Estratégia de Reversão de Média Móvel com Acompanhamento de Momentum

Visão Geral

Esta estratégia utiliza múltiplos indicadores como médias móveis, Bandas de Bollinger, RSI e Estocástico, combinados com análise de múltiplos prazos, para projetar uma estratégia que aproveita indicadores de momentum para identificar reversões de mercado.

Princípio da Estratégia

A lógica central da estratégia é monitorar o cruzamento entre médias móveis de curto e longo prazo para identificar fundos e topos, com o apoio de indicadores de momentum como RSI e Estocástico em seus valores extremos para detectar condições de sobrecompra e sobrevenda.

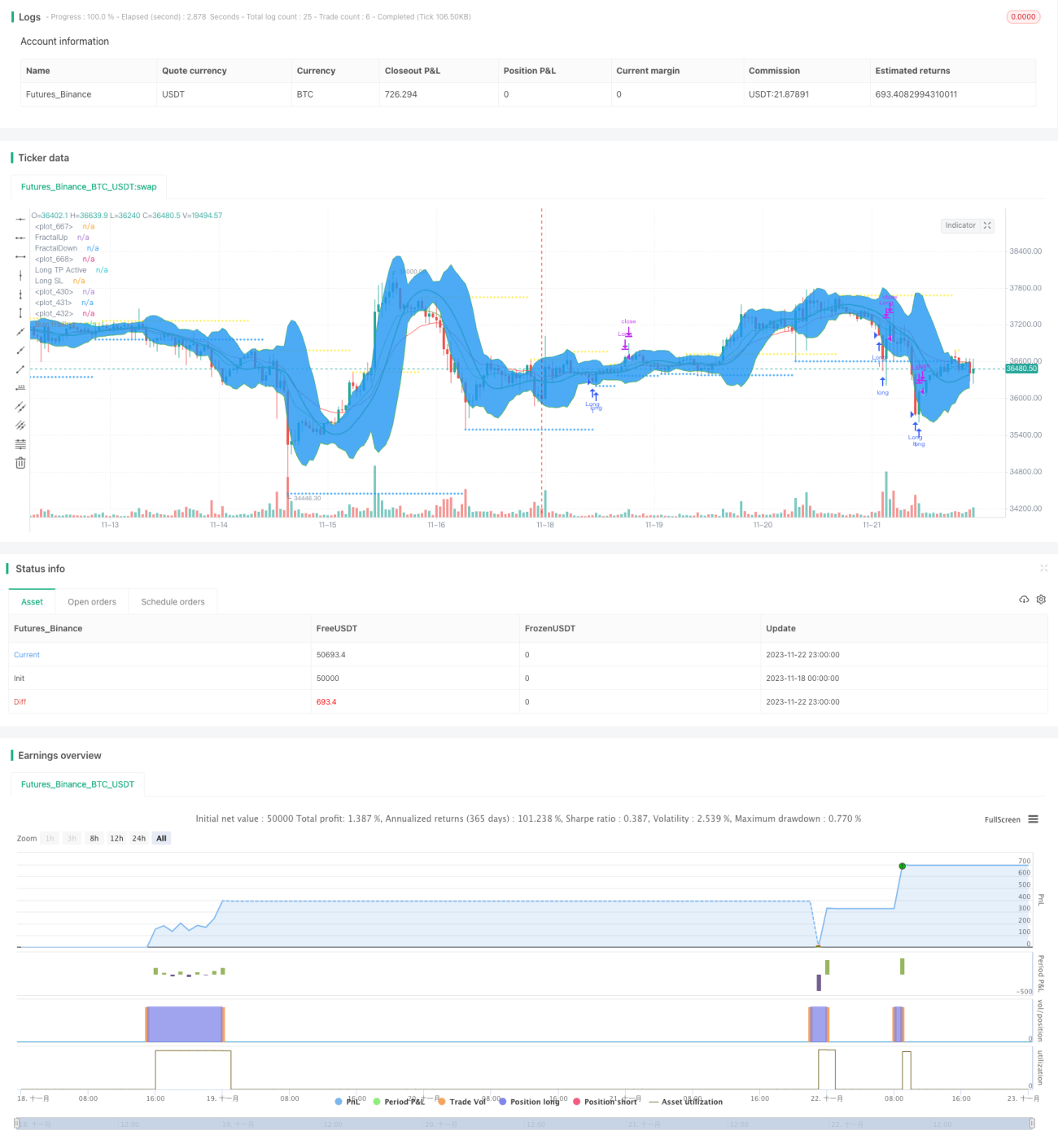

Especificamente, são traçadas duas médias móveis com parâmetros diferentes: uma de curto prazo para avaliar a tendência atual e outra de longo prazo para identificar a tendência principal. Quando a média móvel de curto prazo cruza para cima a média de longo prazo, considera-se uma reversão de alta, gerando sinal de compra; quando cruza para baixo, gera sinal de venda.

Além disso, a estratégia verifica se o RSI entrou em zona de sobrevenda e se o Estocástico (linha K) também está em sobrevenda, para identificar características de fundo. Para topos, utiliza-se a lógica inversa desses indicadores.

Na saída, a estratégia utiliza stop de lucro, stop loss e trailing stop para gerenciar as posições.

Análise de Vantagens

Esta é uma estratégia que combina acompanhamento de tendência e identificação de reversões, integrando indicadores de momentum de forma prática. Possui as seguintes vantagens:

-

O sistema de cruzamento de médias móveis é um método simples e eficaz para identificar reversões. A estratégia de dupla média é fácil de operar e apresenta bons resultados históricos.

-

A combinação com indicadores como RSI ajuda a confirmar a confiabilidade dos sinais de reversão, evitando sinais enganosos fora de regiões de fundo ou topo.

-

