Estratégia de acompanhamento de tendência baseada em médias móveis

Visão Geral

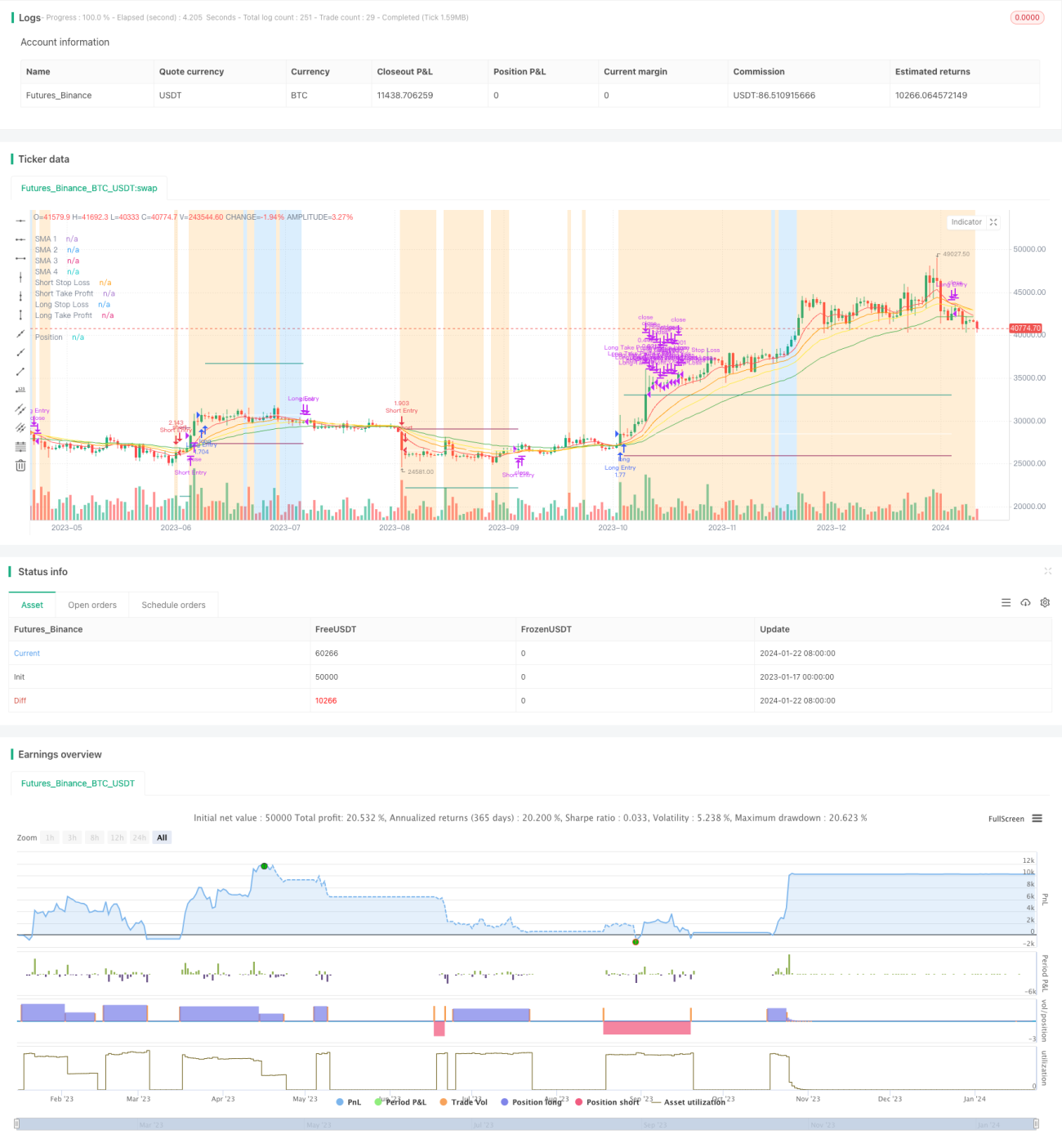

Esta estratégia é uma estratégia simples de seguimento de tendência baseada em médias móveis. Ela determina a direção atual da tendência e sua duração comparando as relações de tamanho entre médias móveis de diferentes períodos. Quando uma média móvel de curto prazo cruza para cima uma de longo prazo, opera-se comprado; quando cruza para baixo, opera-se vendido. Além disso, a estratégia define níveis de stop loss e take profit para controlar o risco.

Princípio da Estratégia

A estratégia utiliza 4 médias móveis de diferentes períodos: 5 dias, 10 dias, 15 dias e 25 dias. Estas 4 médias são denominadas MA1, MA2, MA3 e MA4. MA1 é a mais curta e MA4 a mais longa.

Quando MA1 > MA2 > MA3 > MA4, o preço está em tendência de alta, então opera-se comprado; quando MA1 < MA2 < MA3 < MA4, o preço está em tendência de baixa, então opera-se vendido.

As condições de abertura para compra e venda também exigem a satisfação do filtro de stop loss baseado no ATR, ou seja, o valor do ATR deve ser maior que sua média móvel simples de 40 períodos. Isso evita sinais falsos quando a volatilidade do preço é muito baixa.

Vantagens da Estratégia

A estratégia apresenta as seguintes vantagens:

- Ideia simples e fácil de implementar.

- O uso de múltiplas médias móveis para determinar a direção da tendência é confiável.

- A definição de stop loss e take profit permite controlar eficazmente a perda máxima por operação.

- O filtro de stop loss baseado no ATR evita sinais falsos quando a volatilidade do preço é muito baixa.

Análise de Riscos

A estratégia também apresenta os seguintes riscos:

- Em mercados altamente voláteis, pode gerar sinais falsos.

- A parametrização inadequada (períodos das médias, etc.) pode resultar em desempenho insatisfatório.

- Não considera fundamentos ou notícias importantes que impactam o preço.

Para mitigar esses riscos, pode-se otimizar os parâmetros adequadamente ou adicionar outros filtros para aumentar a estabilidade da estratégia.

Direções de Otimização

As direções de otimização para esta estratégia incluem:

- Testar diferentes combinações de períodos de médias móveis para encontrar os parâmetros ideais.

- Adicionar outros filtros de indicadores técnicos, como MACD, KDJ, para avaliar a confiabilidade dos sinais.

- Adicionar filtro de volume, operando apenas quando o volume aumentar.

- Realizar otimizações detalhadas por ativo, considerando diferenças de parâmetros.

- Incorporar algoritmos de aprendizado de máquina para julgar os sinais.

Resumo

No geral, esta estratégia é uma estratégia de seguimento de tendência relativamente simples, que determina a direção da tendência por meio de médias móveis e define níveis razoáveis de take profit e stop loss para controlar o risco. Ainda há grande espaço para otimização, e ajustes de parâmetros ou adição de filtros podem melhorar ainda mais a estabilidade e a lucratividade da estratégia.

- 1