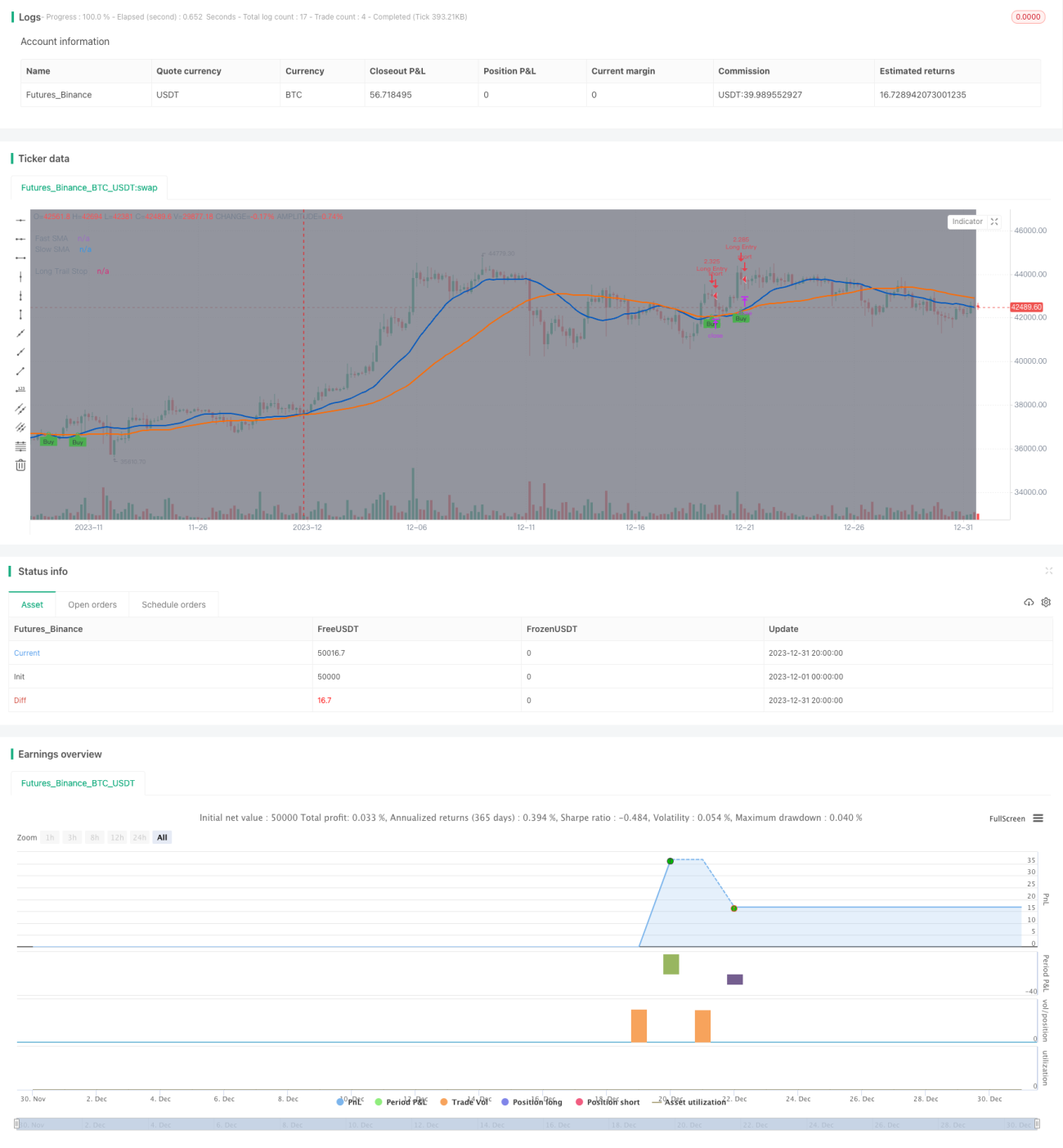

Estratégia de Trailing Stop Dinâmico

Visão Geral

Esta estratégia determina a tendência através do cruzamento entre uma média móvel rápida e uma média móvel lenta. Quando a média móvel rápida cruza acima da média móvel lenta, é feita uma posição comprada (long), e uma linha de stop loss dinâmico é definida para travar os lucros, saindo da posição quando o preço varia uma determinada percentagem.

