Estratégia de trading quantitativo combinando tendência e oscilação

Visão Geral

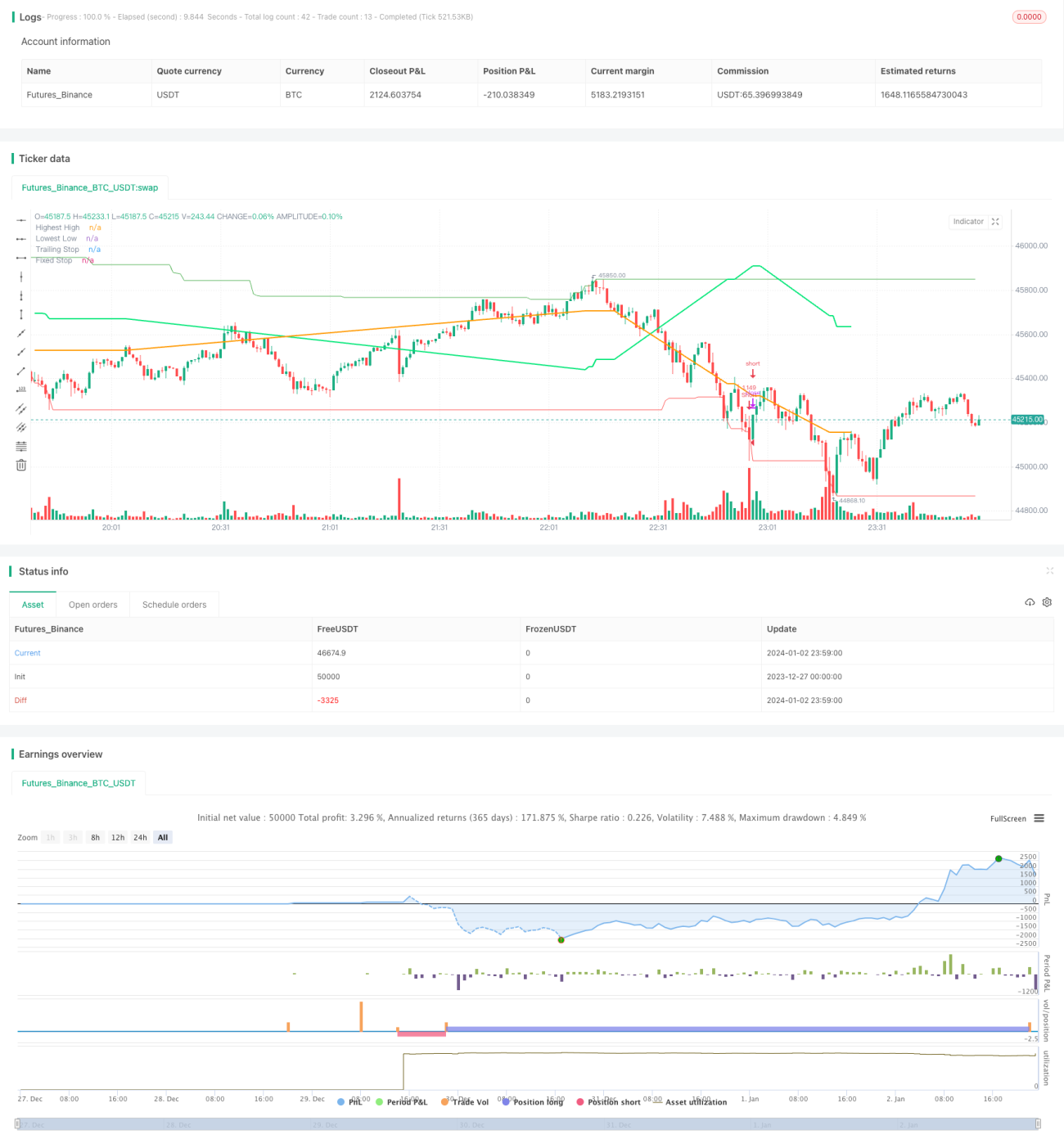

A estratégia de oscilação de dupla tendência é uma estratégia de trading quantitativa que combina tendência e oscilação. Ela utiliza a combinação de dois indicadores para identificar a direção e a força da tendência, e busca melhores pontos de entrada durante as oscilações da tendência.

Princípio da Estratégia

A estratégia utiliza principalmente dois indicadores públicos: Trend Surfers e Mawreez's Trend Oscillator.

Trend Surfers é um indicador de stop loss baseado em tendência. Ele calcula os preços máximos e mínimos em um determinado período para avaliar a movimentação dos preços e sugerir níveis de stop loss. Por exemplo, quando o preço rompe a máxima das últimas 168 barras, é um sinal de alta; quando o preço rompe a mínima das últimas 168 barras, é um sinal de baixa.

Mawreez's Trend Oscillator é um indicador oscilador de duas linhas. Semelhante ao MACD, ele utiliza a diferença do DI para avaliar a direção e a força da tendência. A curva do indicador acima da linha zero indica alta, e abaixo indica baixa.

As regras de trading da estratégia são:

Entrada em posição comprada: quando Trend Surfers rompe a máxima e o indicador Mawreez's Trend Oscillator está em alta.

Entrada em posição vendida: quando Trend Surfers rompe a mínima e o indicador Mawreez's Trend Oscillator está em baixa.

O stop loss é uma combinação de stop loss trailing e stop loss fixo.

Análise de Vantagens

A estratégia combina indicadores de tendência e oscilação, permitindo capturar tanto tendências quanto encontrar melhores preços de entrada em oscilações. As vantagens incluem:

- Filtro duplo de indicadores, evitando efetivamente falsos rompimentos.

- Combinação de tendência e oscilação, facilitando a captura de acumulação em zonas de oscilação com preços baixos ou alívio de posições em níveis elevados.

- Múltiplos métodos de stop loss, permitindo um bom controle de risco.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- Combinação dupla de indicadores, podendo perder sinais.

- Indicadores de tendência e oscilação podem emitir sinais conflitantes.

- Stop loss fixo pode ser acionado precocemente.

Para mitigar esses riscos, podem ser adotadas as seguintes medidas:

- Ajustar parâmetros dos indicadores de forma mais flexível, reduzindo a taxa de filtragem.

- Adicionar regras de identificação de tendência para evitar conflitos entre indicadores.

- Ajustar dinamicamente os níveis de stop loss.

Direções de Otimização

A estratégia possui espaço adicional para otimização:

- Testar diferentes combinações de parâmetros e períodos para encontrar os melhores parâmetros.

- Adicionar regras auxiliares como volatilidade, volume de negociação, etc.

- Utilizar técnicas de aprendizado de máquina para otimizar dinamicamente indicadores e parâmetros.

Resumo

A estratégia de oscilação de dupla tendência combina as vantagens dos indicadores de tendência e oscilação, permitindo identificar a direção da tendência e aproveitar oportunidades de oscilação. Através da otimização de parâmetros e regras, a rentabilidade da estratégia pode ser ainda mais aprimorada. Esta estratégia apresenta boas perspectivas de desenvolvimento.

- 1