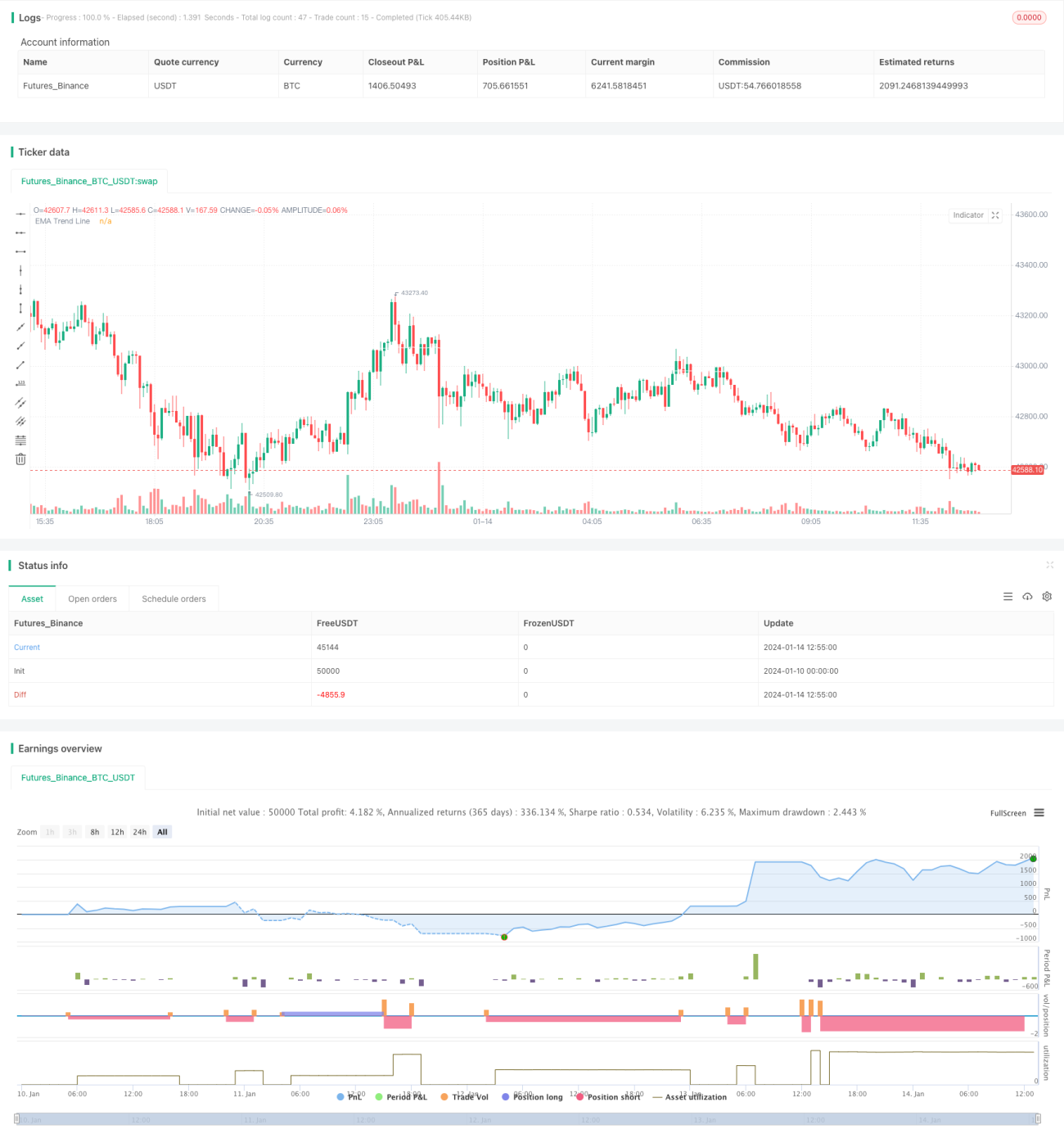

Estratégia de Seguimento de Tendência Combinando Duplo EMA com RSI

Visão Geral

Esta estratégia combina o uso de dupla EMA e o indicador RSI para identificar tendências de preço e entrar no mercado no momento em que a direção da tendência se inverte. Especificamente, a estratégia utiliza uma EMA de período mais longo para determinar a direção principal da tendência, enquanto o RSI identifica condições de sobrecompra e sobrevenda de curto prazo. Quando o preço faz um pullback na direção da tendência principal, o RSI gera um sinal de negociação, e a estratégia opera comprado ou vendido conforme a direção da tendência.

