Estratégia de negociação de Bitcoin baseada em indicadores quantitativos

Visão Geral

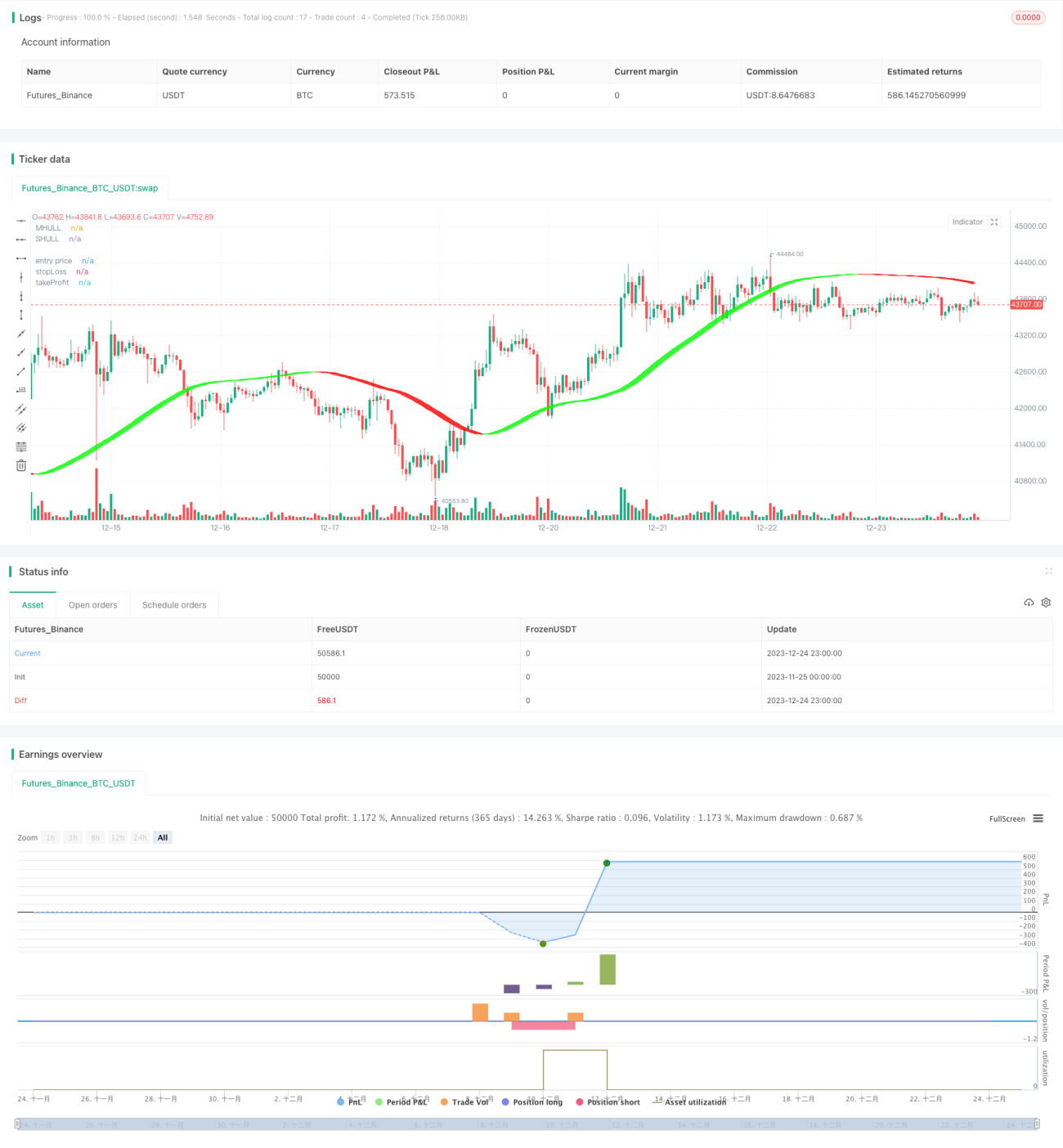

Esta estratégia utiliza múltiplos indicadores quantitativos para determinar os momentos de compra e venda do Bitcoin, realizando negociações automatizadas. Inclui principalmente o Indicador Hull (Hull), Índice de Força Relativa (RSI), Bandas de Bollinger (BB) e Oscilador de Volume (VO).

Princípios da Estratégia

-

Utiliza a Média Móvel de Hull modificada para determinar a direção principal da tendência do mercado, combinada com as Bandas de Bollinger para auxiliar na identificação de pontos de compra e venda por rompimento.

-

O indicador RSI, combinado com uma faixa de volatilidade adaptativa, identifica zonas de sobrecompra e sobrevenda, emitindo sinais de negociação. Simultaneamente, são configurados dois conjuntos de parâmetros como verificação de sinal Duplicado.

-

O Oscilador de Volume avalia a força de compra e venda, evitando rompimentos falsos.

-

Com base nos parâmetros de relação preço de stop loss / preço de take profit, são pré-definidos níveis de stop loss e take profit, implementando o gerenciamento de risco.

Análise de Vantagens

-

A Curva de Hull captura as mudanças de tendência mais rapidamente, e o auxílio das Bandas de Bollinger reduz sinais falsos.

-

A otimização dos parâmetros do indicador RSI e a verificação com sinais Duplicados proporcionam maior confiabilidade.

-

O Oscilador de Volume, combinado com a tendência e os sinais dos indicadores, evita negociações imprecisas.

-

O método de stop loss e take profit pré-definido controla automaticamente o lucro/prejuízo de cada operação, gerenciando efetivamente o risco geral.

Análise de Riscos

-

A configuração inadequada de parâmetros pode resultar em frequência excessiva de negociações ou na deterioração da eficácia dos sinais.

-

Em eventos inesperados que causam forte volatilidade do mercado, o stop loss pode ser ultrapassado, resultando em perdas significativas.

-

Ao alterar o ativo negociado para outra criptomoeda, os parâmetros precisam ser novamente testados e otimizados.

-

Quando os dados de volume estão ausentes, o Oscilador de Volume se torna ineficaz.

Direções de Otimização

-

Realizar mais testes de combinações de parâmetros do RSI para encontrar os parâmetros ideais.

-

Experimentar a combinação de outros indicadores como MACD, KD, etc., com o RSI para melhorar a precisão dos sinais.

-

Adicionar um módulo de previsão de modelo, combinando aprendizado de máquina para determinar a direção do mercado.

-

Testar o efeito dos parâmetros ao mudar para outros ativos negociados.

-

Otimizar o algoritmo de stop loss e take profit para maximizar os lucros.

Resumo

Esta estratégia utiliza de forma abrangente múltiplos indicadores técnicos quantitativos para determinar os momentos de compra e venda. Através de otimização de parâmetros, controle de risco e outros métodos, realiza a negociação automatizada do Bitcoin. O efeito é positivo, mas ainda requer testes e otimizações contínuas para se adaptar às mudanças do mercado. Pode servir como referência para investidores, auxiliando na tomada de decisões de negociação.

- 1