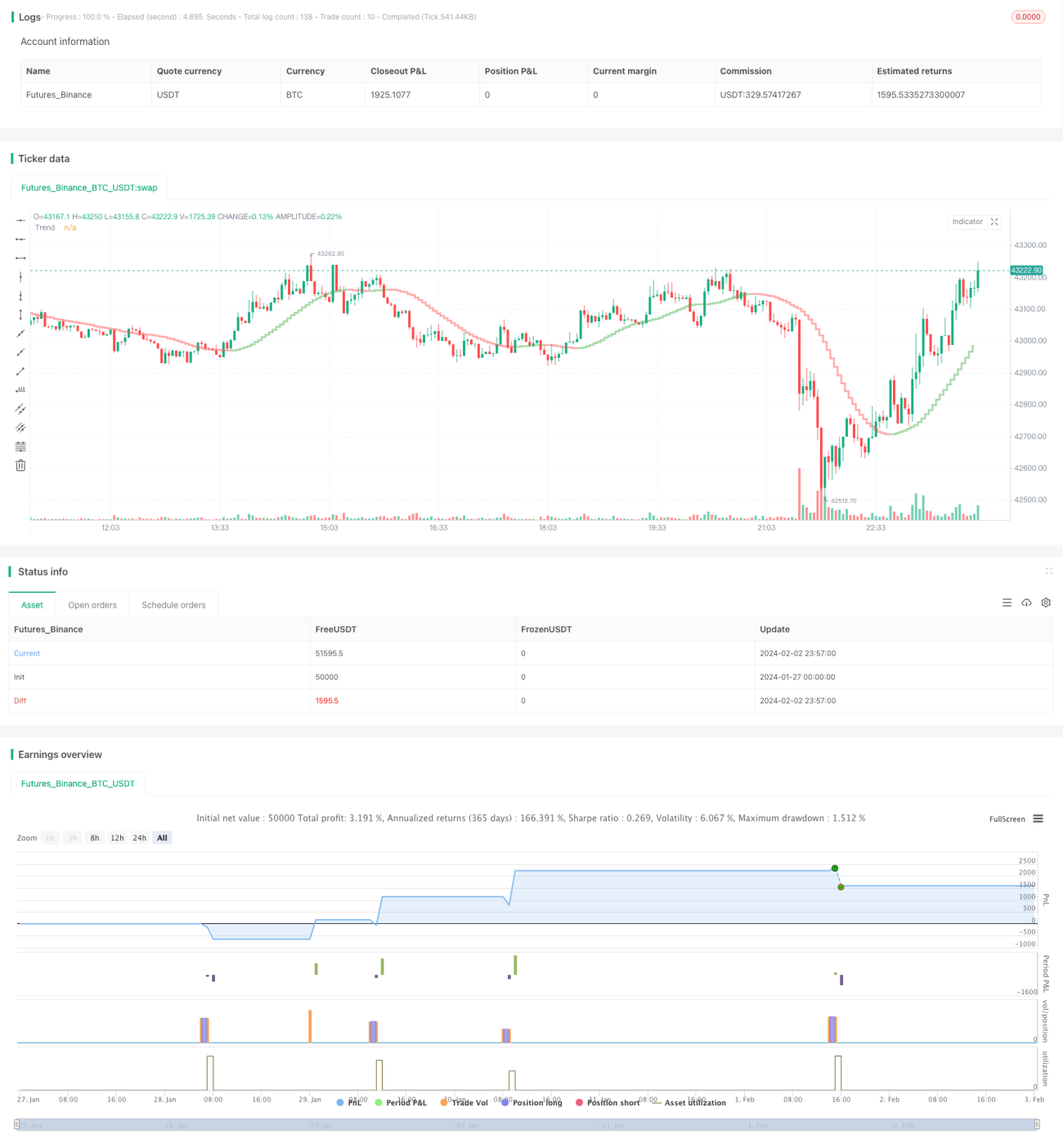

Estratégia Ripple baseada no indicador Coral Trend com backtesting em intervalos

Visão Geral

Esta estratégia utiliza o indicador Coral Trend de LazyBear para determinar a direção da tendência de preços, identificando reversões na direção do indicador para detectar potenciais pontos de entrada. Para filtrar falsos rompimentos, a estratégia emprega o indicador ADX ou uma combinação do Absolute Strength Histogram com o HawkEye Volume como confirmação, garantindo entradas mais confiáveis.

O mecanismo de saída utiliza o preço máximo/mínimo das últimas N barras multiplicado por uma relação risco-retorno configurável para definir níveis de stop loss e take profit.