Os mecanismos de stop de lucro, stop loss e trailing stop ajudam a travar lucros e controlar riscos.

Análise de Riscos

Embora a estratégia tenha muitos pontos positivos, existem alguns riscos a serem considerados:

-

A estratégia de dupla média pode sofrer em mercados laterais. Se o mercado se consolidar por muito tempo, as posições serão abertas e fechadas com frequência.

-

Indicadores como RSI não conseguem evitar completamente sinais falsos. Por exemplo, uma rápida ultrapassagem do topo anterior pode impedir que o RSI entre em zona de sobrecompra.

-

Stops muito largos aumentam o risco de perdas. A amplitude do stop loss precisa ser ajustada conforme o ativo específico.

Direções de Otimização

A estratégia ainda possui vários pontos que podem ser otimizados:

-

Testar diferentes tipos de médias móveis para encontrar a mais adequada.

-

Adicionar mais indicadores auxiliares, como MACD, KD e Bandas de Bollinger, para enriquecer a lógica.

-

Utilizar aprendizado de máquina para otimizar automaticamente os parâmetros de gerenciamento de posições, tornando os stops mais inteligentes.

-

Os parâmetros podem ser otimizados individualmente para cada ativo, a fim de se adaptar às suas características.

Resumo

Em resumo, a Estratégia de Reversão com Médias Móveis e Momentum é uma estratégia quantitativa simples e prática. Ela utiliza o sistema de médias móveis para identificar pontos de reversão do mercado, apoia-se em indicadores de momentum para confirmar a confiabilidade dos sinais e emprega gerenciamento inteligente de posições para travar lucros e controlar riscos. A estratégia é fácil de entender e implementar, merece ser praticada e otimizada, sendo um bom ponto de partida para traders que desejam aprender trading quantitativo.

/*backtest

start: 2023-11-18 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("APEX - Tester - Buy/Sell Strategies - Basic - BACKTESTER", overlay = true)

//study("APEX - Tester - Buy/Sell Strategies - Basic ", overlay = true)

source_main = close- 1