Estratégia de rastreamento de reversão quantitativa de dois fatores

Visão Geral

Esta estratégia combina dois fatores: a reversão do padrão 123 e o Awesome Oscillator, implementando uma negociação de reversão quantitativa de duplo fator. A ideia básica é, ao julgar a reversão do mercado, combinar os sinais de alta/baixa do Awesome Oscillator para obter uma entrada mais precisa.

A estratégia é adequada principalmente para negociações de reversão de curto e médio prazo. Através da confirmação de múltiplos fatores, ela pode filtrar efetivamente falsas reversões e melhorar a qualidade dos sinais.

Princípio da Estratégia

-

Reversão do Padrão 123

Julga a relação entre os preços de fechamento dos dois dias anteriores e o preço de fechamento atual, formando um padrão "alta-alta-baixa" ou "baixa-baixa-alta", indicando um possível sinal de reversão.

Ao mesmo tempo, exige que o indicador Stochastic esteja na zona de sobrecompra/sobrevenda, confirmando ainda mais o sinal de reversão e filtrando falsas reversões.

-

Awesome Oscillator

O Awesome Oscillator é um indicador de momentum construído a partir da diferença entre médias móveis de curto e médio prazo. Quando a linha rápida cruza a linha lenta de cima para baixo, é um ponto de venda; quando cruza de baixo para cima, é um ponto de compra.

Esta estratégia utiliza o sinal de alta/baixa deste indicador para determinar os pontos de entrada e saída.

-

Confirmação de Duplo Fator

Através da dupla confirmação da reversão do padrão 123 e do Awesome Oscillator, é possível filtrar efetivamente falsas reversões e melhorar a precisão do timing de entrada.

Vantagens da Estratégia

-

O uso de dois fatores para determinar pontos de reversão pode filtrar efetivamente sinais falsos de reversão.

-

O Awesome Oscillator, como indicador de momentum, pode melhorar a precisão do timing de entrada.

-

A inclusão do indicador Stochastic evita o risco de comprar no topo e vender no fundo.

-

A estratégia de reversão em si possui uma alta taxa de acerto e uma boa relação risco-retorno.

Riscos da Estratégia

-

O risco de falha na reversão ainda existe. O uso de dois fatores reduz a probabilidade, mas não elimina completamente esse risco.

-

Risco de sobre-otimização. Os parâmetros dos indicadores precisam ser testados e ajustados para diferentes mercados, a fim de evitar sobre-otimização.

-

Risco de ir contra a tendência. Em mercados com forte tendência predominante, as estratégias de reversão tendem a gerar perdas contrárias. Pode-se definir um stop loss para controlar o risco.

Direções de Otimização da Estratégia

-

Testar e otimizar combinações de parâmetros dos indicadores para aumentar a robustez.

-

Adicionar estratégias de stop loss para controlar perdas por operação.

-

Combinar seleção de setores e segmentos para evitar escolha inadequada de ações.

-

Otimizar o período de manutenção da posição para evitar um rastreamento excessivamente cego.

-

Testar diferentes sistemas de médias móveis como condições auxiliares.

Resumo

Em resumo, esta estratégia de rastreamento de reversão quantitativa de duplo fator, com base em uma probabilidade de lucro e relação risco-retorno razoáveis, utiliza o Awesome Oscillator como ferramenta auxiliar de timing de entrada e o indicador Stochastic para evitar comprar no topo. Ela consegue controlar efetivamente os riscos das negociações de reversão, possuindo forte praticabilidade.

No entanto, os riscos inerentes à própria estratégia de reversão não podem ser ignorados. Ainda é necessário otimizar os parâmetros dos indicadores e definir condições de stop loss para controlar os riscos. Se aplicada corretamente, esta estratégia pode proporcionar aos investidores retornos excedentes estáveis.

