Estratégia de Trading com Stop Loss Móvel Stochastic Supertrend

Visão Geral

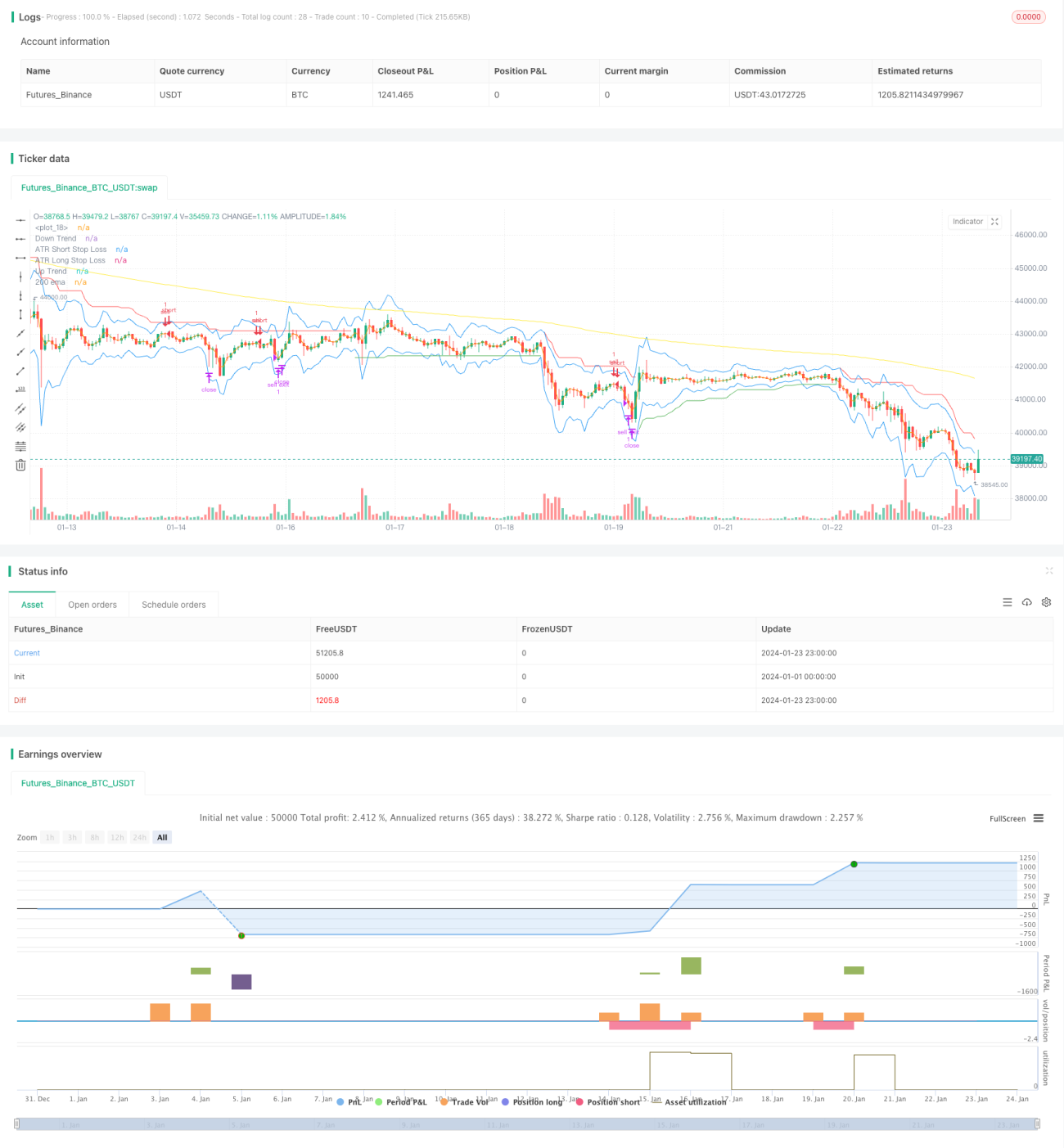

Esta é uma estratégia de trailing stop que combina múltiplos indicadores técnicos. Utiliza principalmente os indicadores Supertrend, Estocástico, média móvel de 200 dias e stop loss por ATR para identificar sinais de negociação e definir níveis de stop. A estratégia é adequada para negociação de tendências de médio a longo prazo e pode controlar o risco de forma eficaz.