Princípio da Estratégia

-

Uma EMA de 200 períodos é usada para determinar a direção principal da tendência. A travessia do preço acima da linha da EMA é um sinal de alta, e abaixo, um sinal de baixa.

-

O parâmetro do RSI é definido como 10 períodos. O RSI cruzando acima de 40 é um sinal de sobrevenda, e abaixo de 60, um sinal de sobrecompra.

-

Quando a tendência principal é de alta (preço acima da EMA), se ocorrer um sinal de sobrevenda com o RSI cruzando abaixo de 40, entra-se comprado.

-

Quando a tendência principal é de baixa (preço abaixo da EMA), se ocorrer um sinal de sobrecompra com o RSI cruzando acima de 60, entra-se vendido.

-

O stop loss é definido como 4 vezes o ATR. O take profit é definido como 2 vezes o stop loss, resultando em uma relação risco-retorno de 2:1.

Análise de Vantagens

A maior vantagem desta estratégia é combinar indicadores de tendência e reversão, permitindo entrada no mercado durante pullbacks da tendência, resultando em bom desempenho. As vantagens específicas incluem:

-

O uso do sistema de dupla EMA para determinar a direção principal da tendência permite acompanhar efetivamente a tendência dos preços.

-

O RSI identifica condições de sobrecompra e sobrevenda de curto prazo, auxiliando na determinação do momento de entrada.

-

O stop loss baseado no ATR pode ser ajustado conforme a volatilidade do mercado, favorecendo o controle de risco.

-

Seguir rigorosamente os princípios de negociação de tendências reduz negociações desnecessárias e diminui o risco sistêmico.

Análise de Riscos

Os principais riscos desta estratégia são:

-

Durante períodos de tendência lateral ou enfraquecimento, podem ocorrer sinais falsos de negociação. Nesse caso, é necessário avaliar o momento com cautela antes de entrar.

-

Em condições extremas de mercado, o stop loss baseado no ATR pode ser muito largo ou muito apertado, exigindo ajustes dinâmicos. Outros métodos de stop loss também podem ser considerados.

-

A frequência de geração de sinais pode ser alta, sendo importante verificar se está alinhada com sua preferência de frequência de negociação.

-

É necessário monitorar se os parâmetros do RSI estão adequados e realizar otimizações periódicas.

Direções de Otimização

As principais áreas de melhoria da estratégia incluem:

-

Testar a adição de outros indicadores de tendência, como MACD, para auxiliar na determinação da direção.

-

Testar outros indicadores de reversão, como KDJ, Bandas de Bollinger, em combinação com o RSI para encontrar melhores sinais de negociação.

-

Incorporar algoritmos de aprendizado de máquina para ajustar parâmetros de forma adaptativa, implementando stop loss e take profit dinâmicos.

-

Considerar fatores como indicadores de sentimento e notícias para melhorar a robustez geral do sistema.

Resumo

No geral, esta estratégia é uma típica estratégia de curto prazo que combina acompanhamento de tendência e indicadores de reversão. Utiliza a dupla EMA para determinar a tendência principal e o RSI para capturar oportunidades de pullback dentro da tendência. Em princípio, a estratégia combina as vantagens de diferentes indicadores, formando um bom efeito de complementaridade. Se for aprimorada por meio de otimização de parâmetros, fusão de modelos, entre outros métodos, seu desempenho ainda tem grande potencial de melhoria.

- 1