encontrar a melhor combinação de parâmetros. A estratégia não é sensível aos parâmetros, mas ainda é recomendável encontrar parâmetros ótimos para diferentes instrumentos.

- Adicionar mecanismos de saída adaptativos. Pode-se testar a inclusão de stop-loss dinâmico, saída por tempo, etc., para tornar a estratégia mais adaptável às mudanças do mercado.

- Introduzir algoritmos de aprendizado de máquina. Pode-se tentar fazer o modelo aprender a julgar a probabilidade de sucesso da reversão, aumentando assim a taxa de acerto da estratégia.

Resumo

Em geral, esta estratégia é uma estratégia de reversão de curto prazo. Utiliza a capacidade do indicador RSI de julgar sobrecompra/sobrevenda, combinada com múltiplas ferramentas auxiliares para validação multifatorial, melhorando a qualidade do sinal. A estratégia tem alta eficiência de captura e boa estabilidade. Vale a pena testar e otimizar ainda mais, alcançando eventualmente a lucratividade.

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1