Princípio da Estratégia

Quando a linha K do Estocástico cai de uma zona de sobrecompra, o Supertrend indica tendência de alta e o preço ultrapassa a média móvel de 200 dias, abre-se uma posição comprada. Quando a linha K do Estocástico sobe de uma zona de sobrevenda, o Supertrend indica tendência de baixa e o preço rompe abaixo da média móvel de 200 dias, abre-se uma posição vendida. Após a entrada, o stop loss é definido dinamicamente usando o indicador ATR.

Especificamente, quando o valor K do Estocástico cruza acima de 80, considera-se um sinal de sobrecompra; quando o valor K cruza abaixo de 20, considera-se um sinal de sobrevenda. O indicador Supertrend determina a direção da tendência de preço: quando aponta para cima, o preço está em tendência de alta; quando aponta para baixo, o preço está em tendência de baixa. O indicador ATR é usado para calcular a amplitude real.

Condição para disparar sinal de compra: a linha K do Estocástico cai da zona de sobrecompra (menor que 80), o Supertrend indica alta e o preço está acima da média móvel de 200 dias.

Condição para disparar sinal de venda: a linha K do Estocástico sobe da zona de sobrevenda (maior que 20), o Supertrend indica baixa e o preço está abaixo da média móvel de 200 dias.

Após a entrada, define-se um stop loss por ATR para acompanhar a volatilidade do preço e controlar o risco. O stop para posição comprada é o preço mínimo menos o valor do ATR multiplicado por um coeficiente; o stop para posição vendida é o preço máximo mais o valor do ATR multiplicado por um coeficiente.

Vantagens da Estratégia

Esta estratégia combina múltiplos indicadores para determinar a direção da tendência e o momento de entrada, filtrando eficazmente sinais falsos. Além disso, utiliza um trailing stop dinâmico baseado em ATR, que permite controlar o risco de acordo com a volatilidade do mercado, preservando ao máximo o capital.

Em comparação com estratégias de acompanhamento de tendência que usam apenas médias móveis simples, esta abordagem consegue capturar melhor os pontos de reversão. Em comparação com métodos de stop loss fixos, o stop dinâmico por ATR oferece maior flexibilidade. Assim, a estratégia apresenta uma boa relação risco-retorno.

Riscos da Estratégia

A estratégia depende principalmente de indicadores; se estes emitirem sinais incorretos, pode levar a perdas devido a operações na direção oposta. Além disso, em mercados laterais, o stop loss pode ser acionado com frequência, gerando perdas.

Embora o stop por ATR possa ajustar o nível de stop de acordo com a volatilidade, ele não elimina completamente a possibilidade de o stop ser violado. Em caso de gaps de preço, a ordem de stop pode ser acionada diretamente.

Otimização da Estratégia

Esta estratégia pode ser otimizada nas seguintes dimensões:

-

Ajustar os parâmetros dos indicadores para melhorar a precisão dos sinais de compra e venda. Por exemplo, testar diferentes parâmetros para o Estocástico ou ajustar o período do ATR e o multiplicador do Supertrend.

-

Testar a eficácia de outros métodos de stop loss. Por exemplo, experimentar algoritmos de stop inteligente adaptativos mais flexíveis que o ATR, ou considerar um stop que acompanhe um trailing stop móvel.

-

Adicionar filtros adicionais para entrar apenas em condições mais confiáveis. Por exemplo, incluir indicadores de volume ou energia para evitar entradas equivocadas quando o volume é insuficiente.

-

Otimizar a gestão de capital, como ajustar dinamicamente o tamanho da posição.

Resumo

A estratégia de trailing stop com Estocástico e Supertrend combina múltiplos indicadores para determinar a direção da tendência e utiliza o trailing stop inteligente por ATR para controlar o risco. Esta estratégia filtra eficazmente o ruído do mercado e oferece uma boa relação risco-retorno. Podemos otimizar continuamente esta estratégia ajustando parâmetros, modificando o método de stop loss e adicionando filtros, de modo a adaptá-la a ambientes de mercado mais complexos.

- 1