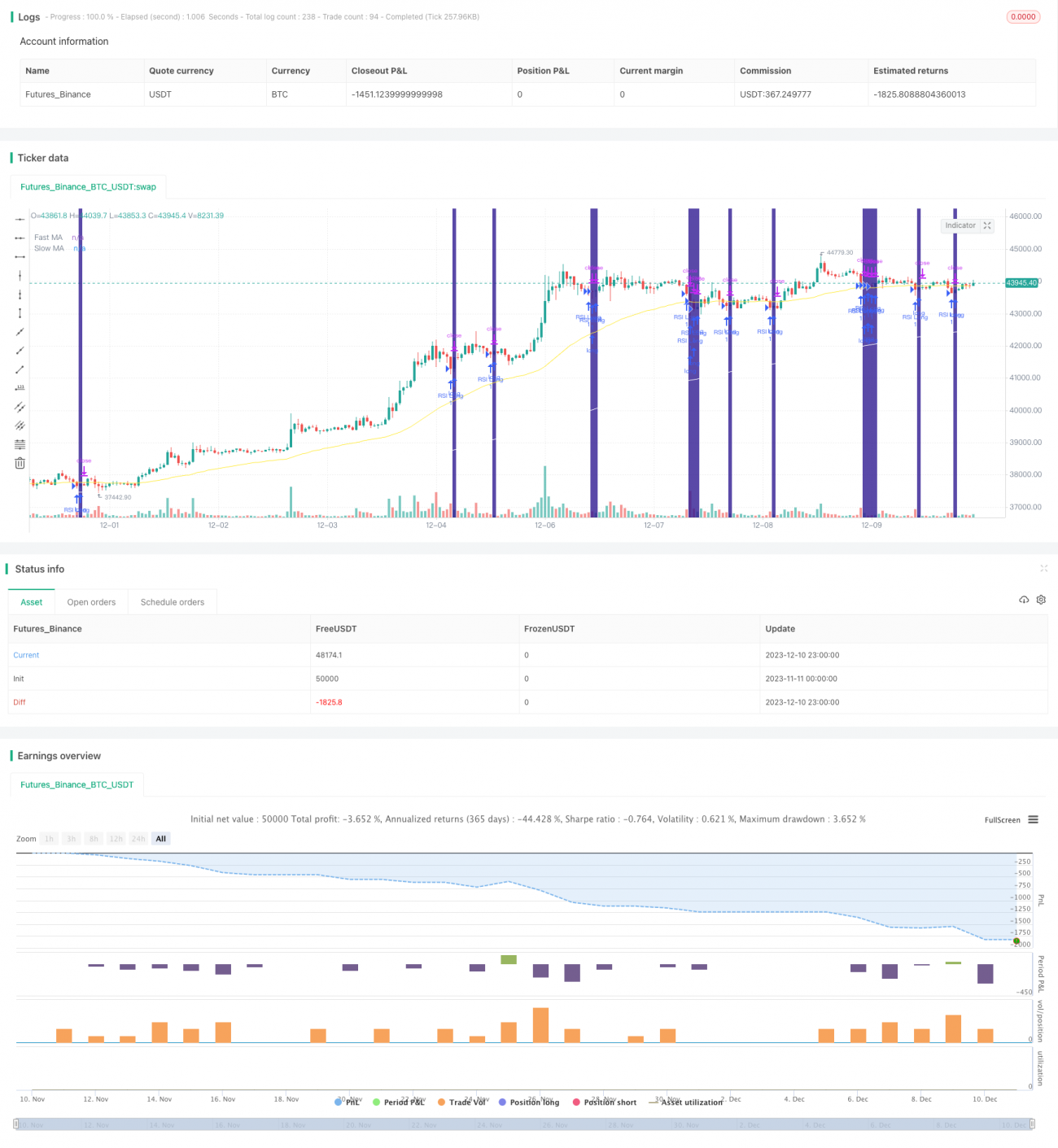

Estratégia de trailing stop baseada no indicador RSI

Visão Geral

O nome desta estratégia é "Estratégia de Stop Loss de Rastreamento de Tendência com Base no Indicador RSI". Esta estratégia utiliza o indicador RSI para julgar situações de sobrecompra e sobrevenda, combinado com indicadores de médias móveis rápidas e lentas (MA) para determinar a direção da tendência e definir as condições de entrada. Ao mesmo tempo, utiliza um mecanismo de stop loss de rastreamento percentual para realizar a saída com stop loss.

