Estratégia de reversão de tendência de criptomoedas baseada em pontos altos e baixos do PIVOT

Visão Geral

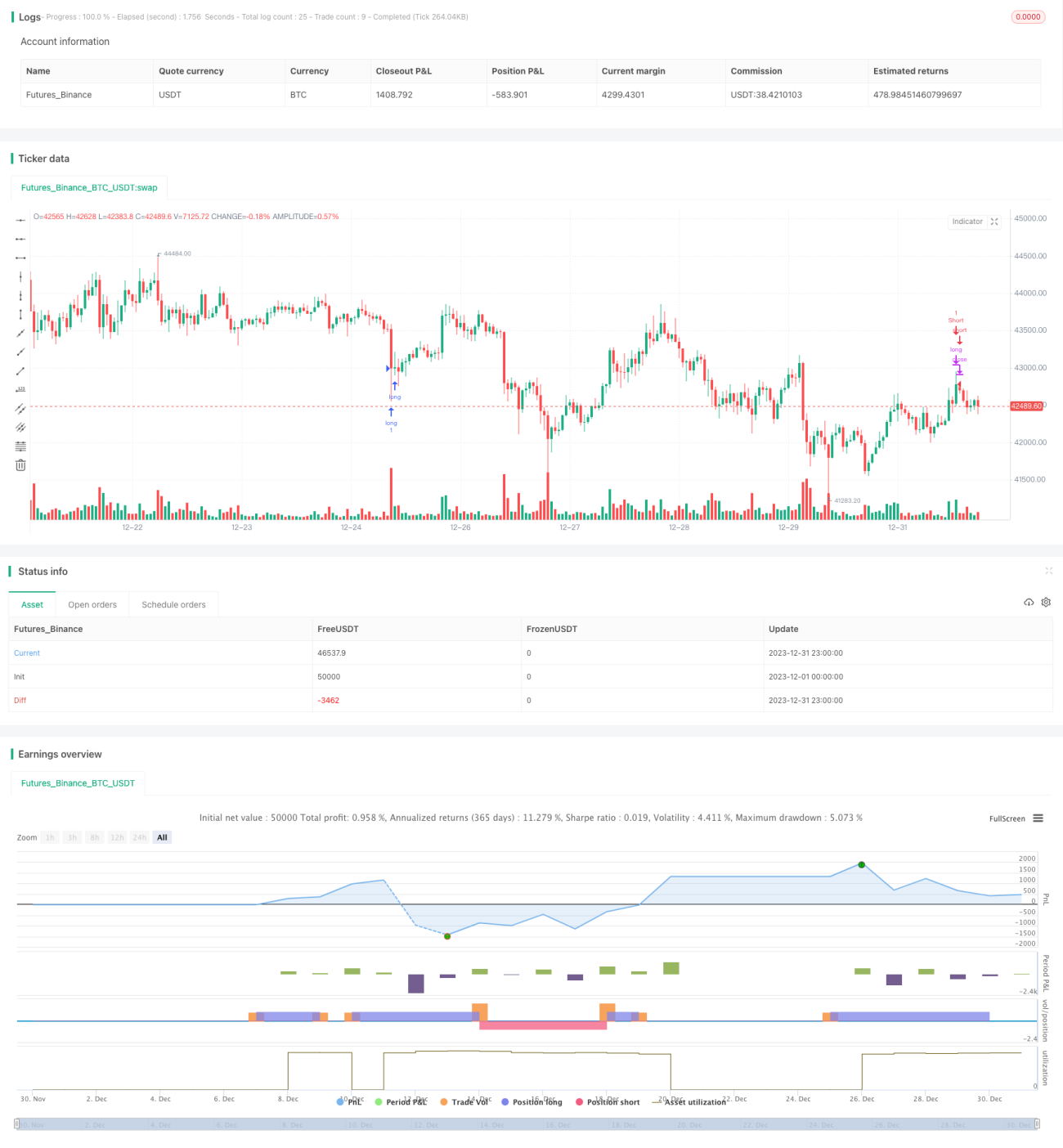

Esta estratégia baseia-se nos pontos de pivot (máximos e mínimos) e na sua rutura para identificar reversões de tendência em criptomoedas, sendo classificada como uma estratégia de reversão por rutura. A estratégia primeiro calcula os pontos de pivot de máximo e mínimo do ativo num determinado período recente e, em seguida, verifica se o preço rompe esses níveis-chave e sofre uma reversão, de modo a capturar grandes mudanças de tendência.

Princípio da Estratégia

-

Cálculo dos pontos de pivot máximos e mínimos

Utiliza as funções

ta.pivothigh()eta.pivotlow()para calcular os pontos de preço mais alto e mais baixo num determinado número de barras recentes, que servem como pontos de pivot-chave. -

Identificação da rutura

Se o preço romper para cima um ponto de pivot mínimo, ou para baixo um ponto de pivot máximo, considera-se que ocorreu uma reversão de tendência.

-

Definição de critérios de filtro

Exige-se que o preço ultrapasse o ponto de pivot com uma margem significativa e que rompa a média de fecho das últimas 150 barras, evitando ser apanhado em movimentos falsos.

-

Entrada e saída

Quando a condição de compra é acionada, entra-se numa posição longa; quando a condição de venda é acionada, fecha-se a posição longa. O mesmo raciocínio aplica-se para entradas e saídas curtas.

Análise de Vantagens

- O uso de pontos de pivot torna a estratégia sensível a grandes mudanças de tendência.

- Os filtros eficazes evitam a entrada durante movimentos laterais, garantindo que a entrada ocorre apenas após a confirmação da reversão.

- Como identifica ruturas nos pontos de pivot máximos e mínimos, consegue capturar oportunidades de reversão atempadamente.

Análise de Riscos

- Movimentos laterais prolongados podem levar a que a estratégia fique presa em posições.

- É necessário ajustar o comprimento dos pontos de pivot e os critérios de filtro para se adequarem a diferentes ativos.

- É essencial que as taxas de corretagem sejam próximas de zero, caso contrário o impacto nos ganhos/perdas pode ser significativo.

Direções de Otimização

- Testar diferentes combinações de parâmetros para os pontos de pivot.

- Adicionar um stop loss móvel para controlar perdas individuais.

- Combinar com outros indicadores para filtrar sinais.

Conclusão

A estratégia é globalmente robusta e adequada para capturar grandes reversões. No entanto, é necessário controlar o risco e ajustar os parâmetros a diferentes moedas. Com uma otimização adequada dos parâmetros e uma gestão de risco eficaz, a estratégia pode obter bons resultados.

- 1