Estratégia de trading de cruzamento duplo de médias móveis golden cross

Visão Geral

A estratégia de cruzamento de médias móveis (golden cross) utiliza o cruzamento de duas médias móveis de períodos diferentes como sinais de compra e venda. Especificamente, quando a média móvel de curto prazo cruza acima da média móvel de longo prazo, gera-se um sinal de cruz dourada (golden cross), indicando que o mercado se torna bullish; quando a média móvel de curto prazo cruza abaixo da média móvel de longo prazo, gera-se um sinal de cruz da morte (death cross), indicando que o mercado se torna bearish.

Princípio da Estratégia

A estratégia baseia-se em dois princípios:

-

As médias móveis refletem a tendência e a força do mercado. A média móvel de curto prazo captura os movimentos recentes e pontos de inflexão; a média móvel de longo prazo representa a tendência principal do mercado.

-

Quando a média móvel de curto prazo forma um cruz dourada com a média móvel de longo prazo, indica que a força do curto prazo supera a força da tendência de longo prazo, sendo provável o início de uma nova tendência de alta. Quando forma um cruz da morte, indica que a tendência de baixa de longo prazo predomina, sendo provável a continuação da queda.

Especificamente, a estratégia define médias móveis simples de 13 e 30 períodos, gerando sinais de negociação em seus cruzamentos. O princípio do cruzamento é o seguinte:

-

Quando a média móvel de curto prazo cruza acima da média móvel de longo prazo, gera-se um sinal de cruz dourada, indicando uma oportunidade de compra (long). Nesse momento, a entrada é feita avaliando a solidez da tendência: se o preço mantiver uma alta por um certo número de períodos, há confiança de que a tendência atual é de alta, então entra-se em posição comprada.

-

Quando a média móvel de curto prazo cruza abaixo da média móvel de longo prazo, gera-se um sinal de cruz da morte, indicando uma oportunidade de venda (short). Nesse momento, a entrada é feita avaliando a solidez da tendência: se o preço mantiver uma queda por um certo número de períodos, há confiança de que a tendência atual é de baixa, então entra-se em posição vendida.

-

A inclinação das médias móveis é usada para avaliar a força do sinal de cruzamento. Somente quando a diferença entre as inclinações da média de curto prazo e da média de longo prazo ultrapassa um certo limiar, considera-se que o sinal de cruzamento é suficientemente forte para justificar a entrada. Isso suprime a interferência de sinais falsos comuns.

-

O stop loss é definido em 20% e o take profit em 100%.

Análise de Vantagens

A estratégia de cruzamento de médias móveis apresenta as seguintes vantagens:

-

Conceito claro e simples, fácil de entender e implementar, adequado para iniciantes.

-

Utiliza a característica de suavização dos preços, oferecendo certo efeito de eliminação de ruído, evitando ser enganado por flutuações de curto prazo.

-

Avalia a solidez da tendência, evitando entrar mecanicamente em posições compradas ou vendidas, combinando com o julgamento do mercado geral.

-

Introduz o fator de momentum da inclinação das médias móveis, tornando os sinais mais confiáveis.

-

Otimização backtest simples, exigindo apenas o ajuste de alguns parâmetros-chave, como os períodos das médias móveis e o tempo de solidez da tendência.

Análise de Riscos

A estratégia também apresenta os seguintes riscos:

-

O cruzamento de médias móveis é, por natureza, um sinal atrasado, não sendo capaz de prever perfeitamente os pontos de inflexão, havendo um certo grau de latência. Deve-se encurtar adequadamente os períodos das médias móveis ou combiná-las com fatores que possam prever pontos de inflexão.

-

Sistemas de negociação mecânicos tendem a atuar simultaneamente, agravando os movimentos do mercado, podendo tornar o stop loss ou take profit ineficazes. Deve-se configurar stop loss e take profit escalonados, ou intervir manualmente quando adequado.

-

Não lida bem com mercados laterais (oscilantes). Deve-se evitar ativos que oscilem repetidamente nesses períodos, escolhendo aqueles com direções claras para negociar.

-

A definição adequada da janela de tempo para avaliar a solidez da tendência tem grande impacto nos resultados, exigindo testes repetidos para determinar o valor ideal.

Direções de Otimização

A estratégia de cruzamento de médias móveis também pode ser otimizada nos seguintes aspectos:

-

Adicionar indicadores para avaliar a tendência de grande escala, evitando operações contrárias à tendência. Por exemplo, incluir a comparação com a posição em relação à média semanal ou mensal.

-

Adicionar validação do volume de negociação, gerando sinais apenas quando o volume aumenta, evitando sinais falsos.

-

Otimizar os parâmetros das médias móveis, buscando a melhor combinação de períodos. Pode-se tentar parâmetros adaptativos para as médias móveis.