Princípio da Estratégia

Após determinar a direção principal da tendência com base no indicador Coral Trend, quando a cor do indicador permanece inalterada, ocorre um pequeno pullback na direção oposta. Se o pullback terminar e o preço retornar à direção principal indicada pelo Coral Trend, considera-se um bom momento de entrada.

As condições de entrada incluem:

-

A direção do indicador Coral Trend está alinhada com a direção da negociação (long = verde, short = vermelho).

-

Desde o último rompimento completo do preço em relação ao Coral Trend (o máximo da última barra ultrapassou a linha Coral Trend), já houve pelo menos 1 barra cujo mínimo (para long) está totalmente acima da linha Coral Trend, ou cujo máximo (para short) está totalmente abaixo da linha Coral Trend.

-

Ocorre um pequeno pullback na direção oposta, durante o qual o preço de fechamento permanece consistentemente no lado oposto do Coral Trend.

-

Após o fim do pullback, o preço de fechamento retorna à direção principal indicada pelo Coral Trend.

Essas são as condições principais. Simultaneamente, a estratégia utiliza o ADX ou o Absolute Strength Histogram combinado com o HawkEye Volume como condição de confirmação.

O ADX exige que seu valor seja > 20 e que a última barra apresente aumento. Além disso, a ordem das linhas DI (verde e vermelha) deve estar alinhada com a direção da negociação.

O Absolute Strength Histogram exige que sua cor esteja alinhada com a direção da negociação (long = azul, short = vermelho). O HawkEye Volume exige que sua cor esteja alinhada com a direção da negociação (long = verde, short = vermelho).

O mecanismo de saída utiliza o preço máximo ou mínimo das últimas N barras multiplicado pela relação risco-retorno para definir stop loss e take profit. O valor de N e a relação risco-retorno são configuráveis.

Análise de Vantagens

A maior vantagem desta estratégia é utilizar o indicador Coral Trend para determinar a tendência principal e, em seguida, identificar oportunidades de entrada por meio de suas reversões, evitando seguir o mercado em tendências laterais. Além disso, o uso de indicadores de confirmação filtra muitos falsos rompimentos, aumentando a taxa de sucesso das entradas.

A estratégia também oferece um mecanismo completo de gerenciamento de risco, incluindo ajuste de stop loss e controle percentual de exposição ao risco, garantindo que mesmo perdas individuais não causem grandes impactos no capital total.

Análise de Riscos

O maior risco desta estratégia é depender de indicadores para decisões de entrada, o que pode levar à ilusão de que a configuração de parâmetros por si só gera lucros automaticamente. Na realidade, a otimização de parâmetros e a configuração de regras devem considerar os padrões subjacentes de movimento de preços, e a interação intuitiva entre indicadores e preços deve ser avaliada para definir configurações mais adequadas ao estilo de negociação e ao ativo específico.

Além disso, a definição de stop loss e take profit deve ser apropriada. Um take profit excessivamente grande pode impedir a realização do lucro, enquanto um stop loss muito apertado aumenta o risco. Isso deve ser ajustado conforme a volatilidade do ativo e a tolerância ao risco do trader.

Direções de Otimização

As áreas de otimização desta estratégia incluem:

-

Ajustar os parâmetros do indicador Coral Trend para torná-lo mais sensível às mudanças de preço de diferentes ativos.

-

Testar diferentes indicadores ou combinações de confirmação, como KDJ, MACD, para melhorar a precisão dos sinais de entrada.

-

Ajustar o cálculo de stop loss e take profit de acordo com a volatilidade de diferentes ativos, para obter melhor controle de risco.

-

Adicionar um módulo de gerenciamento de capital que ajuste o tamanho da ordem de acordo com o número de posições, controlando efetivamente a perda total.

-

Incluir um módulo de controle de horário de negociação, permitindo que a estratégia opere apenas em períodos específicos, evitando perdas durante movimentos voláteis.

Conclusão

Esta estratégia primeiro utiliza o Coral Trend para determinar a tendência de médio/longo prazo dos preços e, em seguida, identifica reversões com confirmação de sinais de confirmação para filtrar falsos rompimentos, construindo uma estratégia de acompanhamento de tendência relativamente confiável. Além disso, a configuração robusta de gerenciamento de risco permite que a estratégia opere a longo prazo com estabilidade de capital. Com otimizações adicionais de parâmetros e módulos, espera-se que a estratégia se adapte a mais ativos, oferecendo maior estabilidade e capacidade de lucro.

- 1