Estratégia de Pullback de Momentum

Visão Geral

A Estratégia de Pullback de Momentum (Momentum Pullback Strategy) é uma estratégia de posições longas e curtas que identifica valores extremos do RSI como sinais de momentum. Diferente da maioria das estratégias baseadas em RSI, esta estratégia busca o primeiro pullback na direção da leitura extrema do RSI para realizar a entrada.

Ela realiza operações de compra/venda no ponto de primeiro pullback da EMA de 5 períodos (mínimo)/EMA de 5 períodos (máximo), e encerra a posição no ponto mais alto/mais baixo das últimas 12 barras rolantes. Esse mecanismo de ponto mais alto/baixo rolante significa que, se o preço entrar em uma consolidação prolongada, o alvo de lucro diminui a cada nova barra. As melhores negociações geralmente são concluídas dentro de 2 a 6 barras.

A distância sugerida para o stop loss é X vezes o ATR a partir do preço de entrada (ajustável nos parâmetros de entrada do usuário).

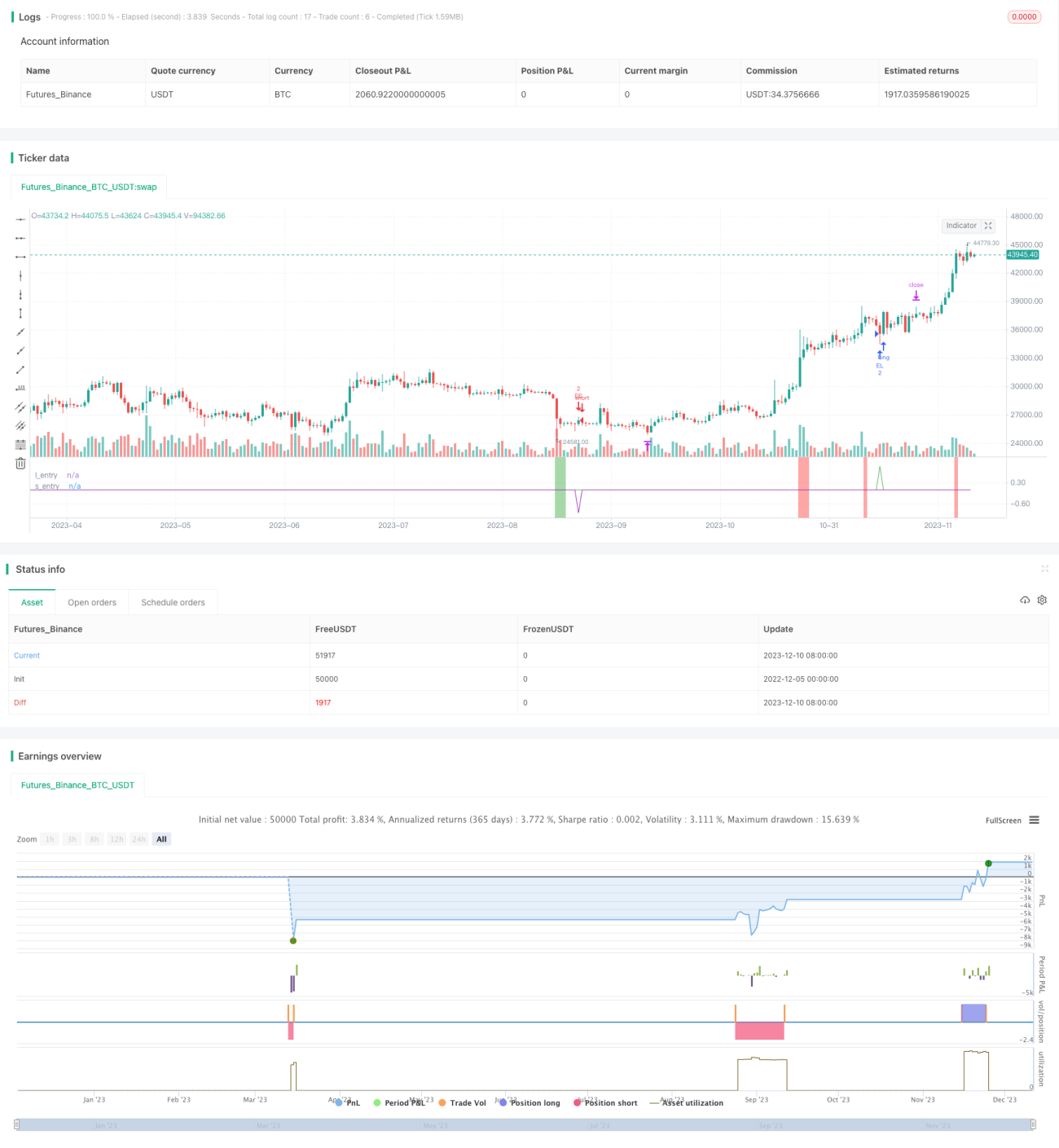

A estratégia é robusta em diferentes períodos e mercados, com uma taxa de acerto entre 60% e 70% e negociações lucrativas de tamanho considerável. É necessário evitar que sinais sejam gerados durante a volatilidade causada por notícias econômicas importantes.

Princípio da Estratégia

-

Calcular o RSI de 6 períodos, buscando pontos extremos acima de 90 (sobrecomprado) e abaixo de 10 (sobrevendido).

-

Quando o RSI estiver em sobrecompra, realizar a entrada comprada no primeiro pullback dentro de 6 barras até a EMA de 5 períodos (linha mínima).

-

Quando o RSI estiver em sobrevenda, realizar a entrada vendida no primeiro pullback dentro de 6 barras até a EMA de 5 períodos (linha máxima).

-

A estratégia de saída é um take profit móvel: para posições compradas, o primeiro alvo de saída é o ponto mais alto das últimas 12 barras; à medida que novas barras surgem, o alvo é atualizado para o novo ponto mais alto das últimas 12 barras, proporcionando uma saída rolante. Para posições vendidas, o oposto é aplicado: o stop loss é o ponto mais baixo rolante das últimas 12 barras.