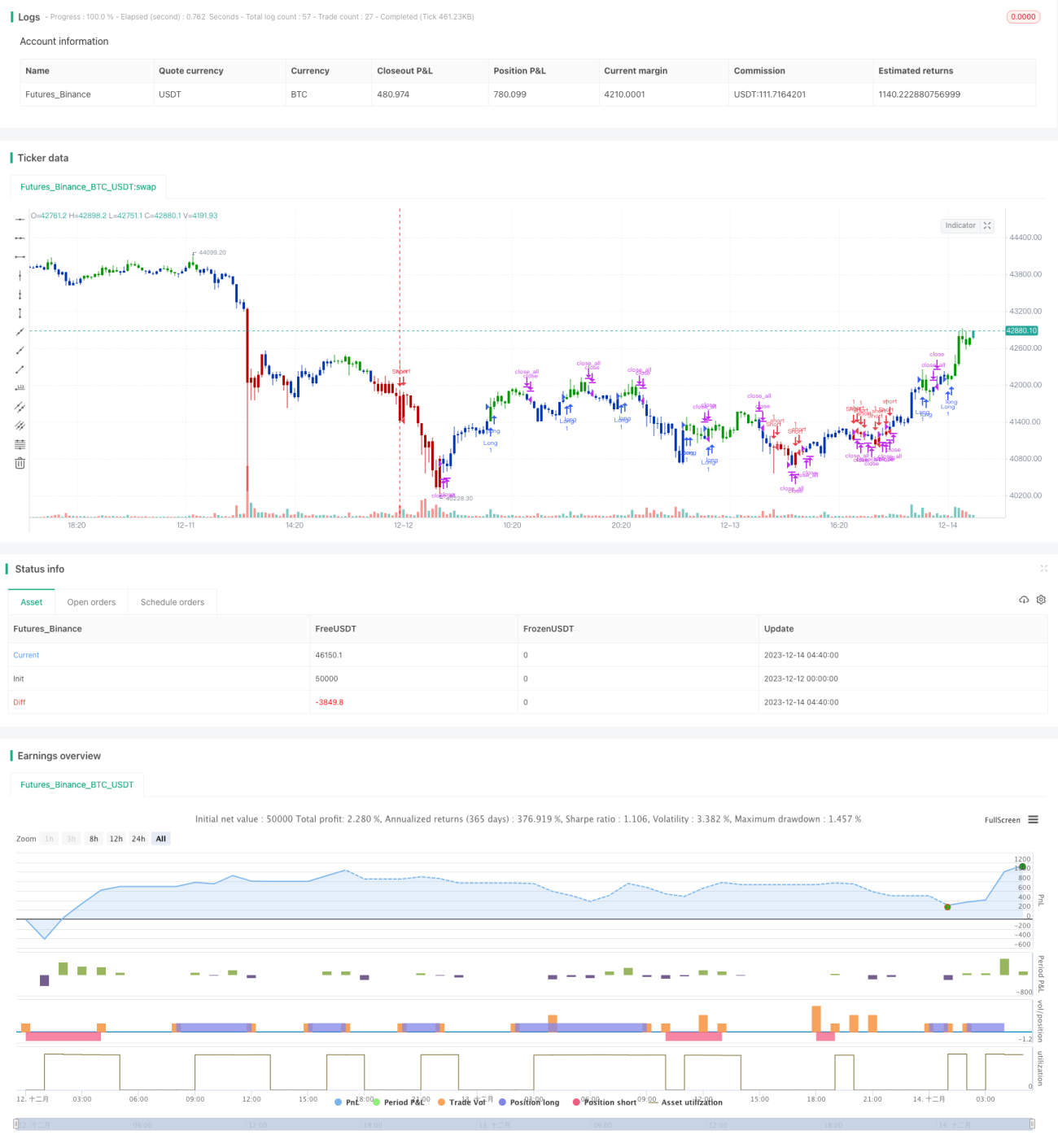

/*backtest

start: 2023-12-12 00:00:00

end: 2023-12-14 05:00:00

period: 20m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 12/08/2021

// This is combo strategies for get a cumulative signal. - 1