Estratégia de Momentum Simples Baseada em SMA, EMA e Volume

Visão Geral

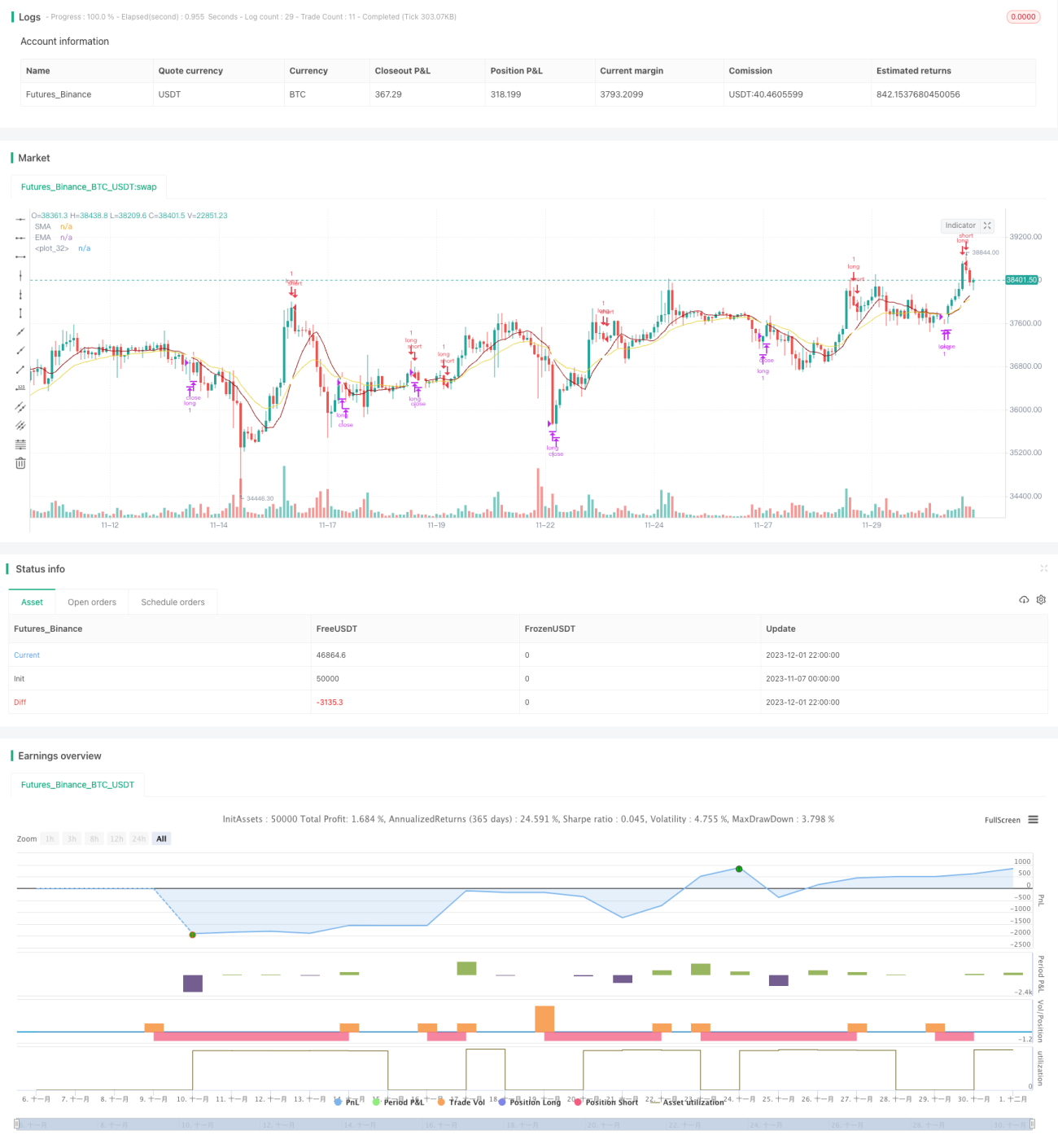

Esta estratégia é uma estratégia de momentum intradiário simples, sem posições vendidas (apenas compradas, nunca vendidas). Ela utiliza os indicadores SMA, EMA e volume para tentar entrar no mercado no momento ideal (ou seja, quando o preço e o momentum sobem simultaneamente). Sua vantagem é a simplicidade de implementação e uma certa capacidade de identificar tendências.

Princípio da Estratégia

A lógica de geração do sinal de entrada (Entry) da estratégia é: quando o indicador SMA estiver acima do indicador EMA e houver uma tendência de alta formada por 3 ou 4 candles consecutivos, e o preço mínimo do candle do meio for superior ao preço de abertura do candle que iniciou a alta, um sinal de entrada é gerado.

A lógica de geração do sinal de saída (Exit) é: quando o SMA cruzar abaixo da EMA, um sinal de saída é gerado.

A estratégia opera apenas no lado comprado, sem posições vendidas. Sua lógica de entrada e saída possui certa capacidade de identificar tendências de alta contínuas.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Lógica simples, fácil de entender e implementar;

- Utiliza indicadores técnicos comuns como SMA, EMA e volume, com parâmetros ajustáveis de forma flexível;

- Possui certa capacidade de identificar tendências de alta contínuas, podendo capturar parte das oportunidades dentro da tendência.

Análise de Riscos

A estratégia também apresenta os seguintes riscos:

- Não consegue identificar mercados em baixa ou laterais, podendo gerar grandes drawdowns;

- Não aproveita oportunidades de venda, não conseguindo realizar hedge em tendências de queda, podendo perder boas oportunidades de lucro;

- O indicador de volume tem baixa eficácia em dados de alta frequência, necessitando de ajustes nos parâmetros;

- É possível utilizar stop loss para controlar o risco.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Adicionar oportunidades de venda, operando nos dois lados (compra e venda) para aproveitar tendências de queda;

- Utilizar indicadores mais avançados, como MACD e RSI, em estratégias combinadas para melhorar a capacidade de julgar tendências;

- Otimizar a lógica de stop loss para reduzir o risco de drawdown;

- Ajustar parâmetros e testar dados de diferentes períodos para encontrar a melhor combinação de parâmetros.

Resumo

No geral, esta estratégia é uma estratégia de rastreamento de tendência muito simples, que utiliza os indicadores SMA, EMA e volume para determinar o momento de entrada. Sua vantagem é a simplicidade e facilidade de implementação, sendo adequada para aprendizado inicial, mas não consegue identificar tendências laterais ou de queda, apresentando certos riscos. Pode ser melhorada com a introdução de posições vendidas, otimização de indicadores e stop loss, entre outros recursos.

- 1