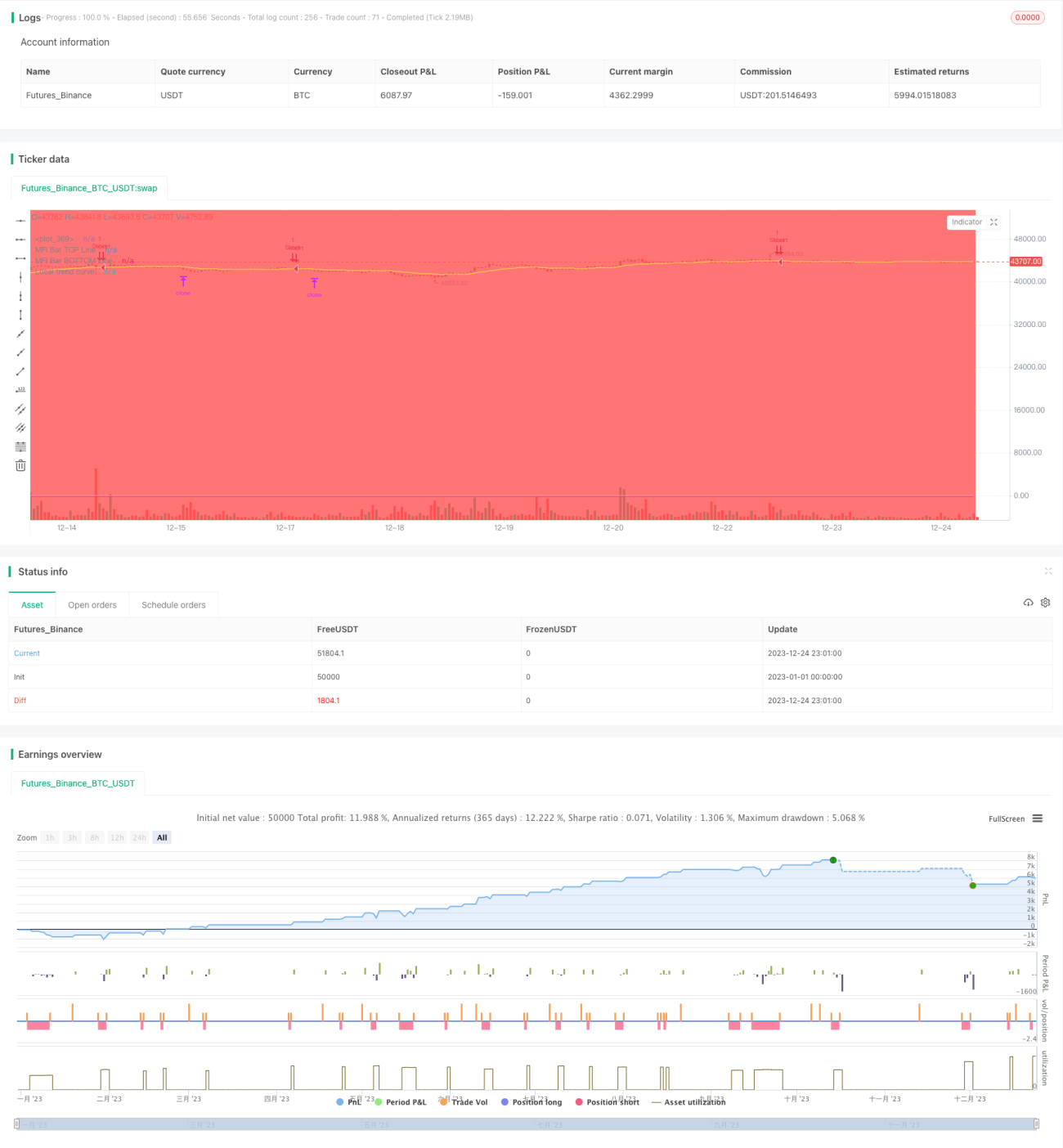

Estratégia de negociação quantitativa baseada em filtro de tendência duplo

Visão Geral

Esta é uma estratégia de trading quantitativo que utiliza um filtro de tendência dupla. A estratégia combina um filtro de tendência global e um filtro de tendência local, garantindo que as posições sejam abertas apenas quando a direção da tendência está correta. Além disso, a estratégia define várias outras condições de filtro, como filtro RSI, filtro de preço, filtro de inclinação, etc., para melhorar ainda mais a confiabilidade dos sinais de negociação. No que diz respeito à saída, a estratégia pré-define níveis de stop loss e take profit. No geral, esta é uma estratégia de trading quantitativo estável e precisa.

