Estratégia de Captura de Cruzamento de Reversão

Visão Geral

A Estratégia de Captura de Reversão com Cruzamento é uma estratégia composta que combina negociação de reversão e cruzamento de indicadores. Ela primeiro utiliza padrões de reversão de preço para gerar sinais de negociação e, em seguida, aplica o cruzamento de alta/baixa do oscilador estocástico como filtro, capturando assim oportunidades de reversão de curto prazo no mercado.

Princípio da Estratégia

A estratégia consiste em duas subestratégias:

-

Estratégia de Reversão 123

- Quando o preço de fechamento passa de uma máxima para uma mínima em dois dias, se o oscilador estocástico de 9 períodos estiver em nível baixo (abaixo de determinado valor), gera um sinal de compra.

- Quando o preço de fechamento passa de uma mínima para uma máxima em dois dias, se o oscilador estocástico de 9 períodos estiver em nível alto (acima de determinado valor), gera um sinal de venda.

-

Estratégia de Cruzamento de Ouro/Morte do Estocástico

- Quando a linha %K cruza para baixo a linha %D, e ambas as linhas %K e %D estão na zona de sobrecompra, gera um sinal de venda.

- Quando a linha %K cruza para cima a linha %D, e ambas as linhas %K e %D estão na zona de sobrevenda, gera um sinal de compra.

Esta estratégia composta avalia os sinais das duas subestratégias. Quando os sinais de ambas são concordantes, gera-se um sinal de negociação real.

Vantagens da Estratégia

Esta estratégia combina reversão e cruzamento de indicadores, integrando informações de preço e indicadores. Ela pode filtrar sinais falsos de forma eficaz, explorar oportunidades potenciais de reversão e aumentar a taxa de retorno dos lucros.

As vantagens específicas incluem:

- Captura as reversões do mercado com giro rápido, sem necessidade de longos períodos de oscilação à espera de sinais.

- A validação cruzada das duas subestratégias melhora a precisão dos sinais.

- A combinação da análise do movimento de preços com a análise de indicadores aumenta a taxa de acerto.

Riscos da Estratégia

A estratégia também apresenta alguns riscos:

- Em condições de forte volatilidade do mercado, a direção da reversão do preço no curto prazo pode ser incerta, gerando facilmente sinais errôneos.

- A configuração inadequada dos parâmetros dos indicadores também pode afetar a qualidade dos sinais.

- O timing da reversão não pode ser controlado, havendo um certo risco temporal.

Para mitigar esses riscos, é possível ajustar os parâmetros dos indicadores, estabelecer mecanismos de stop loss, entre outras medidas.

Direções de Otimização da Estratégia

A estratégia pode ser otimizada nas seguintes dimensões:

- Ajustar os parâmetros dos indicadores e otimizar a combinação de parâmetros.

- Adicionar outros indicadores para filtrar sinais, como indicadores de volume.

- Personalizar os parâmetros dos indicadores de acordo com as características de cada ativo e as condições do mercado.

- Adicionar estratégias de stop loss para controlar riscos.

- Incorporar técnicas de aprendizado de máquina para a tomada de decisão dos sinais.

Resumo

A Estratégia de Captura de Reversão com Cruzamento integra as vantagens de múltiplas estratégias, apresentando forte capacidade de lucro sob a premissa de controle de risco. Por meio de otimização e aprimoramento contínuos, é possível desenvolver uma estratégia eficiente adequada ao seu próprio estilo, enfrentando com serenidade as mudanças do mercado.

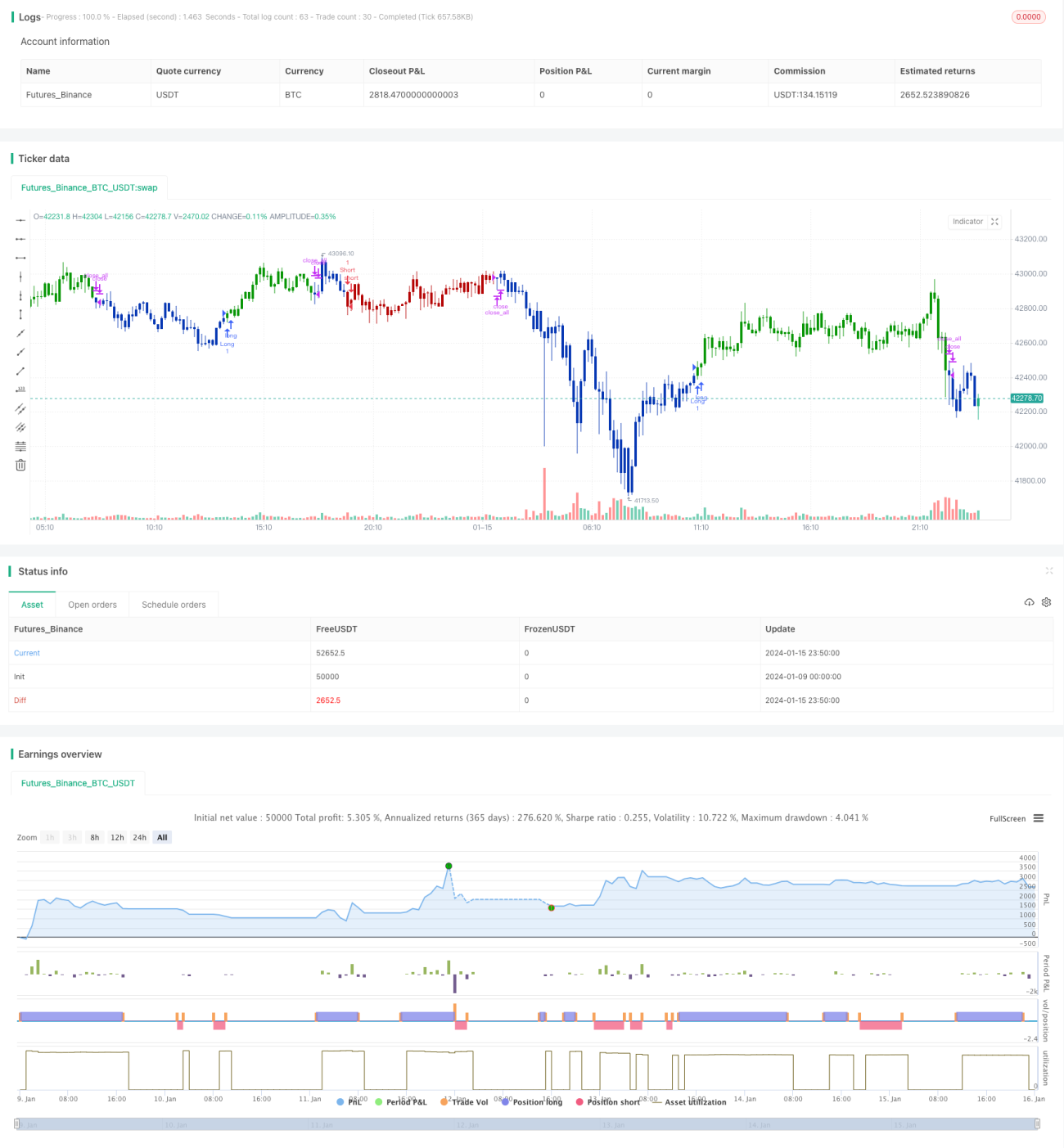

/*backtest

start: 2024-01-09 00:00:00

end: 2024-01-16 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/09/2021

// This is combo strategies for get a cumulative signal. - 1