Estratégia de Squeeze de Momentum do Urso Preguiçoso

Visão Geral

A Estratégia de Squeeze de Momentum do Urso Preguiçoso é uma estratégia de trading quantitativa que combina Bandas de Bollinger, Canais de Keltner e indicadores de momentum. Ela utiliza as Bandas de Bollinger e os Canais de Keltner para determinar se o mercado está em um estado de compressão (squeeze), e então combina com o indicador de momentum para gerar sinais de negociação.

A principal vantagem dessa estratégia é a capacidade de identificar automaticamente o início de movimentos direcionais (trending) e determinar o momento de entrada com o auxílio do indicador de momentum. No entanto, também apresenta certos riscos, exigindo otimização de parâmetros para diferentes ativos.

Princípios da Estratégia

A Estratégia de Squeeze de Momentum do Urso Preguiçoso baseia-se nos três indicadores a seguir:

- Bandas de Bollinger: compostas por uma média móvel central, uma banda superior e uma banda inferior.

- Canais de Keltner: compostos por uma média móvel central, uma banda superior e uma banda inferior.

- Indicador de Momentum: diferença entre o preço atual e o preço de N períodos atrás.

Quando a banda superior das Bandas de Bollinger está abaixo da banda superior dos Canais de Keltner, e a banda inferior das Bandas de Bollinger está acima da banda inferior dos Canais de Keltner, consideramos que o mercado está em estado de compressão. Isso geralmente indica que um movimento direcional está prestes a começar.

Para determinar o momento de entrada, utilizamos o indicador de momentum para avaliar a velocidade da variação de preço. Quando o momentum rompe acima de sua média, gera-se um sinal de compra; quando o momentum rompe abaixo de sua média, gera-se um sinal de venda.

Análise das Vantagens da Estratégia

As principais vantagens da Estratégia de Squeeze de Momentum do Urso Preguiçoso são:

- Capacidade de identificar automaticamente o início de uma tendência, permitindo entrada precoce.

- Combinação de múltiplos indicadores para evitar sinais falsos.

- Abrange tanto trading de tendência quanto de reversão.

- Parâmetros personalizáveis para otimização em diferentes ativos.

Análise de Risco

A Estratégia de Squeeze de Momentum do Urso Preguiçoso também apresenta alguns riscos:

- As Bandas de Bollinger e os Canais de Keltner podem gerar sinais falsos com frequência.

- O indicador de momentum pode ser instável, podendo perder o ponto ideal de entrada.

- Requer otimização de parâmetros; caso contrário, o desempenho pode ser insatisfatório.

- O resultado tem alta correlação com o ativo negociado.

Para reduzir riscos, recomenda-se otimizar os períodos das Bandas de Bollinger e dos Canais de Keltner, ajustar os stops, escolher ativos com boa liquidez e utilizar outros indicadores para confirmação.

Direções de Otimização da Estratégia

Para aprimorar ainda mais a eficácia da Estratégia de Squeeze de Momentum do Urso Preguiçoso, as principais direções de otimização incluem:

- Testar combinações de parâmetros em diferentes ativos e timeframes.

- Otimizar os períodos das Bandas de Bollinger e dos Canais de Keltner.

- Otimizar o período do indicador de momentum.

- Desenvolver estratégias de stop-loss e take-profit distintas para posições compradas e vendidas.

- Adicionar outros indicadores para validação dos sinais.

Por meio de testes e otimizações abrangentes, é possível aumentar significativamente a taxa de acerto e a lucratividade da estratégia.

Conclusão

A Estratégia de Squeeze de Momentum do Urso Preguiçoso integra múltiplos indicadores com forte poder de julgamento, identificando eficazmente o momento de início de uma tendência. No entanto, também apresenta certos riscos, exigindo otimização de parâmetros para diferentes ativos. Com testes e otimizações contínuos, essa estratégia pode se tornar um sistema algorítmico de negociação eficiente.

