Estratégia do Indicador Mo Fei Atravessando o Tempo e o Espaço

Visão Geral

Este é um estratégia quantitativa simples que utiliza o Indicador Morphic para identificar "grandes tubarões" no mercado. É adequada para o timeframe de 5 minutos e usada principalmente para negociação de criptomoedas.

Princípio da Estratégia

A estratégia utiliza o Indicador Morphic com comprimento 3, definindo a linha de sobrecompra em 100 e a linha de sobrevenda em 0. A estratégia aguarda o Indicador Morphic atingir o nível de sobrecompra, indicando a presença de um "grande tubarão" no mercado. Se nos dois primeiros pontos de sobrecompra do Indicador Morphic do dia o preço ainda conseguir manter uma tendência de alta, isso é um sinal de entrada longa.

Quando o Indicador Morphic = 100 e o próximo candle for uma grande vela de alta, entra-se em uma posição comprada. O stop loss é definido no menor preço do dia de negociação, e o take profit ocorre 60 minutos após a entrada.

Para vendas a descoberto, pode-se usar a lógica espelhada. Ou seja, quando o Indicador Morphic atingir a sobrevenda e o próximo candle for uma grande vela de baixa, entra-se em uma posição vendida.

Vantagens da Estratégia

-

O uso do Indicador Morphic pode identificar efetivamente o comportamento dos "grandes tubarões" acumulando ações com potencial no mercado. Essas ações têm probabilidade de continuar subindo.

-

Utilizar o corpo do candle para identificar pontos de rompimento com força significativa pode filtrar muitos falsos rompimentos.

-

Combinado com o filtro SMA, evita-se comprar ações em tendência de queda, reduzindo efetivamente o risco de negociação.

-

Utilizando um método de negociação de curto prazo intradiário, o take profit em 60 minutos pode bloquear lucros rapidamente, reduzindo a probabilidade de retrações.

Riscos da Estratégia

-

O Indicador Morphic pode gerar sinais falsos, levando a perdas desnecessárias. É possível ajustar adequadamente os parâmetros ou adicionar outros indicadores para fazer a filtragem.

-

O método de negociação de curto prazo de 60 minutos pode ser muito agressivo, não sendo adequado para ações com alta volatilidade. É possível ajustar o tempo de take profit ou usar um stop loss móvel para otimizar.

-

Não se leva em consideração o risco de impacto de mercado causado por eventos macroeconômicos importantes. Nesses casos, a estratégia deve ser pausada até que o mercado se estabilize para continuar negociando.

Direções de Otimização da Estratégia

-

É possível testar diferentes combinações de parâmetros, como ajustar o comprimento do Indicador Morphic e otimizar os parâmetros do período SMA.

-

Tentar adicionar outros indicadores para combinar, como Bandas de Bollinger, Indicador KD, etc., para verificar se a precisão dos sinais pode ser melhorada.

-

Testar um relaxamento adequado da amplitude do stop loss para verificar se é possível obter um lucro maior por operação.

-

Tentar desenvolver versões baseadas neste framework de estratégia para outros timeframes, como versões de 15 minutos ou 30 minutos.

Resumo

No geral, esta estratégia é muito concisa e fácil de entender. A ideia básica é consistente com a abordagem clássica de rastrear os "grandes tubarões". Ao identificar os pontos-chave de sobrecompra e sobrevenda do Indicador Morphic, combinados com a filtragem do corpo do candle, muitos ruídos podem ser filtrados. A adição do filtro SMA também melhora ainda mais a estabilidade da estratégia.

O método de negociação de curto prazo de 60 minutos pode obter lucros rapidamente, mas também traz um risco operacional mais alto. No geral, este é um template de estratégia quantitativa com grande valor prático, que merece pesquisa e otimização aprofundadas, e também nos fornece ideias valiosas para o desenvolvimento de estratégias.