-

Combinar com indicadores tradicionais, como MACD, KDJ, etc., para auxiliar no julgamento, aumentando a precisão dos sinais.

-

Configurar stop loss e take profit escalonados para melhor controlar o risco.

Resumo

Em geral, a estratégia de cruzamento de médias móveis é uma abordagem muito intuitiva e explicável. Ela combina a característica de suavização das médias móveis com a capacidade simples de identificação de tendências por meio de cruzamentos. Ao mesmo tempo, realiza alguma validação dos sinais, evitando seguir cegamente o movimento, o que aumenta sua praticidade e estabilidade. Além das melhorias mencionadas neste texto, a estratégia ainda possui grande espaço para otimização, merecendo estudo aprofundado.

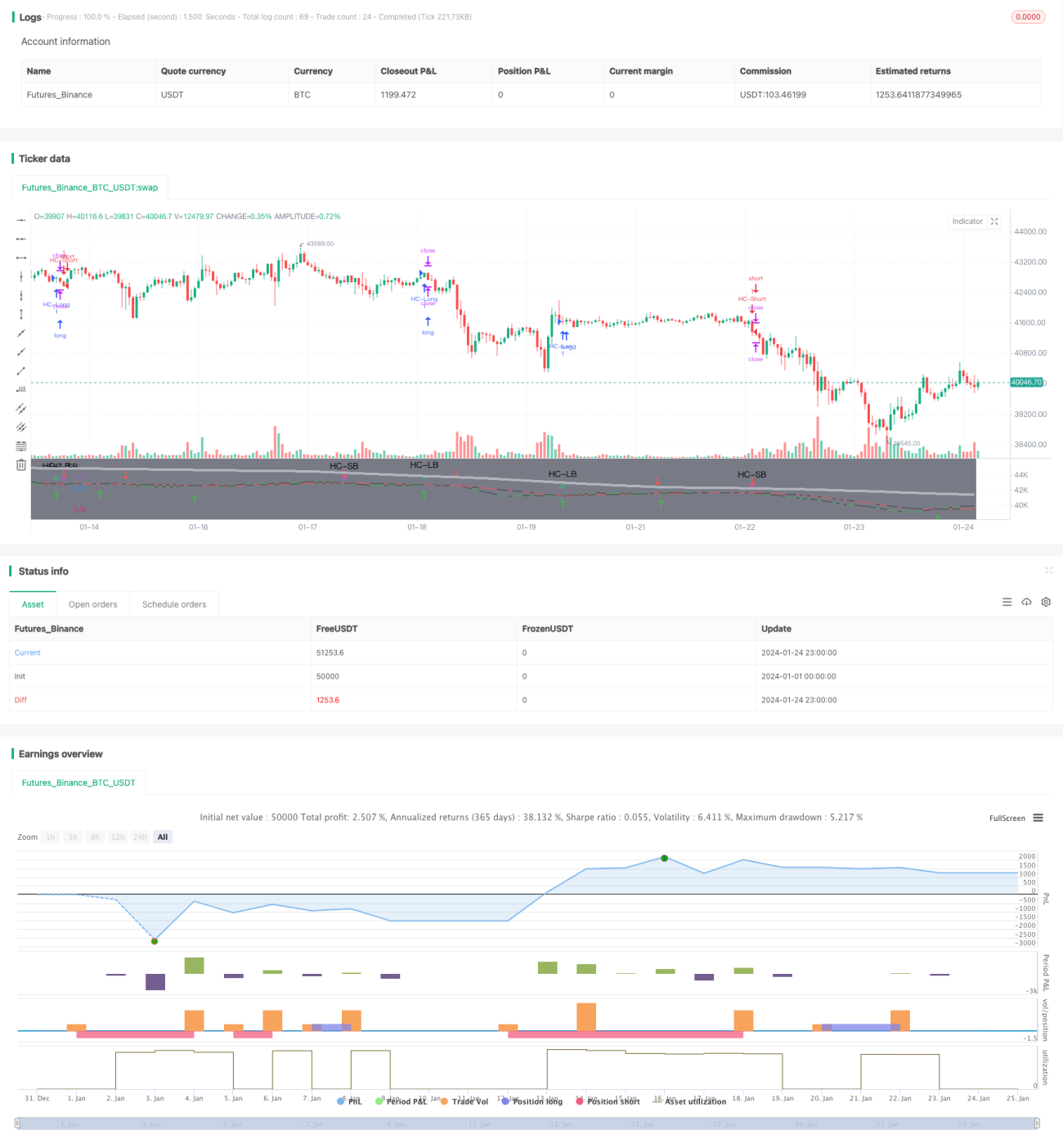

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MakeMoneyCoESTB2020- 1