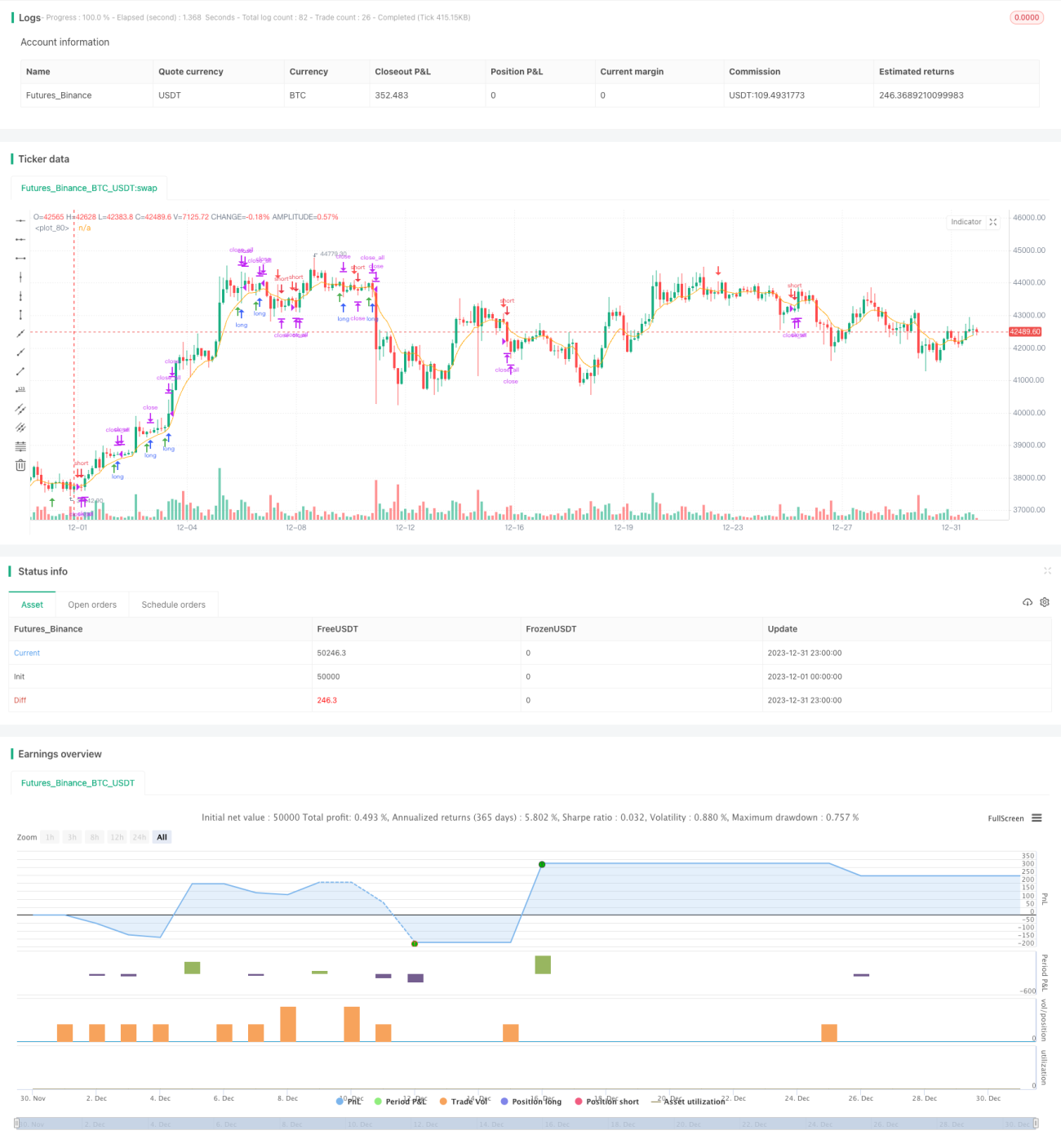

Estratégia de Reversão e Seguimento de Tendência de Curto Prazo

Visão Geral

A estratégia de reversão de tendência por rastreamento é uma estratégia de negociação de curto prazo baseada em futuros NQ de 15 minutos. Ela utiliza filtragem de tendência e identificação de padrões de reversão para encontrar oportunidades de negociação. A estratégia é simples e eficaz, adequada para traders ativos de curto prazo.

