Estratégia de seguimento de tendência baseada em média móvel SSL

Visão Geral

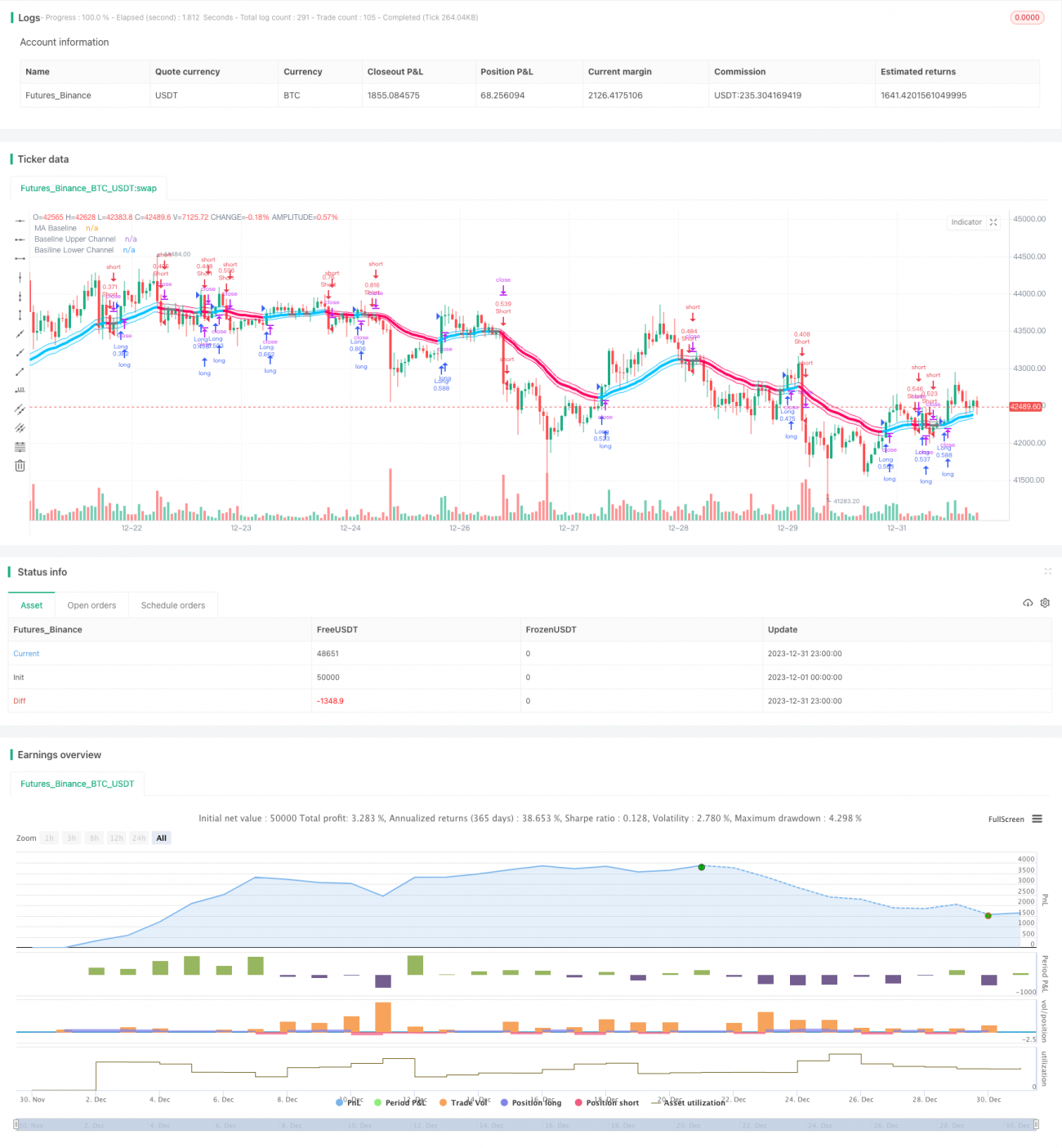

Esta estratégia utiliza o indicador de canal SSL para julgar a tendência do mercado e segue a tendência com base em uma média móvel. É adequado para gráficos de 4 horas e diários de médio a longo prazo.

Princípio da Estratégia

-

O canal SSL é composto pela média móvel de Keltner e pela amplitude verdadeira. Ele pode determinar a direção da tendência do mercado. Quando o preço ultrapassa a banda superior, é um sinal de alta; quando ultrapassa a banda inferior, é um sinal de baixa.

-

A estratégia utiliza indicadores de média móvel como a EMA para calcular uma média móvel de referência. Essa média pode filtrar parte dos falsos rompimentos.

-

A estratégia compra quando o preço rompe a banda superior do SSL e vende quando o preço rompe a banda inferior do SSL. Em uma tendência de alta, persegue altas e vende baixas; em uma tendência de baixa, compra na parte inferior (“pega a faca”).

-

Os métodos de stop loss incluem stop loss percentual, stop loss ATR e stop loss com lookback de menor/maior preço. O take profit é N vezes o stop loss. Os parâmetros específicos são definidos pelo usuário.

Análise de Vantagens

-

O canal SSL determina a direção da tendência com precisão, reduzindo sinais falsos. Combinado com a média móvel como base de entrada, evita comprar topos e vender fundos.

-

Permite selecionar diferentes tipos de médias móveis com flexibilidade, adaptando-se a situações de mercado mais amplas.

-

Os métodos de stop loss são flexíveis e variados, permitindo controlar o risco. O múltiplo de take profit também pode ser ajustado de forma flexível para atender a diferentes preferências.

-

Pode operar tanto comprado quanto vendido simultaneamente, explorando ao máximo as oportunidades bidirecionais do mercado.

Análise de Riscos

-

Os indicadores de média móvel possuem defasagem, podendo acumular perdas.

-

Em mercados laterais, o preço pode inverter logo após romper as bandas, resultando em posições presas.

-

O stop loss com ATR e lookback pode ser muito amplo em rompimentos anormais, aumentando as perdas.

Medidas para mitigar riscos:

- Ajustar adequadamente os parâmetros da média móvel ou escolher outros tipos de média.

- Aumentar a amplitude do stop loss e interromper as perdas em tempo hábil.

- Adicionar um fator multiplicador no ATR ou ajustar o período de lookback.

Direções de Otimização

- Testar mais tipos de indicadores de média móvel para encontrar os melhores parâmetros.

- Otimizar o período do ATR para stop loss.

- Testar diferentes parâmetros de múltiplo de stop loss.

- Testar diferentes coeficientes de risco para take profit.

Resumo

Esta estratégia combina o SSL para julgar a tendência e indicadores de média móvel para confirmar a entrada, permitindo seguir a tendência de forma eficaz. Ela oferece métodos flexíveis de stop loss e take profit, controlando o risco enquanto obtém retornos mais elevados. Através de testes e otimizações contínuas dos parâmetros, é possível alcançar um desempenho comercial superior. É uma estratégia eficaz que vale a pena acompanhar e utilizar no longo prazo.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1