Estratégia de Tendência Progressiva BB KC

Visão Geral

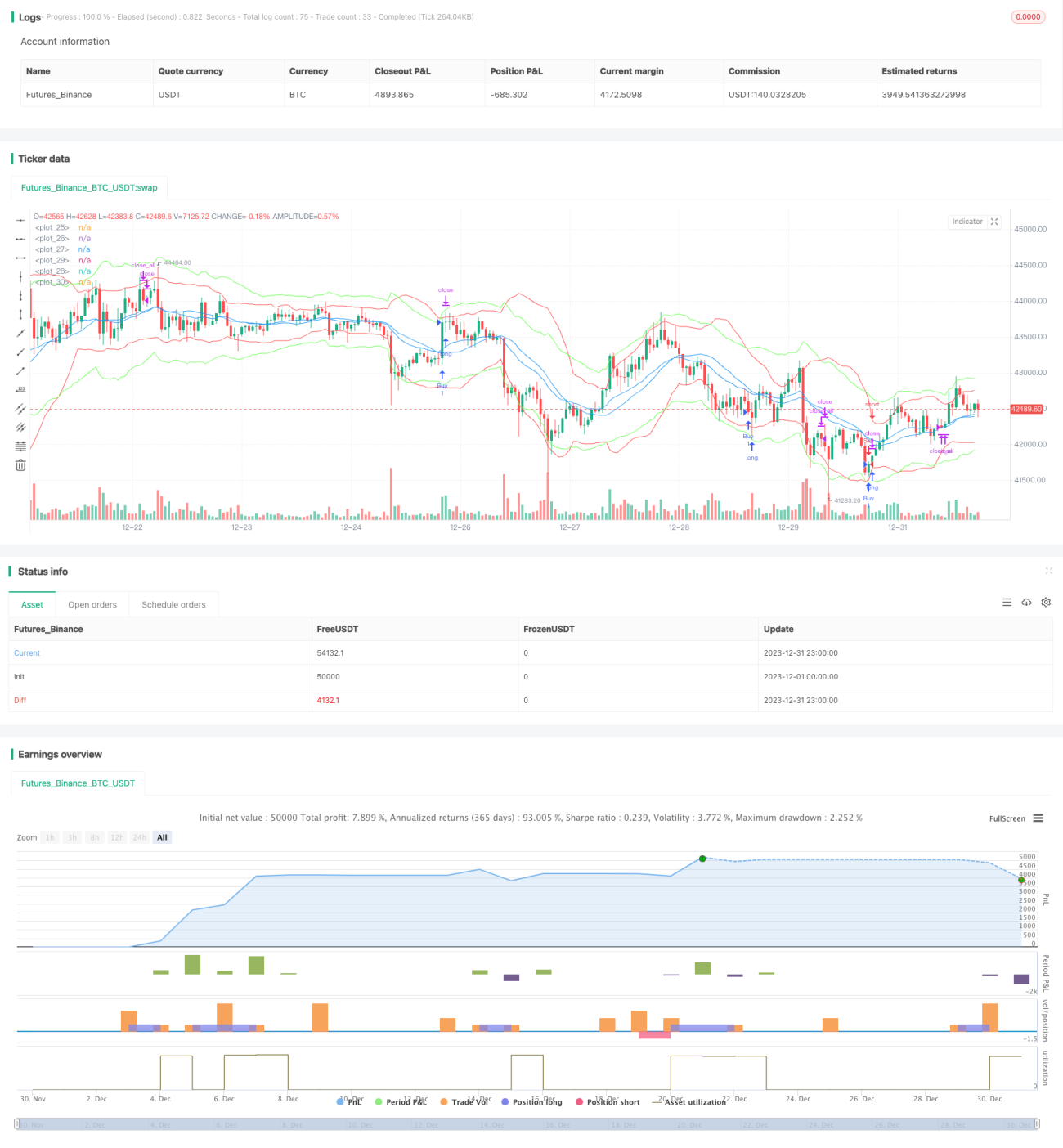

Esta estratégia utiliza a combinação das Bandas de Bollinger e do Canal de Keltner para identificar tendências de mercado. As Bandas de Bollinger são uma ferramenta de análise técnica que delimita canais com base na amplitude de flutuação dos preços. O Canal de Keltner é um indicador técnico que combina a volatilidade dos preços com a tendência para identificar suportes ou resistências. A estratégia integra as vantagens de ambos os indicadores, buscando oportunidades de compra e venda ao identificar o cruzamento dourado entre as Bandas de Bollinger e o Canal de Keltner, e validando os sinais com o volume de negociação. Isso permite identificar efetivamente o início das tendências e minimizar ao máximo os sinais falsos.

Princípio da Estratégia

- Calcular a banda média, superior e inferior das Bandas de Bollinger para um período de 20, com a largura definida por 2 desvios padrão.

- Calcular a banda média, superior e inferior do Canal de Keltner para um período de 20, com a largura definida por 2,2 vezes o True Range médio.

- Quando a banda superior do Canal de Keltner cruza acima da banda superior das Bandas de Bollinger e o volume de negociação é maior que a média de volume dos últimos 10 períodos, comprar (posição longa).

- Quando a banda inferior do Canal de Keltner cruza abaixo da banda inferior das Bandas de Bollinger e o volume de negociação é maior que a média de volume dos últimos 10 períodos, vender (posição curta).

- Se a posição não for encerrada em 20 barras após a abertura, forçar o fechamento com stop gain ou stop loss.

- Após a compra, definir stop loss de 1,5%; após a venda, definir stop loss de -1,5%. Após a compra, definir trailing stop de 2%; após a venda, definir trailing stop de -2%.

A estratégia depende principalmente das Bandas de Bollinger para avaliar a amplitude e a força das flutuações, utilizando o Canal de Keltner como validação auxiliar. A combinação de dois indicadores com parâmetros diferentes, mas de natureza semelhante, melhora a precisão dos sinais. A introdução do volume também reduz efetivamente os sinais falsos.

