Estratégia de Negociação de Oscilação com Suporte e Resistência

Visão Geral

Esta estratégia combina a estratégia de cruzamento de RSI e indicador estocástico, juntamente com uma estratégia de otimização de slippage de fechamento, para obter um controle preciso da lógica de negociação e um stop loss/take profit preciso. Ao mesmo tempo, através da introdução de otimização de sinais, é possível controlar melhor a tendência e gerenciar o capital de forma racional.

Princípio da Estratégia

- O indicador RSI determina zonas de sobrecompra e sobrevenda, combinado com o cruzamento de ouro/morte dos valores K e D do indicador estocástico para formar sinais de negociação.

- Introdução do reconhecimento de fractal dos candles para auxiliar na determinação de sinais de tendência e evitar negociações errôneas.

- A média móvel SMA ajuda a determinar a direção da tendência. Quando a média de curto prazo cruza para cima a média de longo prazo, é um sinal de alta.

- Estratégia de slippage de fechamento: define os preços de stop loss e take profit com base na faixa de flutuação das máximas e mínimas.

Análise de Vantagens

- Parâmetros otimizados do RSI determinam bem as zonas de sobrecompra e sobrevenda, evitando negociações errôneas.

- Parâmetros otimizados do STO (indicador estocástico) com ajuste do parâmetro de suavidade podem filtrar ruídos e melhorar a qualidade dos sinais.

- Introdução da análise técnica Heikin-Ashi para identificar mudanças na direção do corpo do candle, garantindo a precisão dos sinais de negociação.

- A média móvel SMA auxilia na determinação da direção macro da tendência, evitando negociações contra a tendência.

- Combinado com a estratégia de slippage de stop loss/take profit, maximiza o lucro de cada negociação.

Análise de Riscos

- Quando o mercado geral está em queda contínua, o capital enfrenta riscos maiores.

- A frequência de negociação pode ser muito alta, aumentando os custos de transação e os custos de slippage.

- O indicador RSI pode gerar sinais falsos facilmente, devendo ser filtrado por outros indicadores.

Otimização da Estratégia

- Ajustar os parâmetros do RSI para otimizar a determinação de sobrecompra/sobrevenda.

- Ajustar os parâmetros do STO (suavidade e período) para melhorar a qualidade dos sinais.

- Ajustar os períodos das médias móveis para otimizar a determinação da tendência.

- Introduzir mais indicadores técnicos para melhorar a precisão dos sinais.

- Otimizar a proporção de stop loss/take profit para reduzir o risco de cada negociação.

Resumo

Esta estratégia integra as vantagens de múltiplos indicadores técnicos populares. Através da otimização de parâmetros e do aprimoramento das regras, atinge um equilíbrio entre a qualidade dos sinais de negociação e o stop loss/take profit. Possui certa universalidade e capacidade de lucro estável. Através de otimização contínua, é possível melhorar ainda mais a taxa de acerto e a rentabilidade.

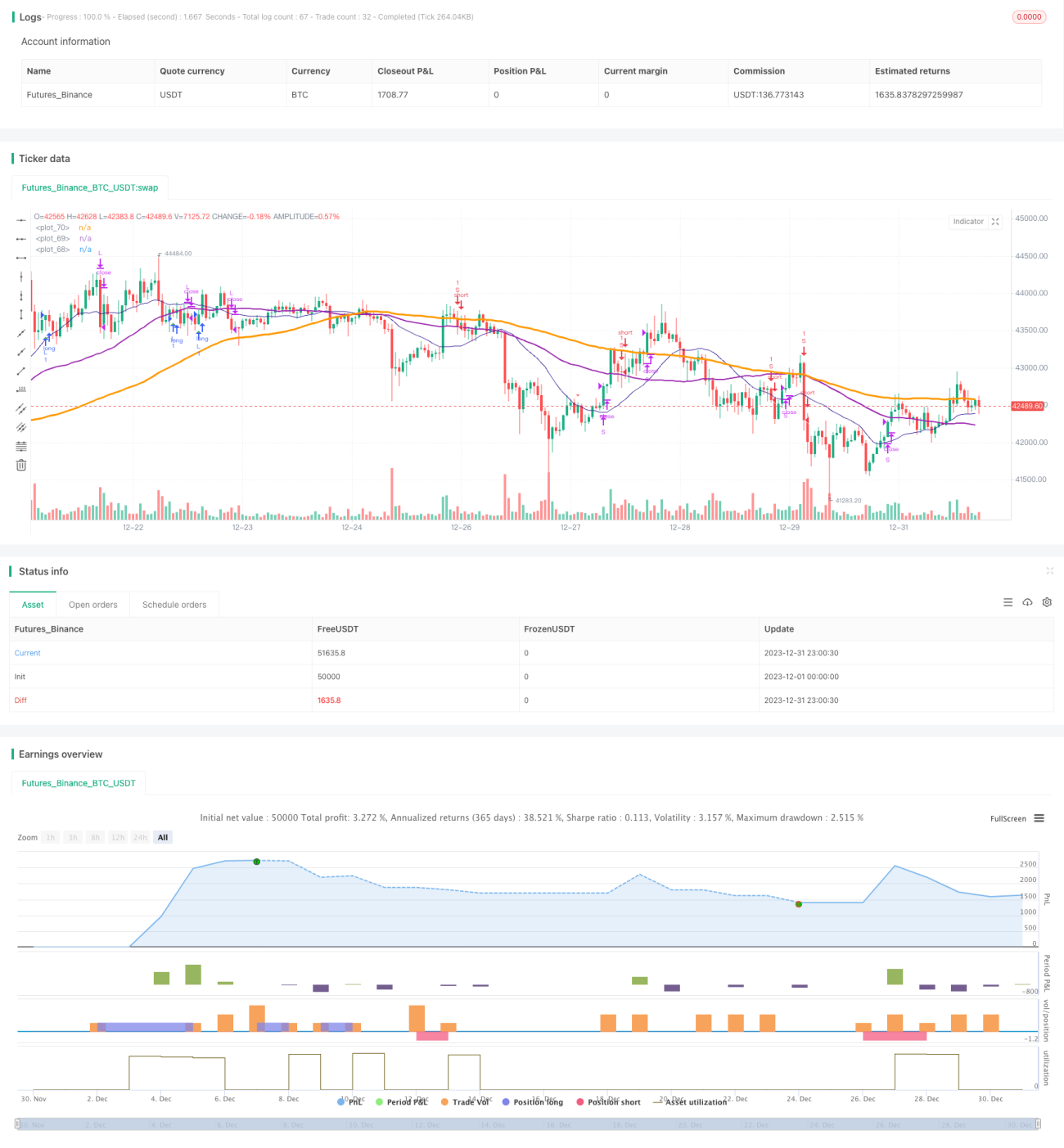

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)- 1