Estratégia de Negociação de Pullback com Cruzamento Descendente das Bandas de Bollinger e RSI

Visão Geral

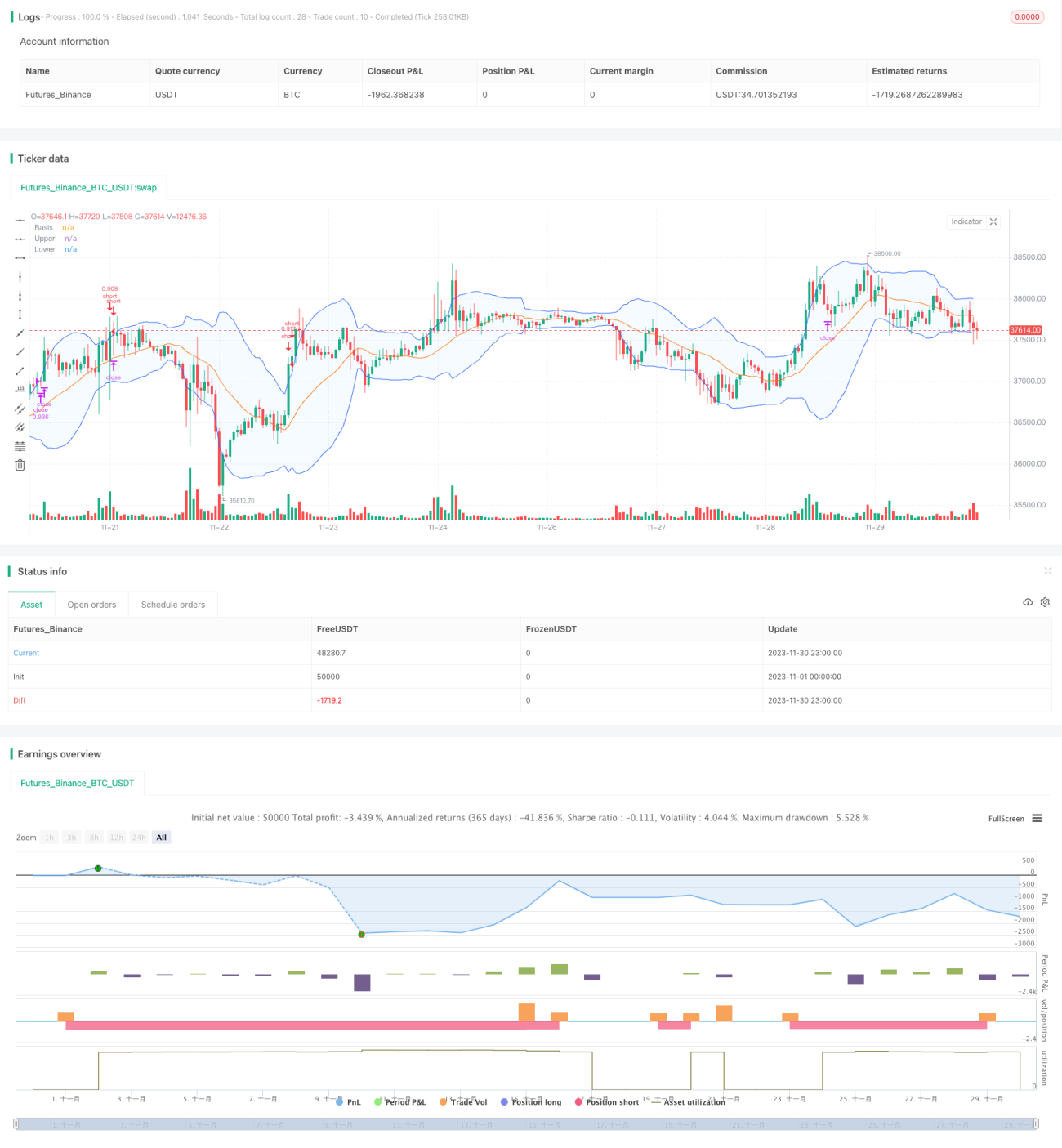

Esta estratégia utiliza as Bandas de Bollinger para identificar se o preço está em uma zona de sobrecompra ou sobrevenda, combinando com o indicador RSI para determinar oportunidades de reversão. Gera uma posição vendida quando ocorre um cruzamento de morte na zona de sobrecompra, e realiza o fechamento da posição para conter perdas quando o preço sobe acima da Banda Superior de Bollinger.

Princípio da Estratégia

A estratégia baseia-se principalmente nos seguintes princípios:

- Quando o preço de fechamento cruza acima da Banda Superior de Bollinger, indica que o ativo entrou em zona de sobrecompra, havendo potencial de correção.

- O indicador RSI pode identificar eficazmente zonas de sobrecompra/sobrevenda, sendo RSI > 70 considerado zona de sobrecompra.

- Quando o preço de fechamento cruza abaixo da Banda Superior, abre-se uma posição vendida.

- O fechamento da posição ocorre quando o RSI recua da zona de sobrecompra ou quando o limite de stop loss é acionado.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Utiliza Bandas de Bollinger para identificar zonas de sobrecompra/sobrevenda, aumentando a taxa de acerto das operações.

- Combina o RSI para filtrar oportunidades falsas de rompimento, evitando perdas desnecessárias.

- Alta relação risco/retorno, maximizando o controle de risco.

Análise de Riscos

A estratégia apresenta os seguintes riscos:

- Após romper a Banda Superior, o preço pode continuar subindo, ampliando ainda mais as perdas.

- O RSI pode não recuar a tempo, agravando as perdas.

- Posição unilateral, impossibilitando a negociação em mercados laterais.

Os riscos podem ser reduzidos através das seguintes medidas:

- Ajustar adequadamente o ponto de stop loss para cortar perdas rapidamente.

- Combinar outros indicadores para identificar sinais de recuo do RSI.

- Incorporar indicadores de média móvel para identificar se o mercado entrou em fase lateral.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Otimizar os parâmetros das Bandas de Bollinger para melhor adaptação a diferentes instrumentos.

- Otimizar os parâmetros do RSI para melhorar a eficácia do indicador.

- Adicionar combinações de outros indicadores para identificar pontos de reversão de tendência.

- Incluir lógica de operação de compra.

- Combinar estratégias de stop loss para ajustar dinamicamente o nível de stop.

Resumo

No geral, esta estratégia é uma típica estratégia de curto prazo para zona de sobrecompra. Utiliza as Bandas de Bollinger para definir pontos de entrada e saída, e o RSI para filtrar sinais. O controle de risco é realizado por meio de um stop loss adequado. Pode ser aprimorada através da otimização de parâmetros, combinação de indicadores e inclusão de novas lógicas de abertura de posição.

- 1