Princípio da Estratégia

A estratégia utiliza o cruzamento de alta (golden cross) entre a média móvel rápida e a média móvel lenta para identificar o início de uma tendência de alta. Especificamente, calcula-se a média móvel simples dos preços de fecho num determinado período, comparando os valores da média rápida com a média lenta. Quando a média rápida cruza acima da média lenta, considera-se que a tendência de alta começou, abrindo então uma posição comprada.

Após abrir a posição comprada, a estratégia não define um stop loss fixo, mas sim uma linha de stop loss dinâmico para travar os lucros. Esta linha de stop loss é definida da seguinte forma: Preço Máximo * (1 - Percentagem de Stop Loss definida). Isto permite que o stop loss suba à medida que o preço aumenta, saindo da posição quando ocorre uma queda de uma determinada percentagem.

A vantagem desta abordagem é que permite acompanhar o movimento de alta indefinidamente, podendo travar os lucros através do stop loss após atingir um determinado nível de ganho.

Análise de Vantagens

As principais vantagens desta estratégia de stop loss dinâmico são:

-

Permite acompanhar o movimento de alta indefinidamente, sem perder grandes tendências. Um stop loss fixo pode facilmente ser acionado no início de uma grande tendência.

-

Permite travar lucros definindo uma percentagem de stop loss. Se apenas se acompanhar a tendência sem parar perdas, pode-se acabar por ter prejuízo no final do movimento. Definir um stop loss permite garantir os lucros.

-

É mais flexível do que um stop loss fixo. Um stop loss fixo só permite definir um preço, enquanto este stop loss varia com o preço máximo.

-

O risco de drawdown é menor. Com um stop loss fixo, a distância do stop loss ao preço máximo é maior, podendo ser acionado em correções normais. Aqui, o stop loss está próximo do preço máximo, não sendo acionado em correções normais.

Análise de Riscos

Esta estratégia também apresenta alguns riscos:

-

O indicador que determina o sinal de entrada pode ser instável, gerando sinais falsos.

-

O método de stop loss é único, sem considerar outros fatores. O mercado pode sofrer alterações súbitas e significativas que tornem a estratégia ineficaz.

-

Não tem limite de take profit, dependendo apenas do stop loss. Se o stop loss falhar, pode causar perdas consideráveis.

-

Os parâmetros precisam de otimização. Períodos como o das médias móveis precisam de ser ajustados para valores ótimos.

Direções de Otimização

Esta estratégia pode ser otimizada nos seguintes aspetos:

-

Adicionar mais indicadores para confirmar a entrada, evitando sinais falsos. Por exemplo, incluir a análise do volume.

-

Adicionar uma definição de take profit. Fechar a posição quando o lucro atinge uma determinada percentagem.

-

Aumentar a segurança do stop loss. Ajustar significativamente a distância do stop loss quando o mercado apresenta comportamentos anómalos.

-

Otimizar para diferentes instrumentos de negociação e períodos de negociação. Os parâmetros variam conforme o instrumento e o período.

-

Incorporar machine learning para ajustar dinamicamente os parâmetros. Permitir que o modelo otimize automaticamente os indicadores de decisão e a amplitude do stop loss.

Resumo

Esta estratégia tem uma lógica geral clara e razoável. Usar o cruzamento de médias móveis para determinar a tendência é um método clássico, e a técnica de stop loss dinâmico pode efetivamente travar lucros e reduzir riscos. No entanto, estes indicadores e parâmetros precisam de ser constantemente testados e otimizados para que a estratégia gere lucros de forma consistente. Também é necessário proteger a estratégia contra alterações significativas do mercado, o que exige o aperfeiçoamento da lógica geral e do quadro conceptual, bem como a implementação de mecanismos de segurança adicionais.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1