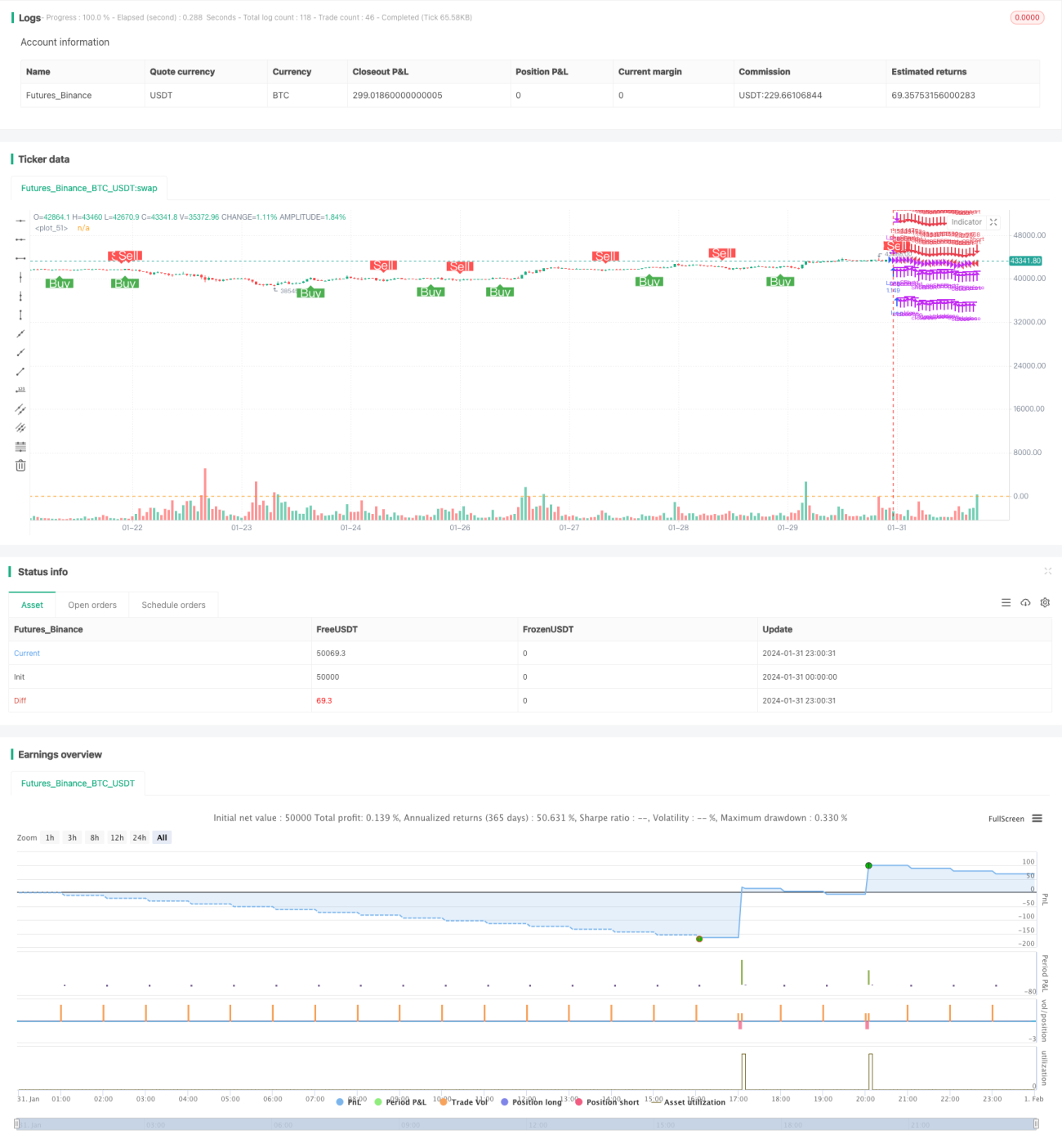

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1