Estratégia de robô escalável personalizada com MACD MFI HTF não repintado

Visão Geral

Esta estratégia é altamente personalizável, combinando os indicadores MACD (sem repintura) e MFI, sendo adequada para robôs de negociação algorítmica. Ela integra indicadores de tendência e momentum, utilizando múltiplos filtros para gerar sinais de negociação.

Princípio da Estratégia

A estratégia utiliza o indicador MACD para identificar a direção da tendência do mercado. O MACD é um indicador de momentum do tipo seguidor de tendência, obtido subtraindo a média móvel lenta da média móvel rápida, gerando o histograma MACD, e então usando a média móvel exponencial do MACD como linha de sinal. Quando a linha rápida cruza acima da linha lenta, é um sinal de compra; quando cruza abaixo, é um sinal de venda.

Além disso, a estratégia também utiliza o indicador MFI para avaliar as condições de sobrecompra e sobrevenda do mercado. O MFI combina informações de preço e volume, variando entre 0 e 100. Valores abaixo de 20 indicam região de sobrevenda, e acima de 80, região de sobrecompra.

Para filtrar sinais falsos, a estratégia incorpora filtros de tendência e RSI. Quando o preço está em uma tendência de alta e o RSI está abaixo do limite definido, é gerado um sinal de compra.

Vantagens da Estratégia

- Combina múltiplos indicadores para avaliar de forma abrangente as condições do mercado, aumentando a taxa de acerto.

- Incorpora mecanismos de filtro para evitar sinais falsos e reduzir negociações desnecessárias.

- Diversos parâmetros e filtros são configuráveis, adaptando-se a diferentes ativos e preferências de negociação.

- Pode ser utilizada tanto para negociação manual quanto conectada a robôs algorítmicos para negociação programática.

Riscos e Soluções da Estratégia

-

Parâmetros mal ajustados podem gerar sinais falsos.

-

É possível testar diferentes parâmetros para selecionar a combinação ideal.

-

Os parâmetros não são universais entre diferentes ativos, exigindo testes e otimizações individuais.

-

A frequência de negociação pode ser excessiva, aumentando custos e riscos de slippage.

-

É possível ajustar os filtros para reduzir a frequência de negociação.

-

Durante a negociação real, é necessário controlar os custos.

Direções de Otimização da Estratégia

- Testar períodos de dados mais longos para avaliar a estabilidade dos parâmetros.

- Experimentar diferentes combinações de parâmetros dos indicadores.

- Otimizar os pesos dos indicadores para melhorar a estabilidade da estratégia.

- Adicionar mais filtros para reduzir negociações desnecessárias.

Resumo

Esta estratégia é altamente personalizável e do tipo seguidor de tendência, combinando indicadores de tendência e momentum para avaliar as condições do mercado, utilizando eficazmente mecanismos de filtro para controlar riscos. Ela pode ser usada tanto para negociação manual quanto conectada a robôs algorítmicos para alcançar um alto grau de automação, constituindo um sistema de estratégia digno de acompanhamento e otimização a longo prazo.

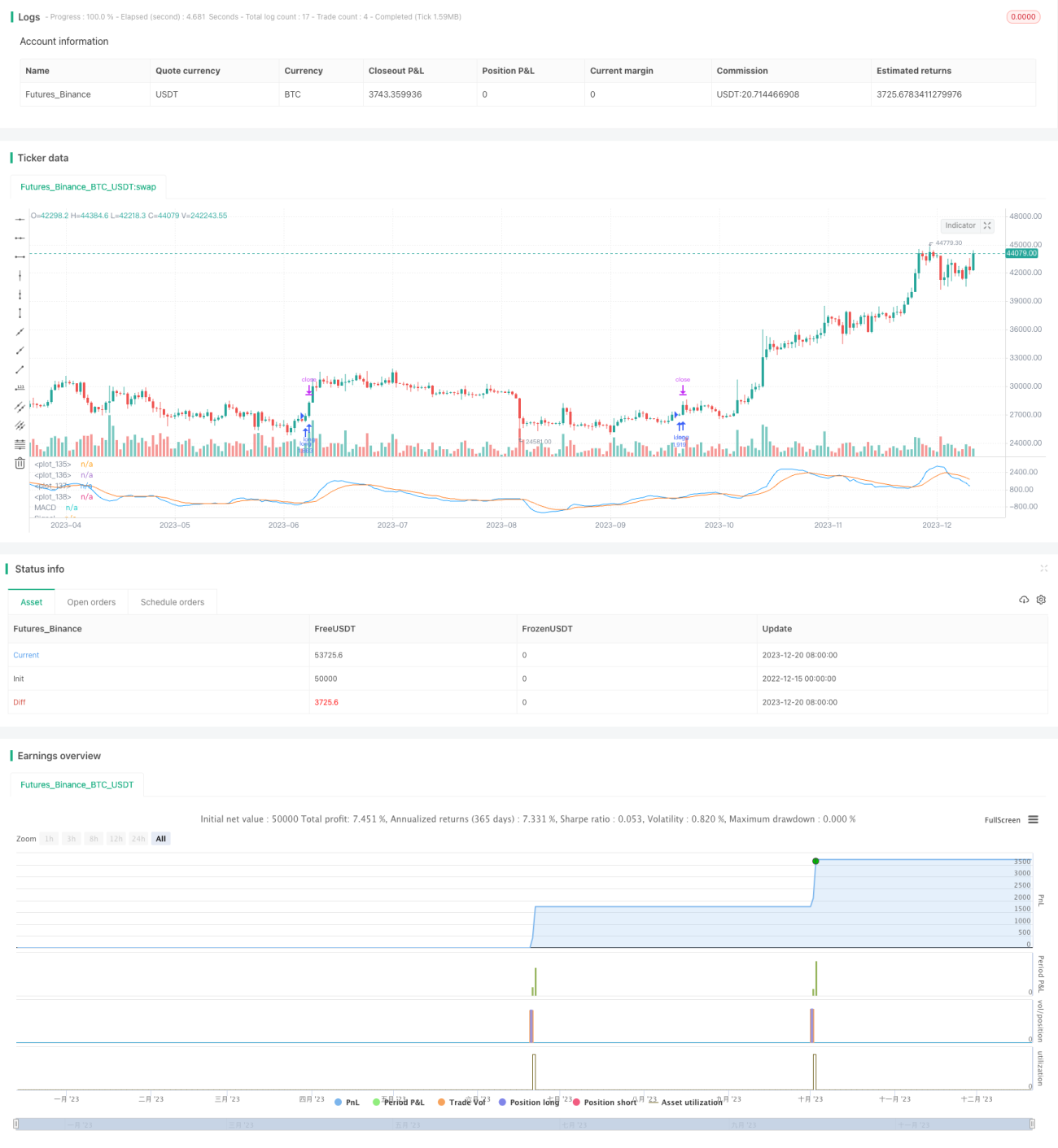

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1