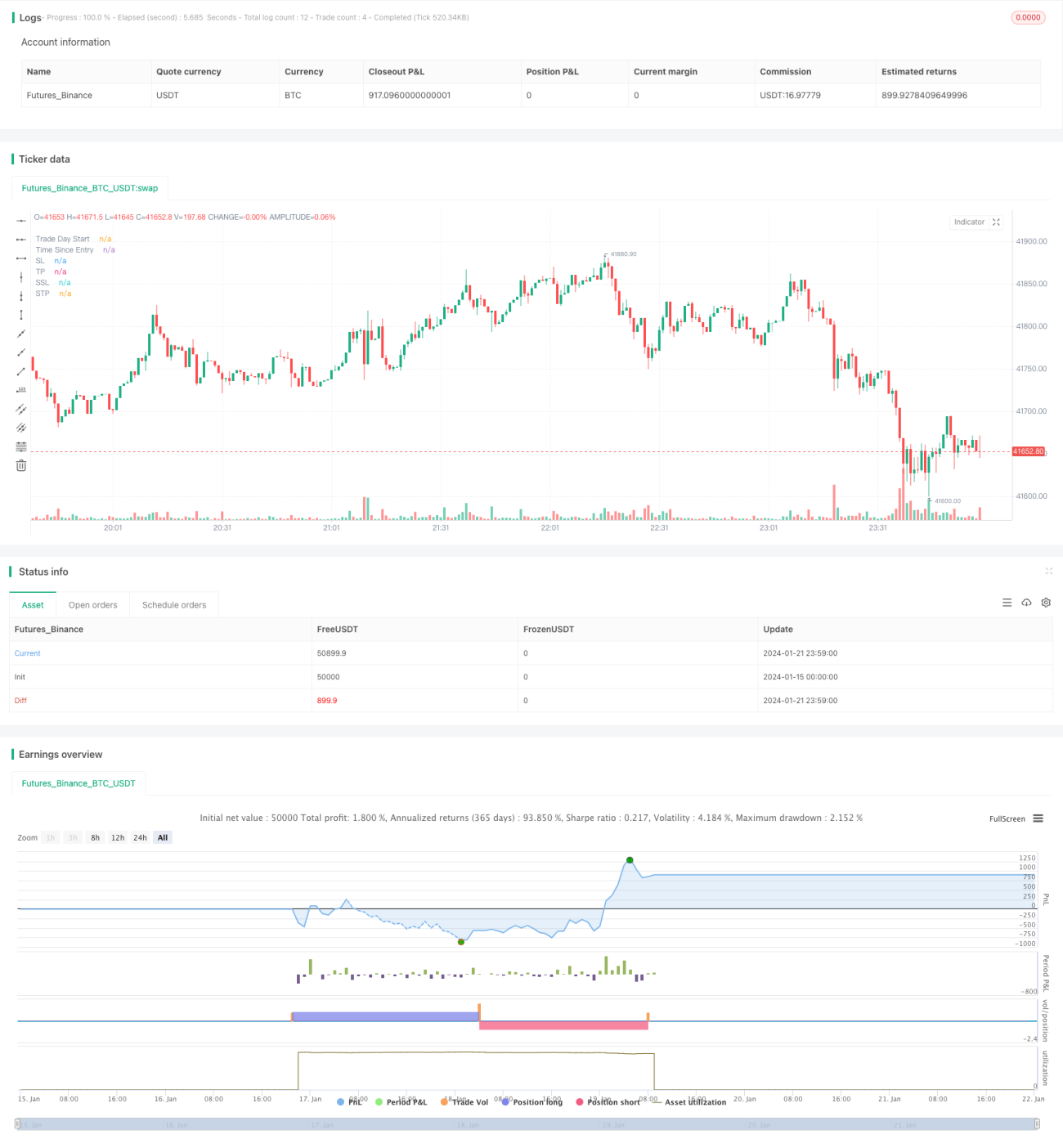

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1