-

A distância do stop loss é o preço de entrada multiplicado por X vezes o ATR, customizável.

Análise de Vantagens

A estratégia combina extremos do RSI como sinal de momentum com entrada por pullback, capturando pontos potenciais de reversão em tendências, com alta taxa de acerto.

O mecanismo de take profit móvel permite travar parte dos lucros com base no movimento real do preço, reduzindo o drawdown.

O stop loss baseado em ATR controla efetivamente a perda por operação.

Robustez elevada, aplicável a diferentes mercados e combinações de parâmetros, facilitando a replicação em tempo real.

Análise de Riscos

Se o valor do ATR for muito grande, a distância do stop loss pode ser excessiva, ampliando a perda por operação.

Se ocorrer uma consolidação de longo prazo, o mecanismo de take profit móvel reduzirá o espaço de lucro.

Se o pullback for muito profundo e ultrapassar 6 barras, a oportunidade de entrada será perdida.

Em eventos econômicos importantes, a negociação pode sofrer slippage ou falsos rompimentos.

Direções de Otimização

É possível testar a redução do número de barras para entrada, por exemplo, de 6 para 4 barras, aumentando a taxa de sucesso na entrada.

É possível testar o aumento do múltiplo do ATR para controlar ainda mais o stop loss por operação.

Pode-se combinar indicadores de volume para evitar perdas decorrentes de divergências em consolidações.

Pode-se entrar após o pullback romper o eixo de 60 minutos, filtrando parte do ruído.

Resumo

A Estratégia de Pullback de Momentum é, em geral, uma estratégia prática de curto prazo para capturar movimentos. Ela combina tendência, reversão e stop loss, sendo fácil de operar em tempo real e ainda possuindo certo alfa. Por meio de ajustes de parâmetros e combinação com outros indicadores, é possível aumentar ainda mais a estabilidade. No geral, trata-se de uma grande vantagem para o trading quantitativo, valendo a pena ser estudada e aplicada.

- 1