Princípio da Estratégia

Esta estratégia determina principalmente o momento de entrada através do indicador RSI e do indicador MA. O parâmetro do indicador RSI é definido como 2 períodos para julgar situações de sobrecompra e sobrevenda. As MAs rápida e lenta são configuradas com 50 períodos e 200 períodos, respectivamente, para determinar a direção da tendência. A lógica específica de entrada é:

Entrada longa: Quando a MA rápida cruza acima da MA lenta, e o preço está acima da MA lenta, e ao mesmo tempo o RSI está abaixo da zona de sobrevenda (padrão 10%), realizar compra.

Entrada curta: Quando a MA rápida cruza abaixo da MA lenta, e o preço está abaixo da MA lenta, e ao mesmo tempo o RSI está acima da zona de sobrecompra (padrão 90%), realizar venda.

Além disso, a estratégia também define um filtro de volatilidade opcional. Este filtro calcula a diferença nas inclinações das MAs rápida e lenta, e só abre posição quando a diferença excede um limite definido. O objetivo é evitar abrir posições durante períodos de oscilação de preços sem uma direção clara.

Na saída, a estratégia adota um método de stop loss de rastreamento percentual. Com base no percentual de stop loss inserido, combinado com a diferença de preço por tick, calcula-se o nível de stop loss, permitindo um ajuste dinâmico do stop loss.

Análise de Vantagens

Esta estratégia possui principalmente as seguintes vantagens:

- O parâmetro do indicador RSI é definido como 2 períodos, capturando rapidamente situações de sobrecompra e sobrevenda e identificando oportunidades de reversão.

- As MAs rápida e lenta podem identificar efetivamente a direção da tendência e os pontos de inflexão.

- A combinação dos indicadores duplos RSI e MA pode evitar falsos rompimentos.

- A configuração do filtro de volatilidade pode filtrar períodos de mercado sem direção definida durante a oscilação.

- O uso de stop loss de rastreamento percentual permite ajustar a amplitude do stop loss de acordo com a volatilidade do mercado, controlando efetivamente o risco.

Análise de Riscos

Esta estratégia também apresenta alguns riscos, principalmente refletidos em:

- Os indicadores RSI e MA têm certo atraso, podendo perder algumas oportunidades de reversão.

- O stop loss percentual é facilmente acionado em quedas com volume reduzido.

- Não consegue lidar eficazmente com produtos de alta volatilidade durante o período noturno e pré-mercado.

Em relação aos riscos acima, as seguintes otimizações podem ser realizadas:

- Ajustar o parâmetro RSI para 1 período para reduzir o atraso.

- Ajustar os parâmetros do período MA de acordo com as características de diferentes produtos.

- Ajustar o nível do stop loss percentual, equilibrando o stop loss e a tolerância à oscilação.

Direções de Otimização da Estratégia

Esta estratégia pode ser otimizada nos seguintes aspectos:

- Adicionar outros indicadores de julgamento, como o indicador de volume, para evitar falsos rompimentos.

- Adicionar julgamento de modelo de aprendizado de máquina, utilizando previsões do modelo para auxiliar na tomada de decisão.

- Otimizar o número de reinvestimentos e o gerenciamento de posição para melhorar ainda mais a taxa de retorno da estratégia.

- Definir mecanismos de filtragem de volatilidade para o período noturno e pré-mercado. Decidir se participará das negociações do próximo pregão de acordo com a amplitude da volatilidade.

Conclusão

No geral, esta estratégia é uma estratégia de rastreamento de tendência relativamente estável. Ela combina os indicadores duplos RSI e MA para julgamento, garantindo certa estabilidade e também capturando oportunidades de reversão de tendência relativamente claras. Ao mesmo tempo, a configuração do filtro de volatilidade pode evitar alguns riscos, e o método de stop loss percentual também pode controlar efetivamente as perdas individuais. Esta estratégia pode ser usada como uma estratégia universal para múltiplos produtos, ou pode ter seus parâmetros ajustados e modelos otimizados para produtos específicos, obtendo assim melhores resultados de estratégia.

- 1