Estratégia de Seguimento de Tendência com Dupla Média Móvel e Cruzamento StochRSI

Visão Geral

Esta estratégia combina duas médias móveis e o indicador StochRSI para identificar a direção da tendência e os pontos de entrada. Sua principal característica é permitir a entrada no mercado logo no início da tendência, enquanto utiliza as condições de sobrecompra e sobrevenda do StochRSI para filtrar falsos rompimentos.

Princípio da Estratégia

A estratégia utiliza uma média móvel rápida EMA(12) e uma média móvel lenta EMA(25) para construir um sistema de duas médias móveis. Quando a média rápida cruza acima da média lenta, gera um sinal de compra; quando cruza abaixo, gera um sinal de venda, servindo para determinar a direção da tendência principal.

Ao mesmo tempo, a estratégia combina os cruzamentos do StochRSI para identificar melhor o momento de entrada. O StochRSI incorpora os indicadores estocásticos (KDJ) e o RSI. Quando a linha K cruza acima da linha D vindo da região de sobrevenda, gera um sinal de compra; quando a linha K cruza abaixo da linha D vindo da região de sobrecompra, gera um sinal de venda.

A estratégia só abre posição quando ambas as médias móveis geram um sinal e o StochRSI também gera o sinal correspondente. Isso filtra efetivamente parte dos falsos rompimentos, evitando negociações ineficazes.

Análise de Vantagens

A maior vantagem desta estratégia é a capacidade de identificar precocemente a direção da tendência e os potenciais pontos de entrada. O sistema de médias móveis pode gerar sinais no início da tendência, enquanto a adição do StochRSI filtra eficazmente os falsos rompimentos, evitando negociações errôneas.

Além disso, a estratégia combina análise de tendência com julgamento de sobrecompra/sobrevenda, unindo as vantagens do acompanhamento de tendência e das operações de reversão. Seja seguindo a tendência ou comprando nas baixas e vendendo nas altas, a estratégia pode capturar oportunidades de forma abrangente.

Análise de Risco

O principal risco da estratégia reside na defasagem inerente ao sistema de médias móveis. Quando o mercado sofre mudanças bruscas e repentinas, o sistema de duas médias móveis tende a gerar sinais com certo atraso, fazendo com que a estratégia perca o melhor momento de entrada.

Além disso, o indicador StochRSI também pode gerar sinais falsos, provocando negociações desnecessárias. Especialmente em períodos de mercado lateral, as linhas K e D podem se cruzar com frequência, aumentando o risco de operações ineficazes.

Direções de Otimização

A otimização da estratégia concentra-se principalmente nos seguintes aspectos:

-

Ajustar os parâmetros das duas médias móveis, utilizando períodos mais adequados para capturar tendências;

-

Otimizar os parâmetros do StochRSI, estabelecendo critérios mais razoáveis para sobrecompra e sobrevenda;

-

Aumentar o volume de negociação ou ajustar os níveis de stop-loss e take-profit para buscar maior rentabilidade;

-

Combinar outros indicadores como filtros adicionais para reduzir ainda mais sinais inválidos.

Conclusão

No geral, esta estratégia é muito adequada para capturar tendências de médio e longo prazo, oferecendo grande potencial de lucro no início da tendência. Combinada com o StochRSI como julgamento auxiliar, ela filtra efetivamente sinais enganosos, evitando perdas desnecessárias. Com a otimização de parâmetros e melhorias na gestão de risco, esta estratégia pode se tornar uma ferramenta poderosa para obter ganhos estáveis.

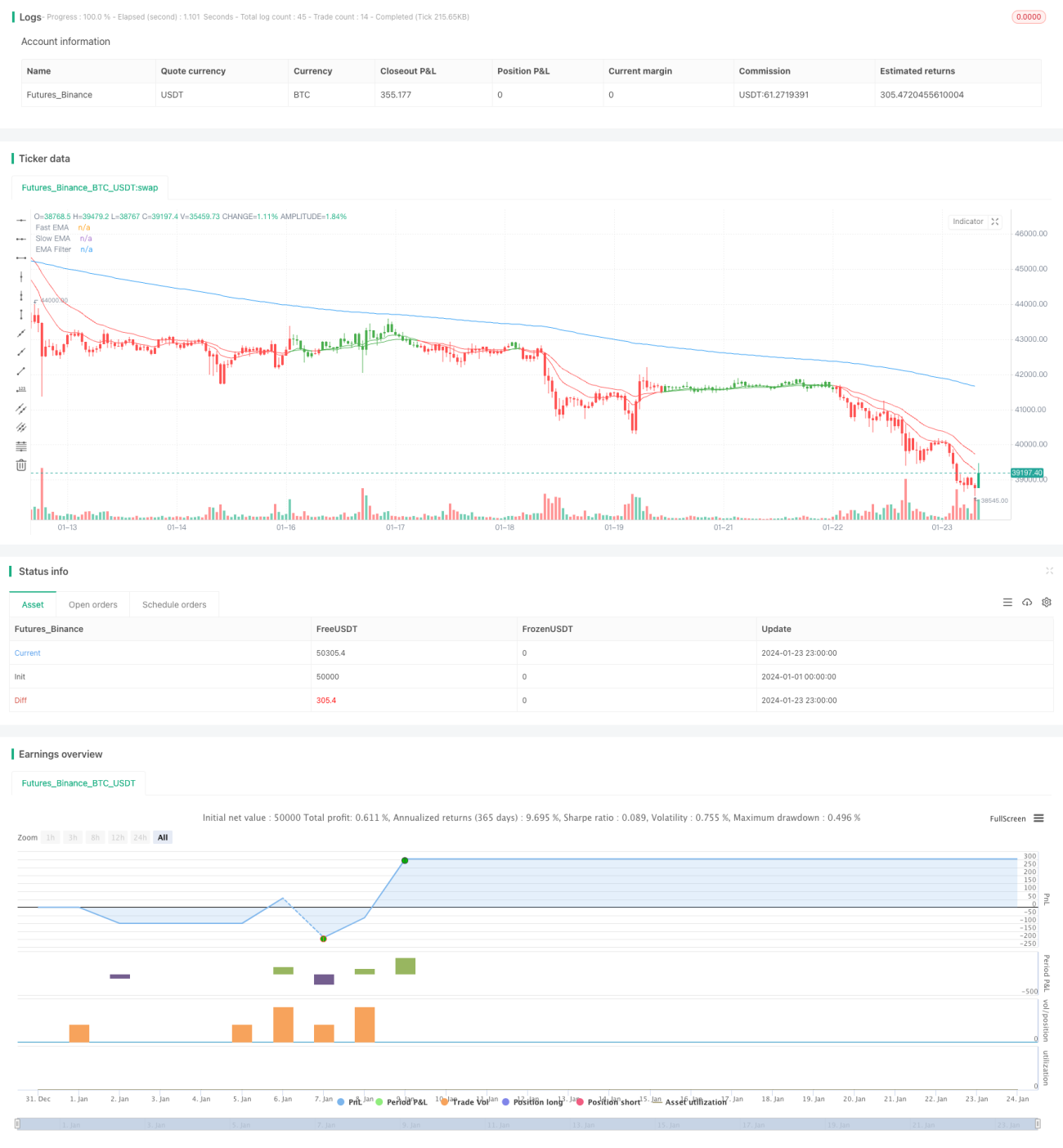

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © btc_charlie / @TheParagonGrp

//@version=5- 1