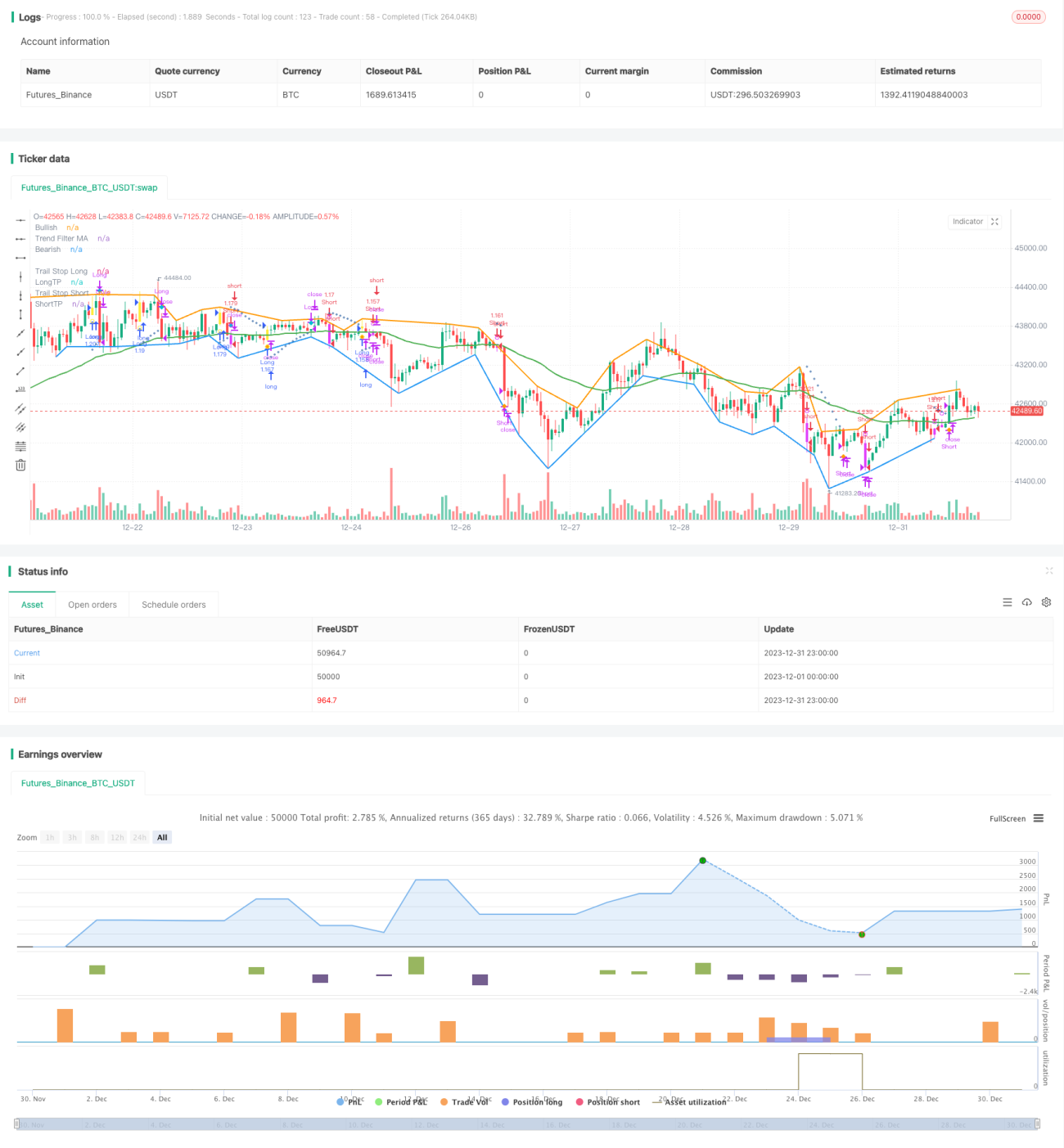

Estratégia de negociação do indicador MACD de múltiplos períodos

Visão Geral

Esta estratégia baseia-se no clássico indicador MACD, combinando simultaneamente múltiplos auxílios de julgamento, como indicadores de tendência, métodos de stop loss e métodos de take profit, formando uma estratégia de negociação de acompanhamento de tendência relativamente completa. Pode ser utilizada tanto para criptomoedas quanto para negociação forex e ações.

Princípios da Estratégia

-

Julgamento do indicador MACD

- A diferença entre a EMA do período FASTLENGTH e a EMA do período SLOWLENGTH forma as barras do MACD

- A EMA do período MACDLENGTH suaviza as barras do MACD formando a linha MACD

- A quebra da linha zero pelas barras do MACD gera sinais de compra/venda

-

Julgamento de tendência

- ADX: Indicador de Movimento Direcional Médio, avalia se existe uma tendência

- MA: Média Móvel, preço acima/abaixo da MA forma tendência

- SAR: Parabólico SAR, movimento do SAR acima/abaixo do preço indica tendência

-

Métodos de stop loss

- Stop loss percentual baseado no ATR: define stop loss percentual com base no fator ATR

- Stop loss por SAR: utiliza o parabólico como stop loss após a entrada

-

Métodos de take profit

- Distância fixa de take profit baseada no ATR: define distância fixa de take profit com base no fator ATR

- Take profit percentual: define distância percentual de take profit

-

Stop loss por tempo

- Pode-se definir stop loss após um número específico de barras

Análise de Vantagens

-

Múltiplos auxílios de julgamento

- Combinando julgamento de tendência e suporte/resistência, reduz sinais falsos

- Stop loss por ATR/SAR, controle de risco mais abrangente

-

Configuração flexível

- Possibilidade de escolher se deseja usar filtro de tendência

- Possibilidade de escolher stop loss por ATR ou SAR

- Possibilidade de escolher take profit por ATR ou padrão

- Parâmetros configuráveis de forma flexível

-

Fornece análise de divergência

- Exibe divergências históricas positivas e negativas

- Fornece dicas textuais

-

Facilidade para otimização e ajustes

- Estratégia incorpora grande quantidade de parâmetros configuráveis

- Permite testar facilmente diferentes combinações de variáveis

Análise de Riscos

-

Parâmetros inadequados podem aumentar as perdas

- Parâmetros ATR ou SAR mal configurados podem causar stop loss prematuro

- Proporção de take profit muito grande pode resultar em take profit precoce

-

Risco de falha no julgamento de tendência

- Parâmetros inadequados dos indicadores de tendência podem levar a julgamentos errados

- Eventos imprevistos podem comprometer a eficácia do julgamento de tendência

-

Risco de stop loss por tempo

- Definir stop loss fixo por tempo apresenta risco de perda

Direções de Otimização

- Ajustar parâmetros do ATR e SAR para tornar o stop loss mais suave

- Testar diferentes períodos de MA para otimizar o julgamento de tendência

- Testar ajustes na proporção de take profit para otimizar a taxa de retorno

- Combinar indicadores de volatilidade para otimizar parâmetros

Resumo

Esta estratégia considera múltiplos aspectos como julgamento de tendência, stop loss/take profit, identificação de divergências, formando uma estratégia de negociação de criptomoedas relativamente abrangente. Ela combina as vantagens do indicador MACD, adiciona filtro de tendência para evitar negociações equivocadas; insere stop loss por ATR/SAR para melhor controle de risco; a identificação de divergências fornece referência adicional. A presença de múltiplos parâmetros configuráveis permite testar e otimizar facilmente. No geral, esta estratégia pode servir como um bom exemplo para pesquisa de estratégias de criptomoedas.

- 1