Estratégia de Seguimento de Tendência com Breakout do Canal de Donchian

Visão Geral

A estratégia de rompimento do canal de Donchian é uma estratégia de acompanhamento de tendência que forma um canal de preços calculando as máximas e mínimas em um determinado período, usando os limites do canal como sinais de compra e venda. Quando o preço rompe a banda superior, abre-se posição vendida; quando rompe a banda inferior, abre-se posição comprada. Essa estratégia é adequada para negociação de criptomoedas de alta volatilidade.

Princípio da Estratégia

A estratégia utiliza o indicador de canal de Donchian para identificar a tendência de preços e calcular pontos de entrada e saída. O canal de Donchian é composto por uma banda superior, uma banda inferior e uma banda média. A banda superior é a máxima em um determinado período, a banda inferior é a mínima, e a banda média é a média dos preços.

Os períodos de entrada e saída podem ser configurados independentemente. Quando o preço rompe a banda inferior para cima, abre-se posição comprada; quando rompe a banda superior para baixo, abre-se posição vendida. O ponto de saída ocorre quando o preço toca novamente a respectiva banda. Também é possível usar a banda média como linha de stop loss.

Além disso, a estratégia inclui pontos de take profit. Para posições compradas, o preço de take profit é o preço de entrada multiplicado por (1 + percentual de take profit); para posições vendidas, o oposto. Ativar esse recurso permite fixar lucros e evitar que as perdas aumentem.

No geral, a estratégia identifica a tendência enquanto garante espaço suficiente para definir stop loss e take profit. Isso a torna particularmente adequada para ativos de alta volatilidade, como criptomoedas.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Julgamento claro da estratégia, com geração de sinais simples e confiável.

- O indicador de canal de Donchian é insensível a oscilações de preço, facilitando a captura de tendências.

- Parâmetros do canal personalizáveis, adaptando-se a diferentes ativos e períodos.

- Função integrada de stop loss e take profit, permitindo controle eficaz de risco.

- Adequada para ativos de alta volatilidade, como criptomoedas, com grande potencial de lucro.

Análise de Riscos

A estratégia também apresenta os seguintes riscos:

- Apesar da função de stop loss, não é possível evitar completamente riscos de movimentos extremos de preço.

- Parâmetros mal configurados podem levar a negociações excessivamente frequentes, aumentando custos de transação e risco de slippage.

- A estratégia é insensível a oscilações de preço, podendo perder algumas oportunidades de negociação.

Para controlar esses riscos, recomenda-se:

- Reduzir adequadamente o capital alocado por operação, diversificar os ativos negociados e controlar o risco geral.

- Otimizar parâmetros, buscando a melhor combinação. Pode-se tentar métodos como aprendizado de máquina para otimização automática.

- Combinar indicadores adicionais para avaliar a confiabilidade dos sinais de rompimento, evitando negociações falsas.

Direções de Otimização

A estratégia pode ser otimizada nas seguintes dimensões:

- Testar e otimizar mais combinações de parâmetros para encontrar os melhores. Os principais parâmetros incluem período do canal, percentual de take profit, permissão de operações compradas e vendidas, etc.

- Adicionar modelos de aprendizado de máquina para identificar automaticamente parâmetros ótimos. Pode-se usar métodos como aprendizado por reforço.

- Combinar outros indicadores para avaliar tendências e confiabilidade dos sinais, como médias móveis, volume, etc.

- Desenvolver estratégias de stop loss, como trailing stop, Chandelier Exit, etc., para controlar melhor o risco.

- Expandir para mais ativos, buscando aqueles que melhor se adequam à estratégia.

Resumo

A estratégia de rompimento do canal de Donchian é, no geral, uma estratégia de acompanhamento de tendência com julgamento claro e risco controlável. Ela é especialmente adequada para ativos de alta volatilidade, como criptomoedas, com grande potencial de lucro. Ao mesmo tempo, a estratégia possui espaço para otimização de parâmetros e possibilidade de combinação com outros indicadores, que são direções futuras de expansão. Através de otimização e inovação contínuas, essa estratégia tem potencial para se tornar uma importante opção para negociação algorítmica de criptomoedas.