Princípio da Estratégia

A estratégia funciona principalmente com base nos seguintes princípios:

-

Utiliza uma EMA de 8 períodos como principal filtro de tendência: acima da EMA, visão de alta; abaixo da EMA, visão de baixa.

-

Identifica padrões específicos de reversão de candlestick como sinais de entrada, incluindo sinais de alta após uma longa vela de alta seguida por uma curta vela de baixa, e sinais de baixa após uma longa vela de baixa seguida por uma curta vela de alta. Esses padrões indicam que a tendência pode estar começando a reverter.

-

O ponto de entrada é definido próximo ao ponto mais alto ou mais baixo da vela de reversão, e o stop loss é definido no ponto mais alto ou mais baixo da própria vela de reversão, proporcionando uma relação risco-retorno eficiente.

-

Utiliza a relação entre os corpos das velas para julgar a validade do sinal de reversão, como regras de que o preço de abertura da vela de baixa está acima do corpo da vela anterior, ou que o corpo está completamente contido, para filtrar ruídos.

-

Opera apenas em períodos específicos de negociação, evitando períodos especiais como a rolagem de contratos principais do mercado, prevenindo perdas desnecessárias devido a movimentos anormais do mercado.

Análise de Vantagens

A estratégia possui as seguintes vantagens principais:

-

Os sinais da estratégia são simples e eficazes, fáceis de entender e implementar.

-

Baseada em julgamento de tendência e reversão, evita ser prejudicada tanto em mercados de touro quanto de urso.

-

Controle de risco adequado, com stop loss razoável, favorecendo a gestão de capital.

-

Exige poucos dados, adequada para uso em diversos softwares e plataformas.

-

Frequência de negociação relativamente alta, adequada para investidores que preferem negociações ativas de curto prazo.

Riscos e Contramedidas

A estratégia também apresenta alguns riscos, sendo os principais:

-

Oportunidades insuficientes de padrões de reversão, com poucos sinais. Pode-se relaxar um pouco as regras de identificação de reversão.

-

Problemas frequentes de falsos rompimentos. Podem ser adicionados mais indicadores de filtro para julgamento conjunto.

-

Instabilidade durante o período noturno e horários não convencionais. Pode-se configurar para operar apenas durante o horário de negociação dos EUA.

-

Espaço limitado para otimização de parâmetros. Pode-se tentar técnicas como aprendizado de máquina para encontrar parâmetros melhores.

Direções de Otimização

A estratégia ainda possui algum espaço para otimização, principalmente nas seguintes direções:

-

Testar parâmetros de EMA com períodos mais longos para melhorar o julgamento de tendência.

-

Adicionar índices do mercado de ações como filtro adicional de tendência.

-

Utilizar técnicas como aprendizado de máquina para otimizar automaticamente os pontos de entrada e stop loss.

-

Adicionar mecanismos dinâmicos de ajuste de posição e stop loss baseados em volatilidade.

-

Tentar arbitragem entre múltiplos ativos para diversificar o risco sistêmico de um único ativo.

Conclusão

A estratégia de reversão de tendência por rastreamento é, de modo geral, uma abordagem muito prática para estratégias de curto prazo. Com parâmetros simples e fáceis de implementar, permite um bom controle de risco individual, sendo adequada para traders ativos de curto prazo em fóruns de ações. A estratégia possui algum espaço para otimização; com certo investimento em pesquisa e desenvolvimento, pode até ser adequada para operações programadas de capital de médio a longo prazo, apresentando bom potencial de desenvolvimento.

- 1