Análise de Vantagens

- Utiliza as vantagens das Bandas de Bollinger e do Canal de Keltner, aumentando a precisão dos sinais de negociação.

- Combinado com o indicador de volume, reduz efetivamente os sinais falsos gerados por frequentes toques nas bandas do mercado.

- Mecanismos de stop loss e trailing stop permitem um controle eficaz do risco.

- O fechamento forçado após sinais inválidos permite rápida saída com stop loss ou stop gain.

Análise de Riscos

- Tanto as Bandas de Bollinger quanto o Canal de Keltner são baseados em médias móveis combinadas com volatilidade, o que pode gerar sinais falsos em mercados laterais.

- Ausência de mecanismo de juros compostos; múltiplos rebaixamentos podem levar a perdas excessivas.

- Sinais de reversão são comuns; o ajuste de parâmetros pode fazer com que oportunidades de tendência sejam perdidas.

Pode-se ampliar moderadamente a margem de stop loss ou adicionar indicadores auxiliares como MACD para filtrar sinais, reduzindo os riscos de sinais falsos.

Direções de Otimização

- Testar diferentes parâmetros (como comprimento da média móvel, múltiplos do desvio padrão, etc.) para ver seu impacto na rentabilidade da estratégia.

- Adicionar outros indicadores para confirmar os sinais, como o indicador KDJ ou MACD como suporte.

- Utilizar métodos de aprendizado de máquina para otimizar automaticamente os parâmetros.

Resumo

Esta estratégia combina as Bandas de Bollinger e o Canal de Keltner para identificar tendências de mercado, complementada pelo volume de negociação para validar os sinais. É possível fortalecer ainda mais a estratégia por meio da otimização de parâmetros e da adição de outros indicadores técnicos, tornando-a adaptável a uma gama mais ampla de condições de mercado. A estratégia tem boa viabilidade geral e é uma das estratégias de trading quantitativo fáceis de compreender e ajustar.

- 1