Estratégia de Stop Loss de Super Trend Following

Visão Geral

Esta estratégia baseia-se no indicador SuperTrend e num stop loss móvel para abrir e fechar posições. Utiliza 4 alertas para abertura e fecho de posições e adota a estratégia SuperTrend. Foi concebida especificamente para robôs, com funcionalidade de stop loss móvel.

Princípio da Estratégia

A estratégia utiliza o indicador ATR para calcular as bandas superior e inferior. Quando o preço de fecho ultrapassa a banda superior, gera-se um sinal de compra; quando ultrapassa a banda inferior, gera-se um sinal de venda. A estratégia também emprega a linha SuperTrend para determinar a direção da tendência. Quando a linha SuperTrend cruza para cima, indica o início de um mercado em alta; quando cruza para baixo, indica o início de um mercado em baixa. Ao gerar um sinal, a estratégia abre uma posição e define um preço de stop loss inicial. Posteriormente, ajusta o stop loss de forma dinâmica, acompanhando a variação do preço, para bloquear lucros, concretizando o efeito de stop loss móvel.

Análise de Vantagens

A estratégia combina as vantagens do indicador SuperTrend na determinação da direção da tendência e do ATR na definição do stop loss, filtrando eficazmente falsos rompimentos. O stop loss móvel permite bloquear lucros e reduzir o drawdown. Além disso, por ter sido projetada para robôs, pode ser automatizada.

Análise de Riscos

O indicador SuperTrend pode gerar muitos sinais falsos. Quando o ajuste do preço de stop loss é demasiado amplo, aumenta a probabilidade de o stop ser atingido. Além disso, a negociação por robô enfrenta riscos técnicos como falhas de servidor e interrupções de rede.

Para reduzir a probabilidade de sinais falsos, podem ajustar-se os parâmetros do ATR ou adicionar outros indicadores como filtro. Ao ajustar a amplitude do stop loss móvel, é necessário equilibrar lucro e risco. Também é recomendável ter servidores e redes de reserva para prevenir riscos de falha técnica.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspetos:

-

Adicionar indicadores ou condições para filtrar sinais de entrada, evitando sinais falsos. Por exemplo, adicionar o indicador MACD.

-

Testar diferentes combinações de parâmetros ATR para encontrar os melhores.

-

Otimizar a amplitude do stop loss móvel para encontrar o ponto de equilíbrio ideal.

-

Adicionar mais níveis de stop loss, permitindo stops parciais.

-

Implementar uma arquitetura de servidores principal e de reserva, alternando rapidamente em caso de falha do servidor principal.

Resumo

Esta estratégia integra as vantagens do indicador SuperTrend e do stop loss móvel, permitindo a abertura automática de posições e stops. Na prática, combinada com as medidas de melhoria nas direções de otimização, pode tornar-se uma estratégia de trading quantitativo muito útil.

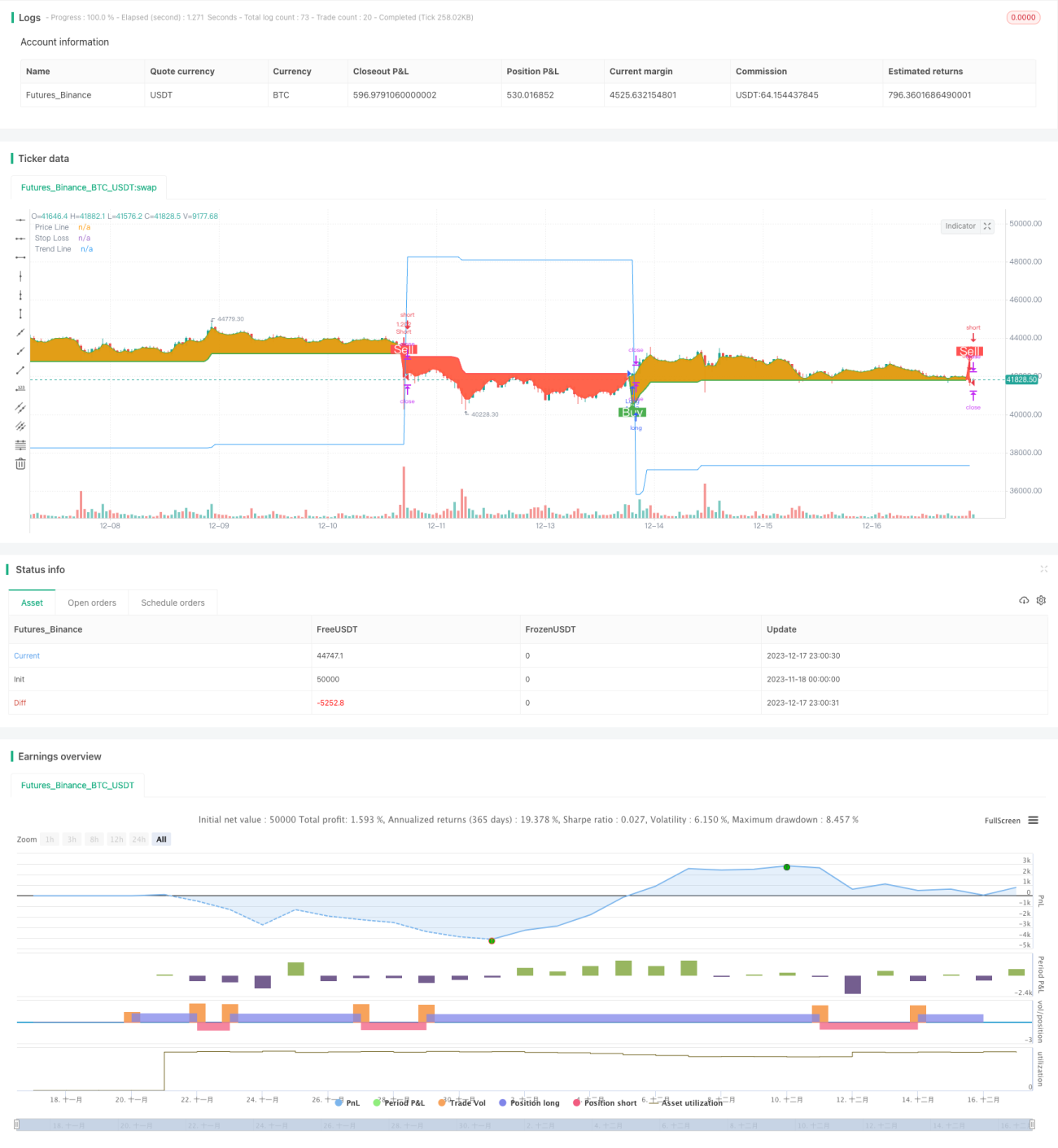

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © arminomid1375

//@version=5

strategy('Mizar_BOT_super trend', overlay=true, default_qty_value=100, currency=currency.USD, default_qty_type=strategy.percent_of_equity, initial_capital=100, max_bars_back=4000)- 1