Princípios da Estratégia

A lógica central da estratégia baseia-se no filtro de tendência dupla. O filtro de tendência global utiliza uma EMA de período mais longo para julgar a tendência geral do mercado, enquanto o filtro de tendência local utiliza uma EMA de período mais curto para julgar a tendência local. Apenas quando ambos os filtros concordam com a mesma tendência, uma posição é aberta.

Especificamente, a estratégia calcula a linha EMA do BTCUSDT para determinar se o mercado geral está em uma tendência de alta ou de baixa – este é o filtro de tendência global. Ao mesmo tempo, a estratégia calcula a linha EMA do contrato atual para determinar a tendência local – este é o filtro de tendência local. Quando ambos concordam, combinados com vários outros filtros auxiliares, a estratégia gera um sinal de negociação e pré-define preços de take profit e stop loss antes de abrir a posição.

Após determinar o sinal de negociação, a estratégia envia imediatamente a ordem de abertura. Simultaneamente, a estratégia pré-define os preços de take profit e stop loss. Quando o preço atinge o take profit ou stop loss, a estratégia automaticamente realiza o lucro ou interrompe a perda.

Análise de Vantagens

Esta é uma estratégia de trading quantitativo estável e confiável, com as seguintes vantagens principais:

-

Utiliza um mecanismo de filtro de tendência dupla, capaz de filtrar a maioria dos sinais falsos, tornando os sinais de negociação mais confiáveis e precisos.

-

Combina vários filtros auxiliares, como filtro RSI, filtro de preço, etc., melhorando ainda mais a qualidade dos sinais.

-

Calcula automaticamente os níveis de take profit e stop loss, sem necessidade de monitoramento manual, reduzindo o risco de negociação.

-

Os parâmetros da estratégia podem ser personalizados e ajustados, adaptando-se a mais instrumentos de negociação, com forte adaptabilidade.

-

A lógica da estratégia é clara e fácil de entender, facilitando a otimização e melhoria, com grande potencial de expansão.

Análise de Riscos

Embora a estratégia tenha muitas vantagens, ainda existem alguns riscos de negociação, concentrados principalmente em:

-

O filtro de tendência dupla pode não determinar o momento de entrada com precisão. Isso pode ser otimizado ajustando os parâmetros do filtro.

-

A definição imprecisa dos níveis de take profit e stop loss pode resultar em saídas prematuras. Testar diferentes combinações de parâmetros pode ajudar a encontrar a solução ideal.

-

A escolha inadequada do instrumento de negociação ou período pode tornar a estratégia ineficaz. Recomenda-se realizar a otimização e teste de parâmetros separadamente para cada instrumento.

-

Existe algum risco de overfitting. É necessário realizar backtesting em mais ambientes de mercado para garantir a robustez da estratégia.

Direções de Otimização

A estratégia pode ser otimizada principalmente nas seguintes direções:

-

Ajustar os parâmetros dos dois filtros para encontrar a melhor combinação de parâmetros.

-

Testar e selecionar os melhores filtros auxiliares.

-

Otimizar o algoritmo de take profit e stop loss para torná-lo mais inteligente.

-

Tentar introduzir técnicas como aprendizado de máquina para permitir o ajuste dinâmico dos parâmetros.

-

Realizar backtesting em mais instrumentos de negociação e períodos mais longos para melhorar a estabilidade da estratégia.

Resumo

No geral, esta é uma estratégia de trading quantitativo estável, precisa e fácil de otimizar. Ela utiliza um filtro de tendência dupla combinado com vários filtros auxiliares para gerar sinais de negociação, filtrando a maior parte do ruído e tornando os sinais mais precisos e confiáveis. Além disso, a estratégia incorpora a definição de take profit e stop loss, reduzindo o risco de negociação. Esta é uma estratégia de grande valor prático; após otimização e validação, pode ser diretamente aplicada em negociações reais. Ela também possui grande potencial de expansão, sendo uma estratégia quantitativa que vale a pena estudar a fundo.

- 1