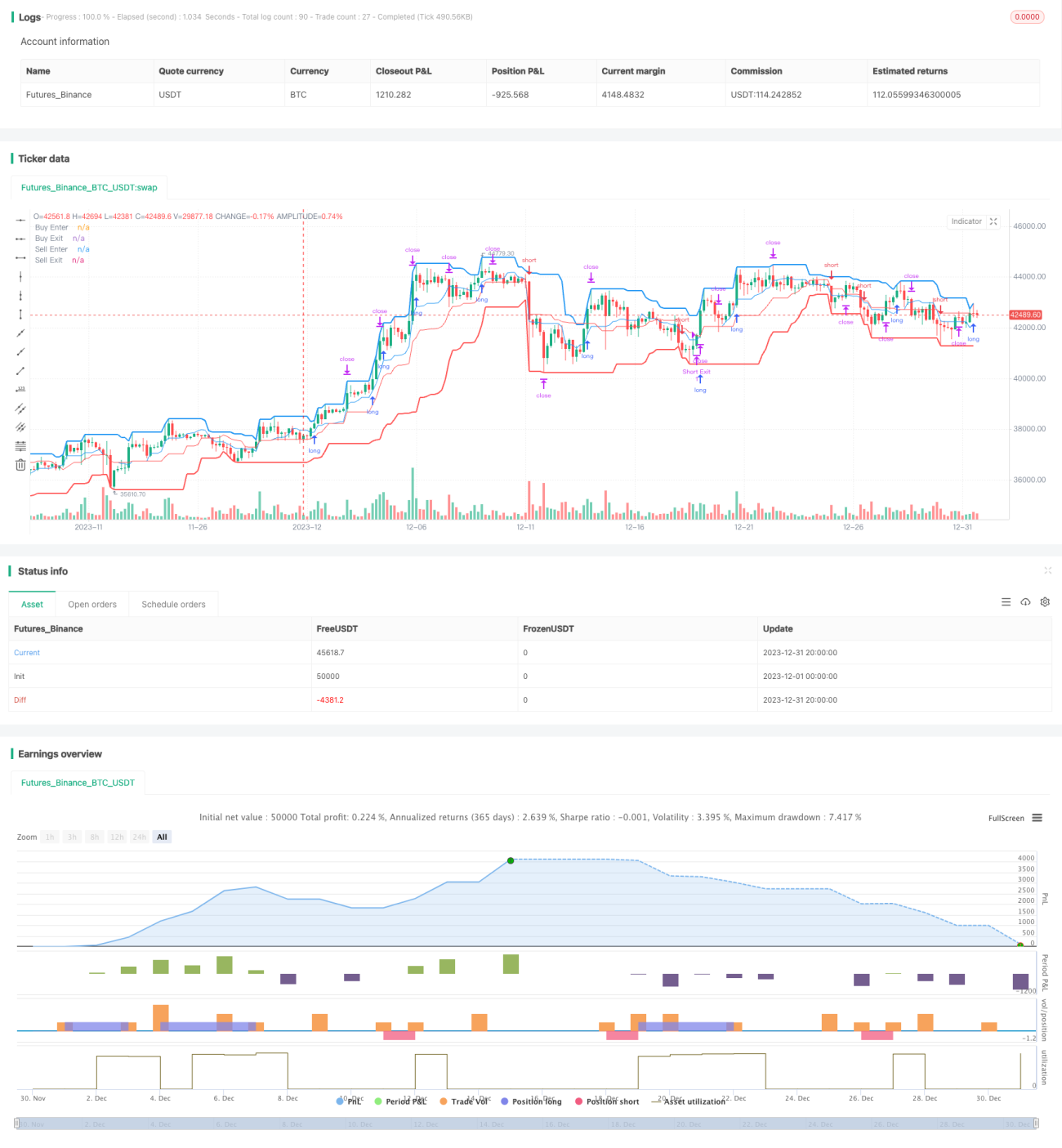

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © algotradingcc

// Strategy testing and optimisation for free trading bot

- 1